")

")

")

")

Though as an investor focusing on dividends and dividend growth, I do appreciate a rising stock price too. Right now, it looks like Philip Morris (NYSE:PM) is offering both.

Investors should not be deterred from investing in Philip Morris based on the recent bull run in the stock. Investors should rather view the run as confirmation that the market is finally starting to see the growth initiatives materializing. At current prices, dividend growth investors will lock in a decent yield and many years of robustly growing dividends.

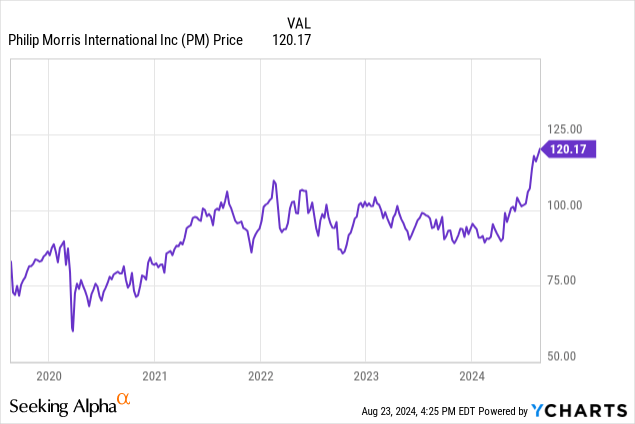

Since late April, the stock has been on a tear, breaching all-time highs. As if that isn’t enough to satisfy investors, in September the Board will raise the dividend once again. For a number of years now, the dividend growth rate has been sub-par. Last year I predicted a new dividend of $1.33 whereas the actual new dividend landed at $1.30. So I’ll have to be careful and temper my expectations a little bit. That said, the company is growing more quickly now than it used to, providing a more solid foundation for dividend growth.

Since mid-April, when the stock bottomed out at around $89, the stock has been going almost straight up to just about breach its all-time high level of $122 from June 2017.

Longer term, though, the stock is definitely still up, but at a much slower pace. Five years ago, the stock stood at $81, which means a price appreciation of 48% over five years. That equates to an average annual appreciation of 8.2%. Adding in the annual dividend yield of about 5% over the period produces a total average annual shareholder return of 13.2%. That is solid and above the long-term returns of the market, though as we’ve seen, much of it has come over just the last couple of months.

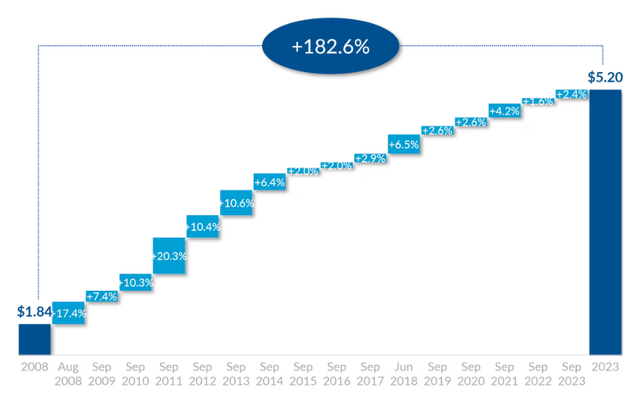

Historical Dividend Growth

You can count on this company sending a dividend check your way every three months. Since being spun off from Altria (MO) back in 2008, it has paid a quarterly dividend and consistently increased its dividend every single year. Some of the earlier years were just impressive with annual hikes of the likes of 17% and 20% as can be seen on the chart below, retrieved from the company’s dividend information page:

Dividend growth (Philip Morris Investor relations site)

Alas, it’s been more than a decade since Philip Morris last hiked its dividend by double digits. Investors have had to content themselves with puny 2-4% annual dividend increases, which has not even been enough to compensate for inflation in the last couple of years.

Five years ago, the quarterly dividend stood at $1.14, now it is at $1.30, for a total growth of 14% — or 2.7% annually. Not really the kind of pace dividend growth investors are looking for. At the end of the day, over time the dividend has to grow in line with underlying earnings growth, and when the latter has been disappointing, so will the former.

