")

Thesis

PIMCO Preferred And Capital Securities Active Exchange-Traded Fund (NYSEARCA:PRFD) is an ETF launched in 2023 by the behemoth asset manager PIMCO. The fund seeks total return, with income as a secondary objective, and takes an active approach towards investing in preferred securities. As per its own literature, the ETF:

Provides investors with exposure across preferred, capital securities and corporate hybrid markets, focusing on attractive valuations within the market while taking advantage of attractive subordination premia. Through active management, the fund seeks to manage liquidity, duration, and relative value opportunities while maximizing risk-adjusted returns and offering the tax advantages of preferred and capital securities.

In this article, we are going to take a closer look at the fund’s structure, its holdings and analytics, as well as express our view on how PRFD fits within a cohort of its peers.

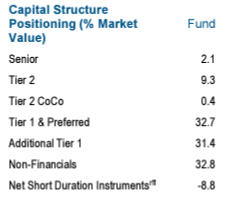

Composition – overweight financials

Just like many of its peers, the fund is overweight securities issued by financial institutions:

Holdings (Fund Fact Sheet)

Non-financials make up only 32.8% of the holdings, with the rest representing various subordinated securities within the financials space. While some securities represent Tier 1 capital, a 9.3% bucket is allocated to Tier 2:

Tier 2 is designated as the second or supplementary layer of a bank’s capital and is composed of items such as revaluation reserves, hybrid instruments, and subordinated term debt. It is considered less secure than Tier 1 capital—the other form of a bank’s capital—because it’s more difficult to liquidate.

Tier 1 and Tier 2 securities are ultimately a bet on a financial institution’s soundness, and barring another great financial crisis, the underlying holdings should be in good standing. Nonetheless, it is worth remembering we had a sudden wave of regional bank failures in March 2023, where the respective preferred equity was wiped out, a wave which culminated with the Credit Suisse takeover and the complete wipe-out of their CoCo bonds even though they did not default.

Unlike regular corporations, banks rely on the faith of the public to stay solvent given their leverage, and any bank run will usually result in the complete wipe-out of common equity, preferred equity, and the majority of the senior bond balance.

From a ratings perspective, the ETF has a balanced approach, with almost equal weights in terms of investment grade and non-investment grade bonds:

- BBB rated: 43%

- sub-investment grade: 33%

- not rated: 24%

However, please remember that Credit Suisse’s preferred equity was mostly investment grade before the UBS rescue and takeover.

From an analytics standpoint, the fund’s portfolio falls in the intermediate duration bucket with a 4.81 years effective duration. The effective maturity reported by the fund is 7 years. The ETF also comes with an adjusted expense ratio of 69 bps.

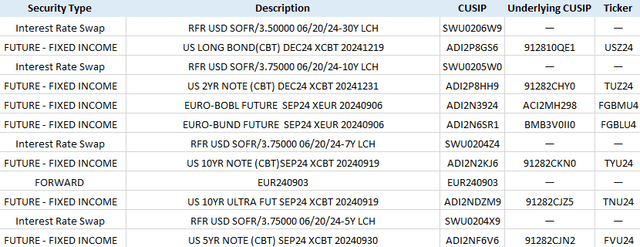

Active management and composition

The distinctive feature for this name is its active management. The fund benchmarks itself against the “ICE BofA US All Capital Securities Index”, but has a very active management, especially when it comes down to duration:

Duration Hedges (Fund Website)

The above is a snapshot of some of the instruments currently present in the fund to manage duration. The name takes views via bond futures (in the Security Type field you can see Future – Fixed Income) and also hedges out certain individual names via interest rate swaps.

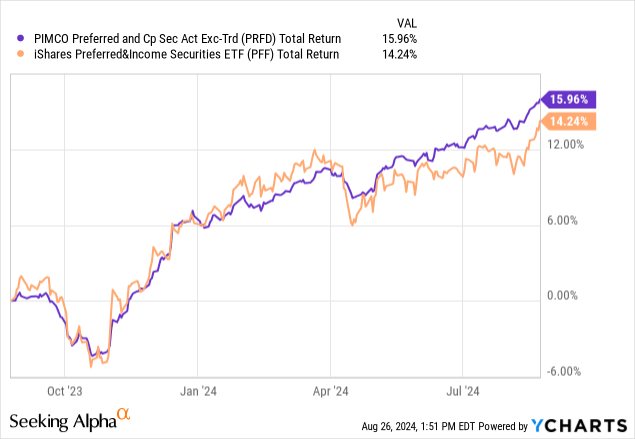

The active take on holdings has helped the name outperform in 2024:

In the above chart, we are comparing the ETF with the iShares Preferred and Income Securities ETF (PFF), the ‘to-go-to’ name in terms of unleveraged preferred equity exposure. We are using a total return analysis so that we smooth out any dividend yield differentials. From the chart, we can see PRFD outperforming in 2024, while the correlation and total return are very high prior. As rates moved higher at the beginning of 2024, PRFD had a shallower drawdown when compared to PFF given its duration hedging. Expect active management to continue to provide positives for the fund going forward.

We like active funds with minimal interventions that steer the ship in the right direction when the wind changes. Active management to us is not a 50% portfolio turnover, but the exploitation of obvious overbought or oversold signals, especially in the rates space.

Yield considerations

The fund is straight-forward in terms of seeking total returns rather than current income. To that end, the 30-day SEC yield is on the low side:

Yield (Fund Website)

Currently, the 30-day SEC yield is a paltry 5.65%, with a portfolio estimated yield to maturity of 6.99%. These levels are not very enticing as they stand, but please keep in mind the fund has rallied tremendously in the past year, and spreads have also tightened towards the bottom of their historic range.

The name is not a buy at the current levels, but can open up with an attractive entry point if spreads widen out again. Given the stated fund objective, do not expect eye-popping figures in terms of yields here, especially since the structure is an ETF and thus unleveraged.

In our mind, PRFD represents a duration managed alternative to PFF, with the fund having proved its mettle in 2024 via its outperformance. However, an investor here is still buying preferred equity and spreads are currently not attractive. Financials have rallied significantly in 2024 on the back of a soft landing base case, with both common and preferred equity being moved up along the way. A sudden change in the base case or doubts about a soft landing would percolate down to financials, and thus might open up an attractive entry point into PRFD.

Conclusion

PRFD is a fixed income exchange-traded fund. The vehicle comes from PIMCO, and represents an actively managed fund in the preferred equity space. The name has outperformed PFF in 2024 (PFF being the golden standard) via duration management using bond futures.

PRFD is up almost +16% in the past year, having benefited from the rally in financials common and preferred equity. The name is overweight Tier 1 and Tier 2 securities from financial companies, which represent almost 70% of the holdings. With spreads very tight currently, PRFD is now yielding only 5.65%, making today’s levels unattractive from an entry standpoint. We are on ‘Hold’ in respect to this name until a risk-off move creates an attractive opportunity.

Read the full article here

")