")

")

Investment thesis

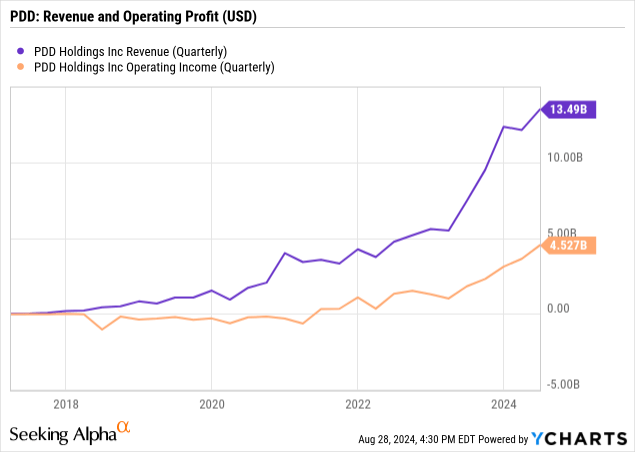

In any other world, PDD Holdings’ (NASDAQ:PDD) Q2 earnings report on Monday would have been a cause for celebration: +86% y-o-y revenue growth (slightly below consensus estimates, but who’s complaining?); +156% operating profit growth, and +144% earnings growth.

These numbers, however, hide the immense challenges that PDD will face in the near future from competitive pressures, a weakening Chinese economy, tumultuous merchant relations, and above all, political scrutiny from China, the US, and Europe. Peers/competitors Alibaba Group Holding (BABA) and JD.com (JD) have been experiencing similar obstacles since 2021; their respective stocks have massively underperformed.

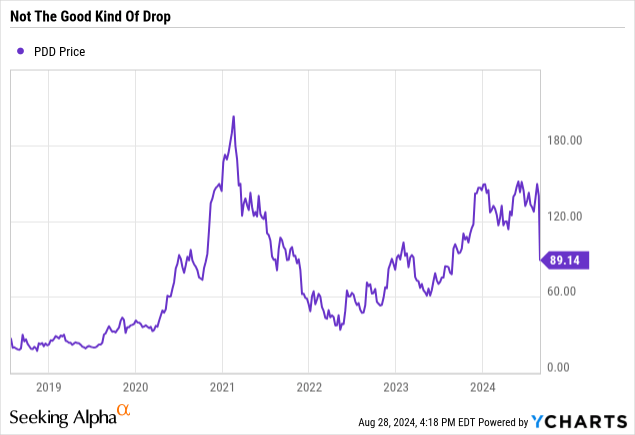

As the -30% drop in share price and cheap trailing valuations may make the stock look tempting, I think investors are right to be cautiously selling PDD for now. In this article, I present a vision of what PDD would look like if any combination of the aforementioned challenges come to fruition; a company that experiences narrowing profit margins with several potential revenue cliffs.

Q2 earnings: Growth with a side of humility

PDD’s Q2 earnings report, released on Monday, should have been a cause for celebration; revenues grew +86% y-o-y to CNY 97 billion ($13.4 billion), operating profit grew +156% y-o-y to CNY 32.6 billion ($4.5 billion), and net profit grew +144% y-o-y to CNY 32 billion ($4.4 billion). Profit margins remained near record highs (65% gross, 33% net) while the company generated CNY 44 billion ($6 billion) in operating cash flow, representing strong earnings quality.

The disappointment came during PDD’s earnings call, where the typically conservative management warned of “many new challenges ahead” and of a “new phase of high-quality development” that will result in increased investments and lower profitability. Instead of focusing on PDD’s incredible revenue and profit growth, Chairman and Co-CEO Chen Lei’s comments were a litany of how the company will sacrifice growth and profitability in service of China’s various social development priorities:

- Collaborating with new brands and manufacturers to create growth opportunities for them.

- Investing in supply chain efficiencies to help farmers sell seasonal produce to urban consumers (an otherwise small and lower-margin business).

- Reducing merchant transaction fees by CNY 10 billion in the first year.