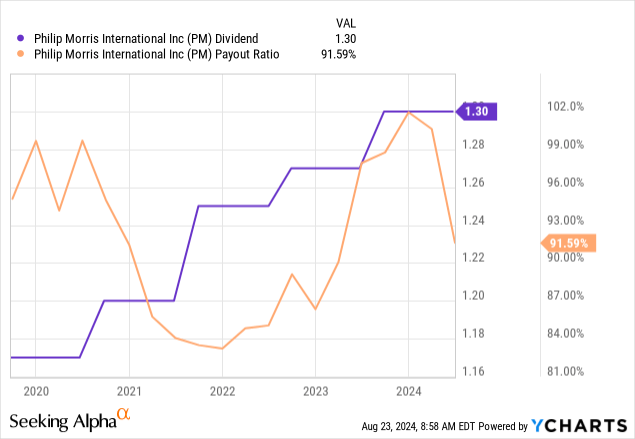

I will at least give the Board of Philip Morris one thing: It has managed to grow the dividend annually on a consistent basis, as can be seen in the purple line above. The orange line reveals why the annual increases have not been higher. For much of the last five years, the payout ratio has hovered around 100% — that just puts a hard limit as to how much you can bump the dividend. The best period was in early 2022, but even then, the payout ratio was high at almost 84%.

The good news is that the recent trend is that of a falling payout ratio, giving the Board some breathing room when it evaluates this year’s increase. Even so, it would be wise to have limited expectations when it comes to the next dividend announcement, as I think the Board would like to see a substantially lower payout ratio before it starts swinging for the fences.

September Dividend Hike

In an ideal world, I would like to see a lower payout ratio so that the Board would have one less worry and one less constraint when setting the new dividend. However, we have to work with what we have. All else equal, the payout ratio will be a drag on dividend growth this year. That is to say, we must assume that the Board will save some of the EPS growth for later years in order to have a cushion to absorb challenging periods when they come.

To have any chance of growing the dividend at all, this company must provide some earnings growth. Luckily, the way things are going over at Philip Morris, it looks like it can be able to churn out double-digit EPS growth this year. In the second quarter, adjusted diluted EPS excluding currency grew 10.6%. All segments are doing well. Even in the combustibles segment, revenues and volumes are up, in stark contrast to Altria where volumes were down in its Q1 period. The smoke-free business is doing even better, particularly helped by ZYN’s phenomenal growth — shipping 50% more cans in the American market than a year ago. In other good news, it is worth noting that at the end of 2023, IQOS surpassed Marlboro in terms of revenues. Marlboro — the symbol of cigarettes for so many decades, is now less important to Philip Morris than the fairly newly invented IQOS!

It’s never a good thing to be losing revenue due to supply constraints as is the case with ZYN, but it is nonetheless the best problem you could have. You’re not building new factory facilities wondering whether the product will sell, you are certain that the new factory will be a money-maker from day one, you just can’t build it quickly enough.

This bodes well for the full year, and indeed the company raised its full-year guidance from an EPS growth of 9-11% to a growth of 11-13% and expect a mid-range EPS of $6.39. If it reaches this new level, at the current dividend rate we’re talking a payout ratio of 81% — the lowest level in at least five years. We — and the Board — can be confident that there is room to grow the dividend. Historically, the lowest increase we’ve seen in recent years is the 2 cent increase in 2022. Things were worse back in 2022, so I would judge the absolute minimum possible increase to be the same as last year, that is 3 cents. I see few reasons why the Board should be that conservative, though, with EPS growing at 10%+ and the management team professing to be confident in long-term EPS growth of 10%, there should be room to share some of that growth with its investors by way of cold hard cash.

On page 108 of its Investor Information July 2024 slide package it says it targets a 75% payout ratio over time. It hasn’t been at that level for a long time so I view it as a target it would work towards incrementally. However, the target definitely rules out the possibility of a full 10% dividend increase, as some of the EPS growth would have to be used toward lowering that payout ratio. A fair compromise this year would therefore be a 5 cent, or 3.8% increase. The annual dividend would be $5.40 for a payout ratio of 85%. It would be one of the lowest payout ratios over the last five years, and be a nice step towards the 75% target. At the same time, investors would receive a noticeably higher increase than in recent years, a signal that times of higher growth are ahead. My prediction is therefore that the Board would go for a new quarterly dividend of $1.35 this September.

