")

")

")

In our last coverage of Realty Income (NYSE:O) we emphasized that investors were better setup after an 8-year return drought. We went through two different longer-term scenarios at the extreme ends and felt it was hard to see it as a bad investment, regardless of what happened.

This would create a fantastic return profile with dividends reinvested. We think this is a good investment for long term holders, as long as they keep their time horizons long and their expectations modest. We are upgrading this to a Buy here.

Source: 8 Year Return Drought

This has worked out and the stock has been practically flying as if it had changed its name to “Realty A.I.ncome”. We look at the recent results and the market pricing of rate cuts to tell you where we stand.

Q2-2024

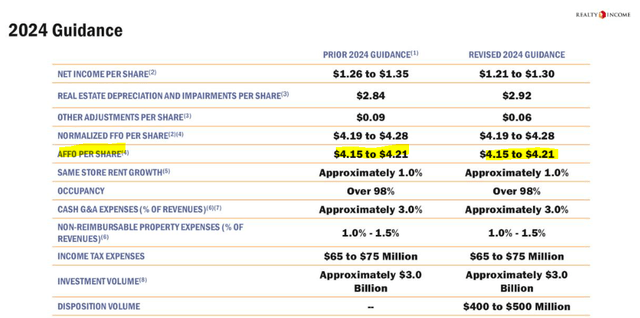

Realty Income beat Q2-2024 estimates slightly, but the amount appeared to be related to timing of the funds from operations (FFO). The REIT kept its guidance for the year unchanged.

Realty Income Q2-2024 Presentation

Analysts yawned, we as well, and in no rush to change their estimates.

Seeking Alpha

This was despite some significantly lower interest rates and credit spreads that were in place compared to its original guidance. It is probable that some of the headwinds bears have spoken about are playing out in the background as Realty income sells underperforming properties or the ones where there is a huge risk of vacancy down the line. You generally don’t see the damage from this in a direct way, but the high cap rates (low prices) on these properties tend to offset the growth numbers to an extent.

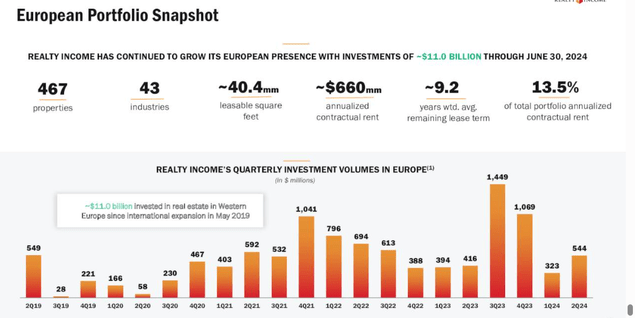

Europe

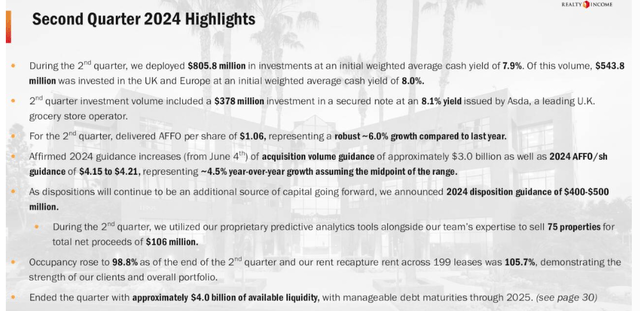

One of the big themes for Realty Income has been the push into Europe over the last few years. Long back, it was often mentioned as a positive that Realty Income was purely US focused. But bulls have begun to embrace the transatlantic capital flow, and frankly they have no choice. Realty Income is really pressing its advantage there, with two-thirds of the Q2-2024 capital going there.

Realty Income Q2-2024 Presentation

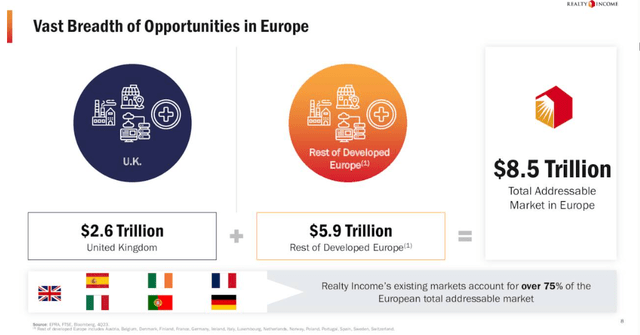

It is fairly interesting to see Realty Income show some trillion dollar opportunities in Europe.

Realty Income Q2-2024 Presentation

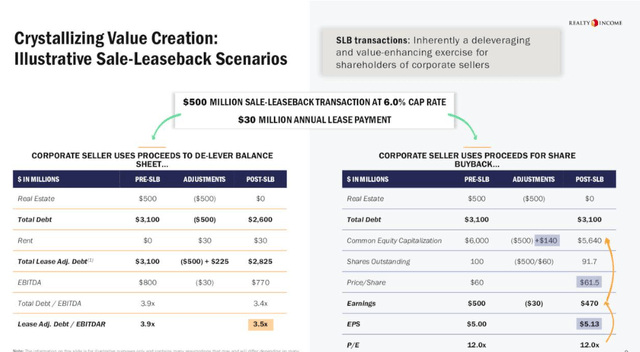

It has even gone through the trouble of showing how exactly this benefits both sides, the buyer and the purchaser (Realty Income in this case).

