")

")

Shares of global women’s healthcare concern Organon & Co. (NYSE:OGN) are up approximately 90% since making an all-time low in December 2023, when they were trading at a P/E on FY24E EPS of 2.4. The Merck (MRK) spinoff appears to have a clear vision to leverage its robust commercial and manufacturing footprint to purchase territorial rights to established brands and create biosimilars. With a significant debt load, a 5.3% current yield, flattish sales for its three years as a public concern, and still compressed valuation metrics, Organon merited a deeper dive. An analysis follows below.

Seeking Alpha

Company Overview

Organon & Co. is a Jersey City, New Jersey based global healthcare concern with a portfolio of more than 70 medicines and products with a primary focus on women’s health. In addition to its feminine offerings, the company markets five immunological or oncological biosimilars and a line of established branded therapies. Organon was founded in The Netherlands in 1923, acquired by Schering Plough in 2007, and spun out of Merck in 2021, with its first regular-way trade conducted at $34.15 a share. Its stock currently trades around $21.00, translating to an approximate market cap of $5.4 billion.

Approach

When it separated from Merck, Organon took with it Nexplanon, a uterine insert designed to prevent ovulation, as well as three biosimilars, a stable of medicines from the parent’s diversified brands division, a significant manufacturing footprint, and world-class commercial capabilities with a reach into more than 140 countries. Since the spin out, the company has attempted to leverage its expansive manufacturing (six sites) and sales footprints by purchasing the commercial rights to approved medicines in what it deems heretofore unexploited geographies from other pharmaceutical concerns, many of them – like the ones bequeathed from Merck – established brands that have lost or are close to losing patent exclusivity.

Revenue Disaggregation

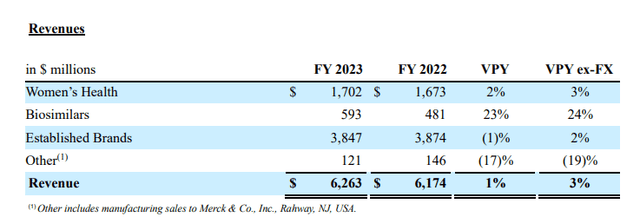

As alluded to above, management breaks out its revenue line by Women’s Health, Biosimilars, and Established Brands.

FY2023 Company Report

Women’s Health is dominated by Nexplanon, the sales of which accounted for 49% ($830 million) of the category’s FY23 top line of $1.70 billion. The three-year insert is set to come off U.S. patent protection in 2027 and in other countries as early as 2025. That said, there are currently no material contested proceedings regarding Organon’s rod technology patent and management is confident that it will suffer no loss of exclusivity for an additional three years due to an anticipated obtainment of a differentiated (five-year insert) label. Organon settled a key litigation matter around these Nexplanon challenges in late 2023 just before the case was to start a trial. Other nine-figure contributors to Women’s Health in FY23 included NuvaRing (contraception), Marvelon/Mercilon (contraception), Follistim AQ (fertility), and ganirelix acetate injection (fertility). The FY23 net sales from its 14 products was up 2% versus FY22.

FY23 top-line contribution from its five biosimilars were primarily comprised of inflammatory disease med and Remicade knockoff Renflexis, which delivered $278 million, up 23% versus FY22, and HER2-overexpressing cancer med and Herceptin knockoff Ontruzant, which generated $155 million, up 28% over FY22. Owing to the performance of these two biosimilars, the category, which includes three other inflammatory meds including Humira biosimilar Hadlima, experienced a 23% boost in sales over FY22 to $593 million.

Established Brands consists of 55 products that are either past or in some cases close to the end of their market exclusivity, but Organon can lean into its low-cost manufacturing capabilities, well-established supply chain, and low promotional costs to generate solid gross profits from these offerings in spite of generic competition. The category possessed eleven therapies that generated FY23 net sales of at least $100 million, led by cholesterol med Atozet ($519 million) and oral asthma med Singulair ($404 million), with LDL lowering drug Zetia, hypertension therapies Cozaar/Hyzaar, inhaled allergy corticosteroid Nasonex, and arthritis med Arcoxia all responsible for sales north of $250 million. By far and away Organon’s largest category, Established Brands contributed FY23 net sales of $3.85 billion, representing 63% of total and down 1% from FY22.

In its three years since going public, the company has produced top lines (which also include a de minimis ‘other’ category) of $6.30 billion, $6.17 billion, and $6.26 billion, with Adj. gross margins of 64.7%, 65.7%, and 62.7% in FY21-FY23, respectively.