- Investing in trust and safety capabilities and “actively identifying and removing unlawful vectors.”

In no uncertain terms, Chen concluded: “sacrificing short-term profit is necessary,” and “high revenue growth is not sustainable and a downward trend in profitability is inevitable.”

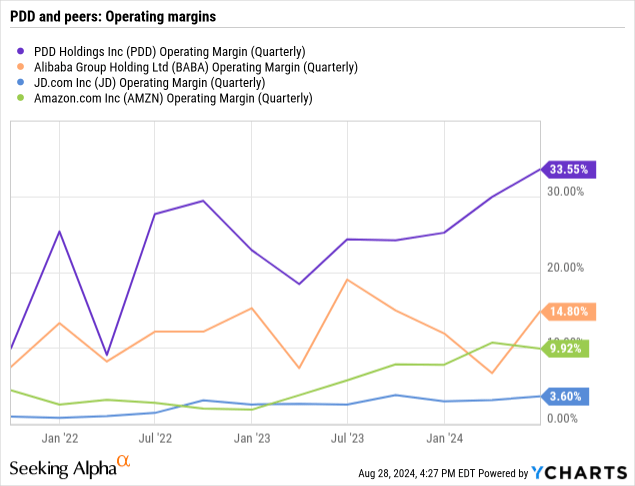

Competition intensifying

After years of taking market share from Alibaba in China and Amazon outside China, PDD’s competitors are finally responding in force. Alibaba’s recent results show that the company’s revenues and profits are starting to grow again, as it embarks on a wide-ranging restructuring. This comes alongside a generally weakening Chinese economy, where consumers are becoming more price-conscious and reducing spending — meaning that PDD, Alibaba, and JD.com will all be competing more intensely for a slower-growing pie.

Meanwhile, Amazon (AMZN) is reportedly planning a new discount section on its website for merchants to ship cheap products straight from warehouses in China, competing directly with Temu and Shein. This will provide immediate competition to Temu’s otherwise rapid growth in the US in recent years. PDD notably does not disclose how much revenue comes from Temu or other overseas revenues.

Both developments nevertheless portend that PDD’s days of rapid growth may already be behind it.

Political scrutiny

PDD’s various apps are facing increased scrutiny from multiple governments, which could lead to restrictions and political attacks that result in lower sales and lower profits. In the best-case scenario, this amounts to low-impact regulations that may cap PDD’s commissions or limit the types of products the company can sell in certain markets. In the worst-case scenario, regulators in China could drastically reduce PDD’s ability to charge commissions and fees to merchants, while regulators in Europe and the US could impose hefty tariffs and other restrictions on products sold on the company’s popular Temu app.

In China, the company is facing increased scrutiny over the commissions and fees it charges merchants; this raises the possibility that the government may step in to impose caps on such fees. In late June, hundreds of merchant suppliers staged a protest at the company’s offices in Guangzhou, alleging PDD’s return and after-sales support fees were unfairly high. Police were eventually called to disperse the protestors. This came amid China’s broader push for “common prosperity” and “high-quality development,” both of which have excluded consumer-focused companies like PDD from government support and access to certain forms of capital.

Meanwhile, regulators in the US and Europe are considering imposing high tariffs on the low-value goods that form the bulk of PDD’s Temu, Shein, and TikTok Shop’s merchandise volumes. Such tariffs, if imposed, would significantly increase the prices of products on Temu and reduce their attractiveness to price-conscious shoppers. In this situation, revenue from PDD’s overseas operations would likely plateau or decline.

