")

")

")

")

")

Introduction

Agree Realty (ADC) and CareTrust REIT (CTRE) are two REITs that have rallied nicely since the July CPI report revealed cooling inflation. With the market pricing in rate cuts soon to follow, both are up double-digits over the past month and a half.

However, as a result of their high-quality business models, I think both still offer investors some nice upside if willing to hold for the long term. In this article, I list reasons why Agree Realty and CareTrust REIT are two quality stocks to own for the long term.

Quality Matters

When it comes to investing, my strategy is to hold stocks that can survive any economic downturn. Although these can be unexpected and some more challenging than others, things like tenant quality, balance sheet, and management play a significant role in sustainability. Additionally, their history of surviving economic volatility should be factored in as well.

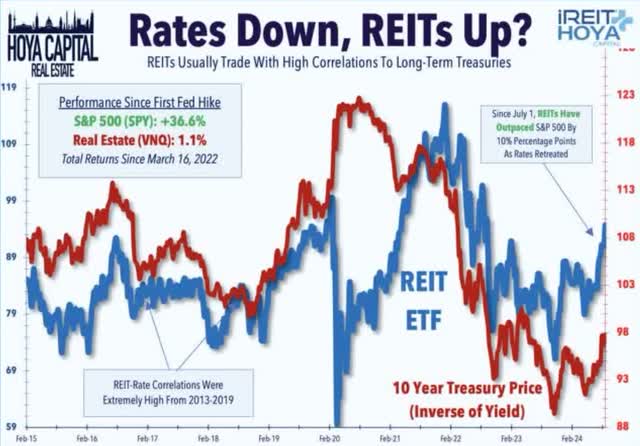

iREIT+HOYA Capital

Moreover, investing in quality stocks during market downturns helps you sleep better knowing that they have a greater chance of recovering when market times are better, like now. This is especially true for many REITs as the sector has been one of the best performing recently. In the chart above, you can see from July until now, REITs have outpaced the S&P as interest rates have retracted.

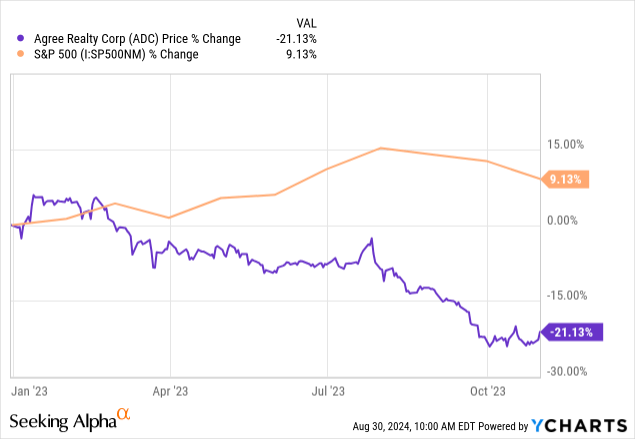

When REIT share prices suffered greatly in 2023, I continued to buy these two due to their higher-quality business models and strong fundamentals. In the chart below, you can see how Agree Realty’s share price was down significantly from January 2023 until the steep sell-off in October of that year against the S&P.

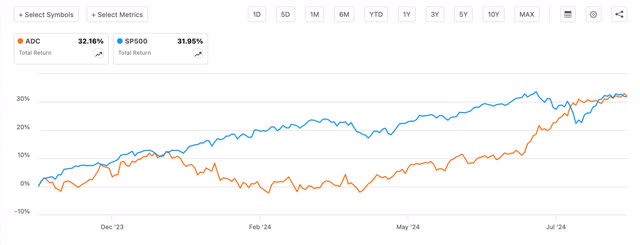

Since then, however, the stock has outperformed the S&P in total returns from the beginning of November until now. The saying “Cream rises to the top” usually holds true when things seem to be going badly. One thing to always remember is tough times don’t last, tough people do, or in this case tough businesses. But enough about that, let’s get into why you should own these two companies for the long term.

Seeking Alpha

Why Agree Realty?