Although those metrics are very consistent to date, there were plenty of ebbs and flows behind them, which will most certainly continue. Most notably, in FY24, patent expirations for Atozet and asthma med Dulera should negatively impact net sales by ~$80 million, while China’s volume-based drug procurement program (designed to promote generics) will hurt by ~$40 million. Management is countering those headwinds with several moves, including onboarding the European rights to Eil Lilly’s (LLY) migraine meds Emgality and Rayvow for an upfront consideration of $50 million and potential milestones of $170 million in 1Q24. Organon anticipates achieving peak sales from Emgality of ~$170 million. The company also expects a growth spurt from autoimmune disease monoclonal antibody Hadlima, a biosimilar of $21 billion mega-blockbuster Humira, which replaced the latter on the Veterans Administration formulary in April 2024. It also anticipates postpartum uterine bleeding device Jada System and Nexplanon to contribute to growth in FY24.

Entering the year, Organon forecasted delivering FY24 Adj. EBITDA of $2.0 billion on net sales of $6.35 billion with Adj. gross margin of 62%, based on range midpoints.

1Q24 Financials

That outlook did not change when the company reported 1Q24 financials on May 2, 2024, posting non-GAAP earnings of $1.22 per share and Adj. EBITDA of $538 million on net sales of $1.62 billion, versus $1.08 per share (non-GAAP) and Adj. EBITDA of $518 million on net sales of $1.54 billion in 1Q23, representing improvements of 13%, 4%, and 5% (7% constant currency) over the prior year period, respectively. A 33% rise in Nexplanon net sales to $220 million and a 46% surge in Biosimilar sales, led by Hadlima and Ontruzant, to $170 million were responsible for the increase at the top line. Adj. gross margin was down 310 basis points to 62.1% versus 65.2% in the prior year period as cost inflation and unfavorable product mix hurt.

That said, Organon’s bottom line beat Street consensus by $0.29 and its top line was $61.8 million better, sparking an initially muted 4% rally to $19.50 in the subsequent trading session. However, that close was the lowest since, with shares of OGN trading as high as $21.98 on May 17 and 22, 2024, marking a 103% rally since nadiring at an all-time low of $10.84 in December 2023.

Second Quarter Results:

Organon posted its Q2 numbers on August 6th. They were mixed. The company delivered non-GAAP profits of $1.12 a share, four pennies a share above expectations. GAAP earnings were 75 cents a share for the quarter. Revenues were flat on a year-over-year basis at $1.61 billion, around $10 million light of the consensus forecast. On a constant currency basis, revenues were up two percent from the same period a year ago, it should be noted.