Realty Income Q2-2024 Presentation

One interesting thing to observe here is that the REIT is running stock buybacks into its model. Obviously, this means that it is talking about the counterparty being a publicly traded company. If you understand this part, then you can also understand the why. European companies can afford to sell their properties for a relatively higher cap rate to sale-leaseback transactions because their stocks are cheap. We can show that portion in the next chart.

Financial Times

So this is a fairly interesting dynamic that Realty Income is exploiting, and one we don’t see changing unless US stocks collapse by 50% or more. Conversely, we may see that if European stocks have a huge bull market. But in any case, Europe remains the play for now.

Realty Income Q2-2024 Presentation

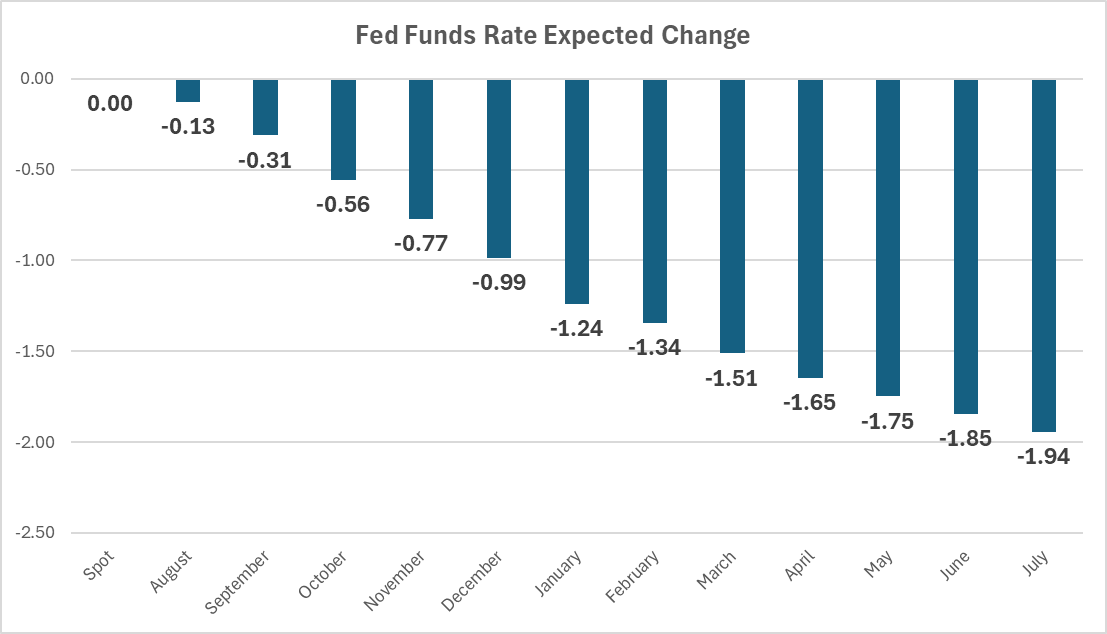

The Final Countdown

The Federal Reserve has embraced the idea of rate cuts with the markets at all-time highs and inflation remaining well above their own targets. All that remains to be done is to deliver on the 200 basis points of rate cuts priced in.

X

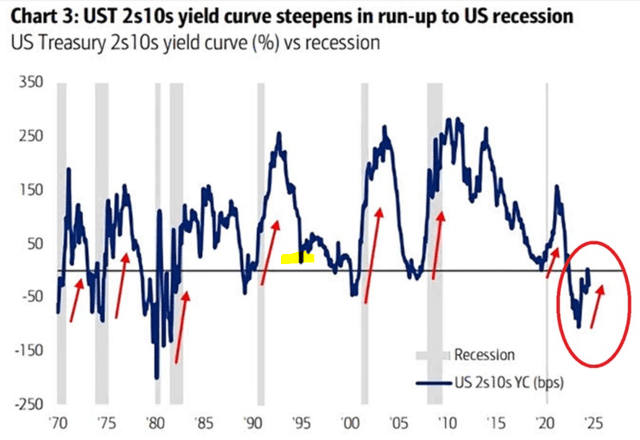

To the extent this remains consistent with an immaculate soft landing, this will support higher valuation for Realty Income. We see no problems with the stock rerating to a 17X multiple if something like this pans out. After all, we have far poorer quality REITs like Iron Mountain Incorporated (IRM) trading at exactly twice that multiple. Of course, the one real soft landing we have had after a barrage of rate hikes was in 1994 and that time the yield curve never inverted.

Bank OF America

So it remains to be seen whether we achieve this.

Verdict

If the rate cut cycles turn out to be too late to stave off a recession, there are once again risks to the downside for the company. Alternatively, we might not see the full extent of rate cuts being priced in as inflation resets at a higher base and starts moving up again. The stock looks fairly priced here for what it delivers, and it certainly is not resoundingly cheap as it was just 3 months back. We are moving this to a “Hold” and think there are better real estate stocks to speculate on for the medium term.

Realty Income Corporation 6% PFD SER A (NYSE:O.PR)

If the rate cut predictions are accurate, then O.PR is a bit undervalued. This is likely to be redeemed if the Fed Funds move down by 200 basis points, and we have a soft landing. Realty Income hates preferred shares, and this one comes courtesy of it acquiring Spirit Realty Capital. We simply don’t own it because we went long Rexford Industrial Realty, Inc. 5.875% PFD SER B (REXR.PR.B). That one had a higher yield at the time (and still does) and also had more upside to par (and still does). We rate O.PR as a hold, but it is a low-risk play for those that believe in all those rate cuts coming through.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult a professional who knows their objectives and constraints.

Read the full article here

")

")

")

")