Agree Realty is a triple-net lease REIT who leases properties to some of the biggest and best retailers here in the U.S. These include names like Walmart (WMT), The TJX Companies (TJX), Costco (COST), and Home Depot (HD). At the end of their latest Q2, their portfolio consisted of 68% investment-rated tenants.

This is important because during times of economic uncertainty, these tenants usually hold up better than their peers. Additionally, they are less likely to experience financial hardship and will likely pay their rent on time. During COVID, ADC collected 99% of their rent, at a time when many tenants were financially constrained, and their landlords had a difficult time with rent collections.

Agree Realty also owns properties in all 49 continental United States and have yet to tap into the international market like their big brother, Realty Income (O). I don’t foresee this happening soon, but this is just to highlight that the REIT has plenty of options for further expansion and growth.

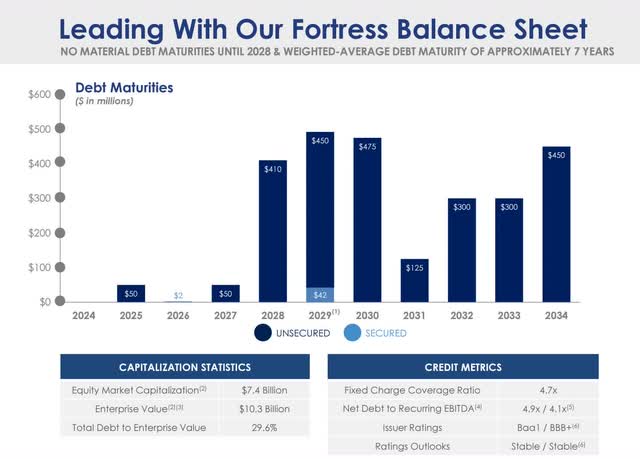

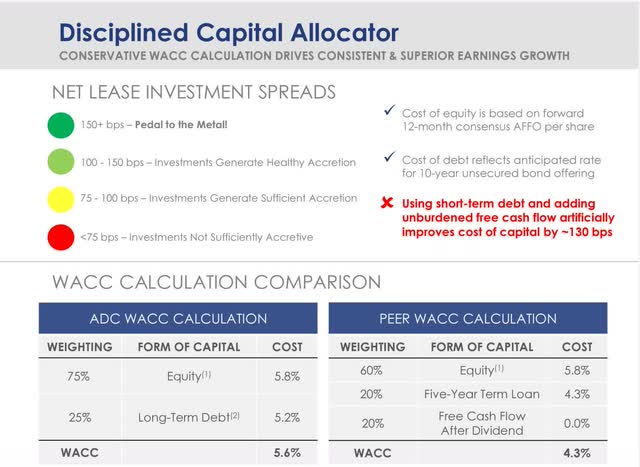

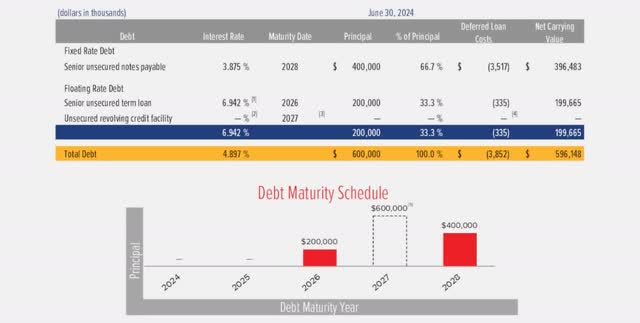

The company was rated investment grade in 2020 and recently received an upgrade to BBB+ this past June. This is likely due to their continued growth and fortress balance sheet. At the end of Q2, Agree Realty expanded their credit facility to $1.25 billion and had a total of $1.7 billion in liquidity pro forma. Furthermore, they have minimal debt maturities until 2028.

ADC August investor presentation

This puts them in a favorable position to continue acquiring properties with a low net debt to EBITDA of just 4.1x. This was in comparison to NNN REIT (NNN) and Realty Income who had net debt to EBITDAs of 5.5x and 5.3x respectively.

