")

Co-authored by Treading Softly

As humans, we’re naturally inclined to evaluate what we see very rapidly and from an external perspective. This is one reason why people like to say that beauty is in the eye of the beholder. This is largely because what you think is beautiful may only be the exterior of the object. The internal qualities may not be readily visible. You can take a quick look at somebody, and while they may be perceived as beautiful or ugly, you will not know their intelligence levels or character.

The story is told of a man who is looking to find a king and goes to a specific family. He sees the oldest son and thinks that this is the man who is to be king. But by the end of the story, it turns out that the youngest and least visually appealing individual in the family was meant to be the king. He would’ve been overlooked due to his age and perceived inexperience. What was inside was most important, not the external aspects.

When it comes to the market, we can often be allured by high yields or charts that trend upwards from left to right. In the process, we fail to dig deeper to understand what’s going on with the chart, the yield, or the investment in general. Sometimes, we fall victim to historical trends, thinking that past returns will guarantee future success. We internally know that it’s not true. Sometimes, you need to look at the younger, the less refined, and the less recognized to find the best opportunities. Often finding opportunities in the market involves digging a little deeper than just doing a preliminary surface level evaluation.

Today, I want to examine one fantastic fund that is often overshadowed by its older brother.

Let’s dive in!

PIMCO Dynamic Income Opportunities Fund (NYSE:PDO), yielding 11.3%, is one of the younger closed-end funds in the PIMCO family. PDO invests in various types of debt. Most debt investments have seen prices fall over the past years as the price of U.S. Treasuries has declined, dragging along all other debt with them.

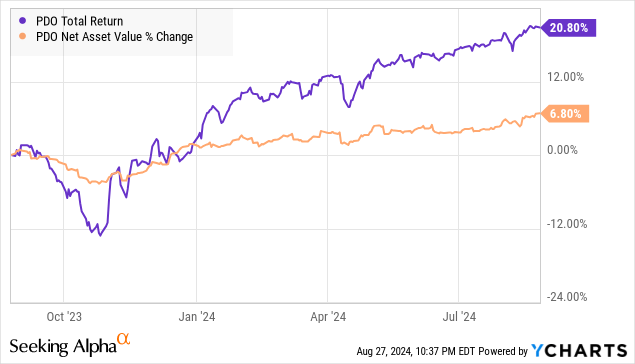

Since bottoming out in October 2023, PDO has produced nice, steady returns, comprised of a hefty distribution and an increase in NAV of about 6.8% (after distributions). This has resulted in a total return of about 21% over the past year.

Debt investments are sensitive to two core factors.

The first factor is Treasury Rates. All debt investments can be measured against the return that an investor can get from investing in a US Treasury with similar maturity. After all, an investment in a US Treasury is about as close to “safe” as an investor can get. At the time of purchase, you know exactly what your return will be if you choose to hold to maturity. As Treasury prices go up or down, the prices of other debt will be influenced as investors have the option to buy Treasuries instead of taking on the higher risks of other debt investments. This is why we see the entire bond market shifting with Treasury rates.

The second factor is credit risk. If you’re looking at holding a bond that was issued by an A-rated company with a trillion-dollar plus market cap, you are technically taking on more risk than you are buying US Treasuries, but is it meaningfully higher risk? The premium you need likely is not high.

On the other end of the spectrum, if you’re buying debt in a company that’s likely to file for bankruptcy or already has filed for bankruptcy, you’re taking a higher risk and will require a much higher potential return.

PDO is a fund that specializes in credit risk investments. While it’s sensitive to interest rates, like all debt, its focus is on identifying opportunities where it believes the market is overestimating the risk.

In the quarterly commentary, PDO’s management wrote:

“With a flexible multi-sector approach across public and private markets, we seek relative value by investing in opportunities where spreads have widened and yields are high, yet we believe credit risk hasn’t increased meaningfully.”