Risk Factors

An obvious risk factor for Philip Morris is currency risk. As the U.S. dollar has been rising for the last ten years or so, I don’t think there’s been a quarter where the company has not been mentioning the currency — usually the currency headwind. We tend to think that currencies fluctuate, but in terms of the U.S. dollar, it’s been an almost continuous uptrend for a decade. If and when the dollar turns, the company would get the wind in its back, and it would be easier to produce EPS growth as reported in U.S. dollars.

Another risk is consolidation among its competitors. When competitors consolidate, they can scale more efficiently, get more favorable sourcing contracts, get more shelf space in stores and have deeper pockets when competing against Philip Morris. Just this week, it was announced that Japan Tobacco (OTCPK:JAPAY) will acquire U.S. centric Vector Group (VGR). Though Vector Group is operating in the combustibles space in the U.S. and is therefore not a direct competitor to Philip Morris, Japan Tobacco will become larger and be better able to compete against Philip Morris in smokeless products and in overseas markets.

Regulatory risk is a constant in the tobacco industry. In June, Philip Morris decided to suspend online sales of ZYN in response to a subpoena from the District of Columbia. Hopefully, it will resolve itself in not too long, but it goes to show the constant risk the industry faces.

Lastly, I would like to highlight innovation as a risk factor. For decade after decade, the only innovation we saw were different marketing techniques. In the last decade, however, we have had some real innovation. Luckily for Philip Morris, it is leading the pack. Still, it would be naïve not to think that a competitor could come up with some compelling products, eating into Philip Morris’ profit margins.

Current Valuation

It’s nice to know the company is growing robustly and that the payout ratio is creeping down. But a good company is only a good investment if we can get it for the right price. In order to figure that out, I will look at some key metrics and compare it to the two largest global competitors, British American Tobacco (BTI) and Japan Tobacco.

| Philip Morris | British American | Japan Tobacco | |

| Price/Sales | 5.0x | 2.4x | 2.5x |

| Price/Earnings | 19.5x | 9.6x | 16.3x |

| Yield | 4.3% | 8.2% | 4.6% |

Source: Seeking Alpha and Japan Tobacco For Shareholders site

The Price/Sales category is won by British American, just in front of Japan Tobacco, with Philip Morris lagging far behind with a multiple twice that of JAPAY’s. When it comes to the P/E ratio BTI is the cheapest one by far, being the only one down there at single digits. Philip Morris is unquestionably the dearest of the three, and it’s been years since I’ve seen it at this level. This multiple is still lower than many other consumer staples stocks, but it has to produce some decent growth in order to defend that multiple.

The dividend yield category is won hands down by British American. Before the recent stock rally, this company offered a double-digit yield. Still, 8.2% is a buy in my book. That said, yields of 4.6% and 4.3% are more than competitive when compared to the yield of the SPDR S&P 500 ETF (SPY) of 1.2%.

I think, as I have for years, that all these companies are solid investments. Admittedly, PM is more expensive than the other two, but it is also leading in innovation and growth in new product categories, while still generating bundles of cash from the legacy combustibles products, where it also has a solid position. Analysts on Wall Street expect management to just about deliver on its long term EPS growth target of 9-11%, by churning out an average annual growth rate of 9.4%. Assuming that the P/E ratio of 19.5x stays constant and adding in the yield of 4.3%, we arrive at an expected average annual shareholder return of 13.7%. Comfortably in the double-digit return space of which a third is paid out in the form of cold hard cash — all provided by the global leader in its industry, that is a prospect I will invest in. And so should all other dividend growth investors out there. Few stocks can offer a nice current yield, double-digit long-term growth prospects and limited downside risk, but Philip Morris can.

Conclusion

Philip Morris has been operating as an independent company since 2008, raising its dividend every year since. Though growth has been anemic over the last decade or so, the company is now growing at double digits and looks set to continue doing so for the foreseeable future. The market has noticed and started bidding up the stock. Still, it’s not too late to join the bandwagon. Investors who get in now will enjoy a nice current dividend yield with a nice bump later in September and likely get even larger hikes in the years to come. A generous current yield with double-digit long-term growth prospects on top is exactly the kind of combination to dividend growth investors are looking for.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")