They also raised their acquisition guidance from $600 million to $700 million for the fiscal year. During their latest quarter, they invested $203 million across 70 net lease properties and acquired 47 for $186 million.

Their superior cost of capital is what allows Agree Realty to provide shareholders with attractive returns. These properties were acquired at a weighted-average cap rate of 7.7%. They also disposed of non-core assets at a weighted-average cap rate of 6.4%, more than 100 basis points spread.

ADC August investor presentation

Another competitive advantage not talked about enough is the ground lease portfolio. ADC had 223 ground leases and these accounted for 11.3% of annualized base rent during Q2. And these were leased to top tenants like Lowe’s (LOW), Walmart, CarMax (KMX), and Bank of America (BAC).

They also pay a well-covered, monthly dividend. And this is protected by a forward AFFO payout ratio of 73% using the midpoint of guidance. This represents a growth rate of 4.4% from the prior year and was raised to $4.11 – $4.14 during the second quarter.

Seeking Alpha

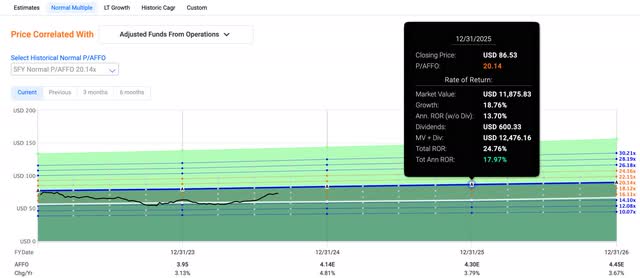

At the time of writing, Agree Realty has a forward P/AFFO multiple of 17.7x times. Although this seems expensive, this is below their 5-year average of 20.14x, signaling they could still have some upside. Over the next 12 months, ADC offers upside of 18% to their 2025 price target. And as interest rates are likely to decline gradually over that time frame, I see ADC’s share price trending in the opposite direction.

FAST Graphs

Why CareTrust REIT?

CareTrust REIT is a stock that doesn’t get enough appreciation here on Seeking Alpha in my opinion. I started covering this REIT in September of 2023 with an initial buy rating.

Since then, their share price has appreciated more than 57% in comparison to 25% for the S&P. In times of uncertainty, healthcare stocks often do well as investors typically flock to safety in the market, i.e., healthcare, consumer staples, etc.

Seeking Alpha

The REIT owns healthcare properties, with most of these consisting of Skilled Nursing Facilities. The company has been public since 2014 and has been impressively acquiring properties since that time. At the end of their second quarter, the REIT owned 285 properties across 30 states.

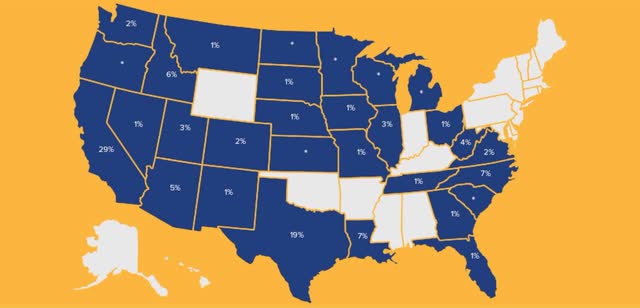

They recently acquired two SNFs for $62.1 million. You can see from the chart below, CTRE has a lot of white space and room to continue expanding. And with aging baby boomers, I expect the REIT to continue making acquisitions, particularly in the South East region where they have minimal exposure.

CTRE investor presentation

Thus far, the REIT has acquired a record of more than $800 million worth of properties at a weighted-average yield of 9.5%. During the quarter, they closed on $268 million worth of investments and two mortgage loans totaling $117 million. They also have a strong pipeline over $230 million, which I expect the REIT to execute successfully as the macro environment turns favorable due to lower interest rates.

One reason is the company’s balance sheet. At the end of Q2, their net debt to EBITDA was one of the lowest I’ve ever seen at just 0.4x, well below their targeted range of 4x – 5x. This is in comparison to another high-quality, healthcare-focused REIT, Sila Realty Trust (SILA), whose net debt to EBITDA was 3.0x. CTRE also had $100 million in cash and total liquidity of $600 million.