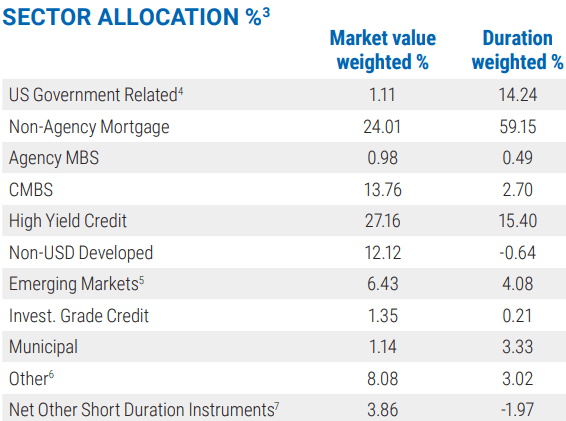

This philosophy has led to PDO having the following allocations:

PDO June 2024 Quarterly Commentary

Their largest sector is “high-yield credit.” In this sector, PIMCO has been focused on what it calls “special situations.”

“We are especially focused on corporate special situations opportunities, where PIMCO can act as a liquidity provider or offer rescue financing. These opportunities are appealing due to their limited downside risk and significant upside potential.”

An example of a “special situation” that we pointed out before was PIMCO stepping in to buy up the debt of Carvana (CVNA) when it was having troubles that many thought would lead to bankruptcy. At one point, PIMCO offered to buy the whole company. While that was refused, PIMCO was able to negotiate a very favorable debt exchange that alleviated CVNA’s near-term cash flow issues.

Recently, CVNA saw its debt receive an upgrade from S&P, from CCC+ to B-. PDO holds $30 million in face value of CVNA’s 13% and 14% bonds maturing in 2030 and 2031, respectively. These bonds were trading in the mid $80s in September when they were issued. Now, both of these are trading well over par. The 14% 2031 bonds recently traded over $113. This gives PIMCO the option of collecting the oversized coupons, or selling them and deploying the cash into another opportunity.

These decisions have led to PIMCO being one of the best bond CEF managers of all time. They identify opportunities where others are fearful and use their size, scale, and expertise to extract maximum value. CVNA went from bonds priced for bankruptcy to bonds trading at large premiums to par. PIMCO identified that opportunity while many were running in the other direction.

The turmoil in interest rates created many opportunities where the market overestimated the risks. PIMCO has been adding to its CMBS (Commercial Mortgage-Backed Security) investments as many good quality CMBS have been thrown out along with those properties that are distressed. PIMCO’s non-agency MBS portfolio was built during the mortgage crisis. As banks were dumping mortgages, PIMCO was buying.

These are the decisions that have led other PIMCO bond funds to outperform other debt opportunities. Many of PIMCO’s funds trade at large premiums to NAV. PDO is trading at a small premium (currently under 4%). Part of the reason is that PDO is a term fund and is scheduled to terminate in January 2033. This means that investors can expect to receive NAV if the termination date is not extended. We wouldn’t count on that happening, as we have seen many “term” funds in the past vote to end the term feature long before the date arrives. However, in the meantime, that feature plays a role in keeping the share price closer to NAV than we see with PIMCO’s perpetual funds.

For those of us who want to be buyers, that’s a great thing. We can buy at only a small premium and enjoy the income-producing talents of PIMCO’s elite team.

Conclusion

When compared with its siblings, PDO trades at a much smaller premium. We also see a comparably attractive yield. Its unique aspect is that PDO is a term fund with a set end date unless that gets changed. What that means is that this CEF is often overlooked and underrecognized as a high-quality fund managed by high-quality managers.

This means that you can get strong income at a reasonable valuation while having access to a world-class management team with a proven track record of outperformance. While we love the tried-and-true older funds, PDO is definitely worthy of adding to the mix.

When it comes to retirement, being an income investor means that you are part of a minority group of investors. It may come as a surprise to you that the vast majority of people planning for their retirement fail to recognize that they can unlock a massive flood of dividends from the markets. Instead, they remain fixated on building a massive pile of cash to slowly erode in their golden years. You are currently the unrecognized and overlooked sibling compared to most retirees in their retirement planning. But to me, nothing could be more beautiful than when your portfolio provides you the income you need in retirement, and you don’t have to sell a single thing.

That’s the beauty of my income method. That’s the beauty of income investing.

Read the full article here