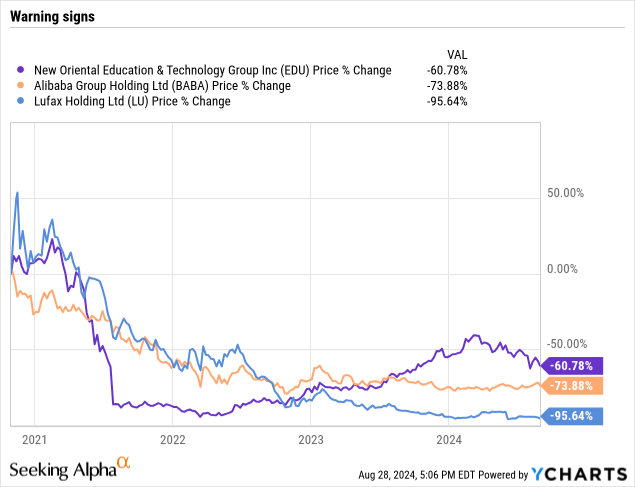

In general, being the target of political and regulatory scrutiny is not good for your business or share price. The world of Chinese equities, in particular, is filled with examples of businesses from e-commerce to education to fintech, whose revenues and profits disappeared overnight through decrees.

Valuations: Putting it all together

What could this “new phase” look like for PDD? Let’s break down how these challenges would affect the company.

Revenue

PDD’s domestic revenue growth could slow down significantly to a respectable 10% y-o-y after 2025 as a result. Political pressure in China for PDD and other e-commerce companies to cut commissions and fees will naturally result in lower revenues, though this may partly be offset by higher volumes from more merchants.

A more substantial risk to PDD’s revenues comes from the risk of the US and EU slapping tariffs on the low-value goods sold on Temu. Such a move would severely impact Temu’s business overnight. PDD does not disclose Temu’s revenues, but assuming it is in the same range as Shein’s estimated $30 billion in annual sales, this means that such a move would affect one-third to one-half of PDD’s revenues.

In a world without additional tariffs, PDD could see revenues of CNY 500 billion ($70 billion) in 2025, putting the stock at a reasonable 1.3x EV/Sales. In a world with tariffs, PDD could see one-third of these revenues disappear and end up with sales of CNY 350 billion ($50 billion).

| Scenario A: Revenue growth slows to +10%, net margin declines to 10% | |||||||

| CNY millions | 2019 | 2020 | 2021 | 2022 | 2023 | 2024F | 2025F |

| Revenue | 30,142 | 59,492 | 93,950 | 130,558 | 247,639 | 470,514 | 517,566 |

| % growth y-o-y | 97% | 58% | 39% | 90% | 90% | 10% | |

| Net income | (6,968) | (7,180) | 7,769 | 31,538 | 60,027 | 102,903 | 51,757 |

| % net margin | -23% | -12% | 8% | 24% | 24% | 22% | 10% |

| % growth y-o-y | 3% | -208% | 306% | 90% | 71% | -50% | |

| Scenario B: Tariffs destroy Temu, net margin declines to 10% | |||||||

| CNY millions | 2019 | 2020 | 2021 | 2022 | 2023 | 2024F | 2025F |

| Revenue | 30,142 | 59,492 | 93,950 | 130,558 | 247,639 | 470,514 | 367,566 |

| % growth y-o-y | 97% | 58% | 39% | 90% | 90% | -22% | |

| Net income | (6,968) | (7,180) | 7,769 | 31,538 | 60,027 | 102,903 | 36,757 |

| % net margin | -23% | -12% | 8% | 24% | 24% | 22% | 10% |

| % growth y-o-y | 3% | -208% | 306% | 90% | 71% | -64% | |

Profit margins

Given management’s repeated warnings of lower profitability in the future, I estimate that PDD’s future net margins may fall back to the 5-10% range seen in 2020 and 2021, and currently experienced by Alibaba and JD.com.

In a world with slower growth but no additional tariffs, this translates into CNY 25-50 billion ($3.5-7 billion) in net profit, or middle-of-the road 17-33x P/E. In a world with tariffs, net profit falls in the range of CNY 18-35 billion ($2.5-5 billion), putting the stock at a more expensive 24-48x P/E multiple.

Conclusion

PDD Holdings’ best days may be behind it, as the company faces intensifying competition and political scrutiny and warns of higher investments and lower profits ahead. Given how susceptible Chinese internet giants are to domestic and international political winds, investors should heed these warnings and be wise to sell the stock. In a bear case scenario, PDD can reasonably see lower revenues and lower profits that make the current share price expensive.

Read the full article here

")

")

")