CTRE investor presentation

Like Agree Realty, their debt was also well-laddered with minimal due until 2026. Currently, CTRE is rated BB+ but with the way the REIT is executing, I expect they could see an upgrade to their credit rating in the near future.

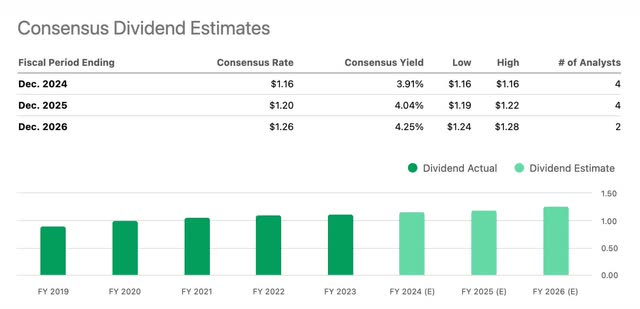

They also pay a well-covered dividend. During Q2, they raised their FFO guidance to $1.46 – $1.48. Funds available for distribution or FAD is expected to be in a range of $1.50 – $1.52. This gives them a forward payout ratio of just 77%. CareTrust REIT also has a respectable dividend track record with a decade of increases and I expect this to continue for the foreseeable future.

Seeking Alpha

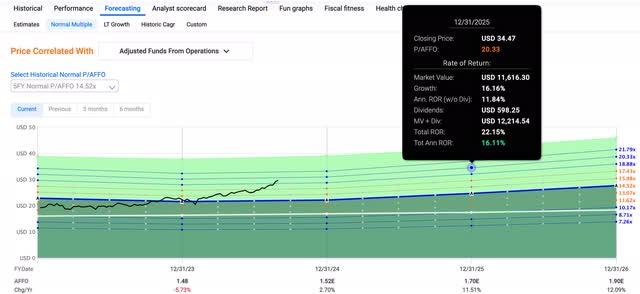

At the time of writing, CareTrust REIT has a forward P/AFFO multiple of 19.6x, above their 5-year average of 14.52x but below their blended multiple of 19.70x. Looking at the chart below, CTRE’s earnings are expected to grow by double-digits in 2025 and 2026.

Moreover, I expect their share price to follow and continue trending higher. Over the course of 12 months, the REIT offers 16.45% upside to their price target of $34.47, making them still attractive at the current price of $29.60.

FAST Graphs

Risks

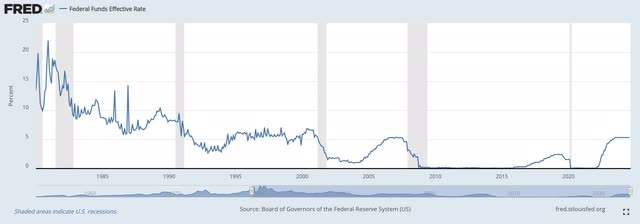

Although both companies are high-quality, they still face risks like any other (company). One major risk for both is if a recession occurs. In the chart below, you can see where interest rates were from 1980 until now. And each time interest rates were cut, they were usually followed by a recession (shaded areas indicate a recession).

FRED St. Louis

Could this be the reason Warren Buffett is hoarding cash? With the FED expected to cut this September, this is possible. If so, both companies will likely be affected if we do enter an economic downturn. And this will place downward pressure on their share prices, negatively impacting the great run both have had this year.

Bottom Line

Despite the share price appreciation, Agree Realty and CareTrust REIT have both seen so far in 2024, I think both still offer attractive upside over the next 12 months. Of course, if the economy falls into a recession, this could impact both companies’ share price going forward.

However, both are high-quality companies that I expect to successfully navigate any downturns as a result of their low-leveraged balance sheets, stellar management teams, growth execution strategies, and recession-resistant business models.

Furthermore, in uncertain times like now, quality over quantity plays a significant role when owning equities for the long term. With that being said, both Agree Realty and CareTrust REIT are two REITs long-term dividend investors should consider for reliable, and growing income.

Read the full article here

")

")

")

")

")

")