August 2024 Company Presentation

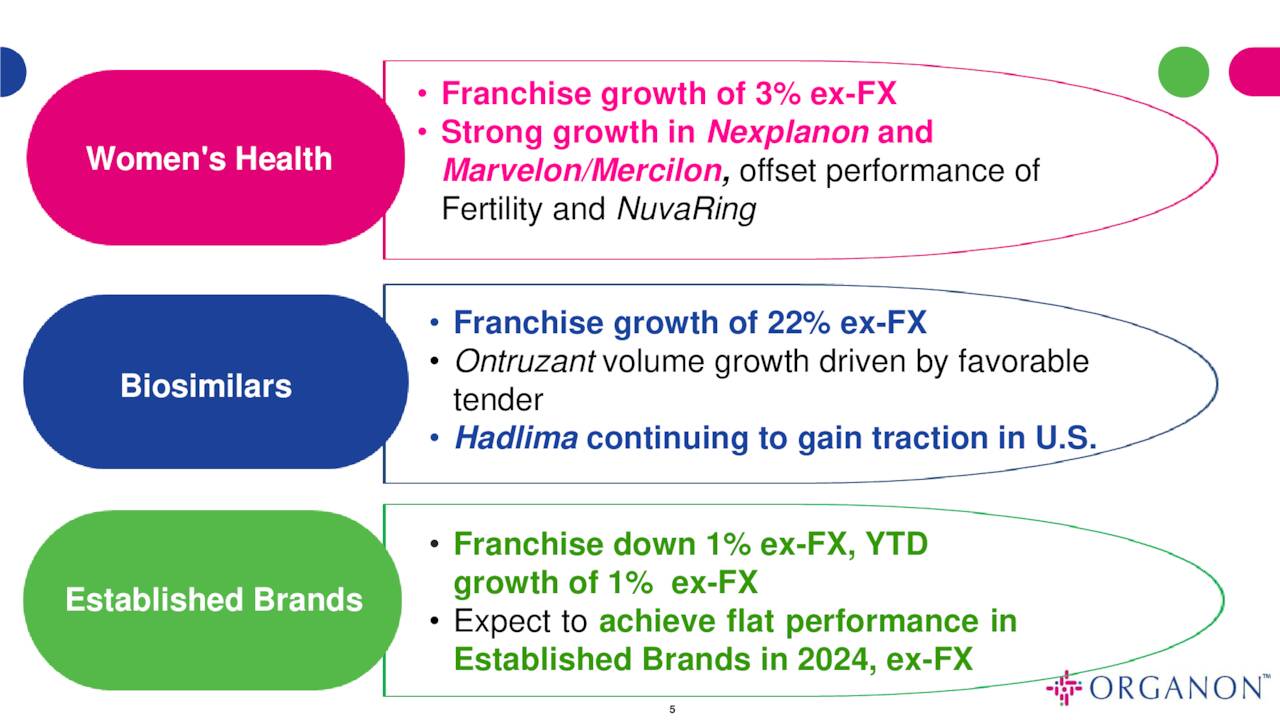

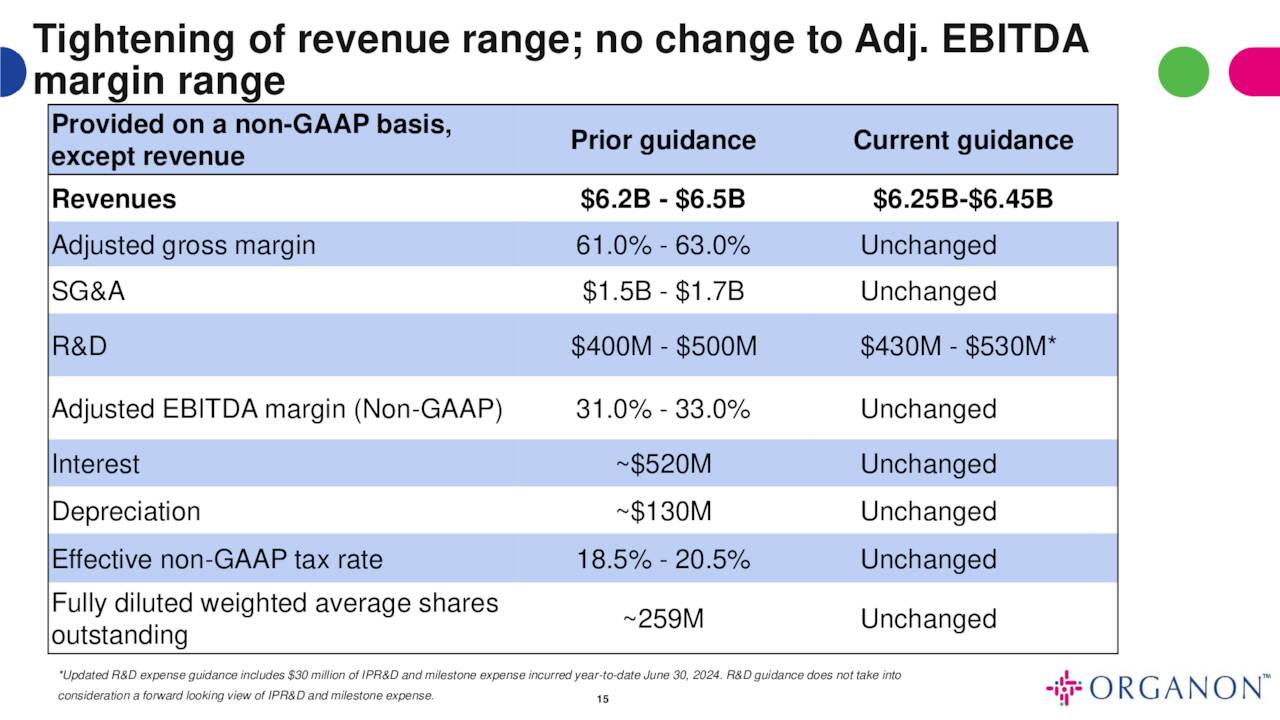

Biosimilars continued to be a key growth engine for Organon, posting a 22% rise over 2Q2023 with sales of $164 million. Women’s Health sales gained a much more modest three percent to $449, while revenues fell at the company’s Established Brands by three percent to $963 million. Management provided the following narrowed FY2024 guidance along with second quarter results.

August 2024 Company Presentation

Balance Sheet & Analyst Commentary

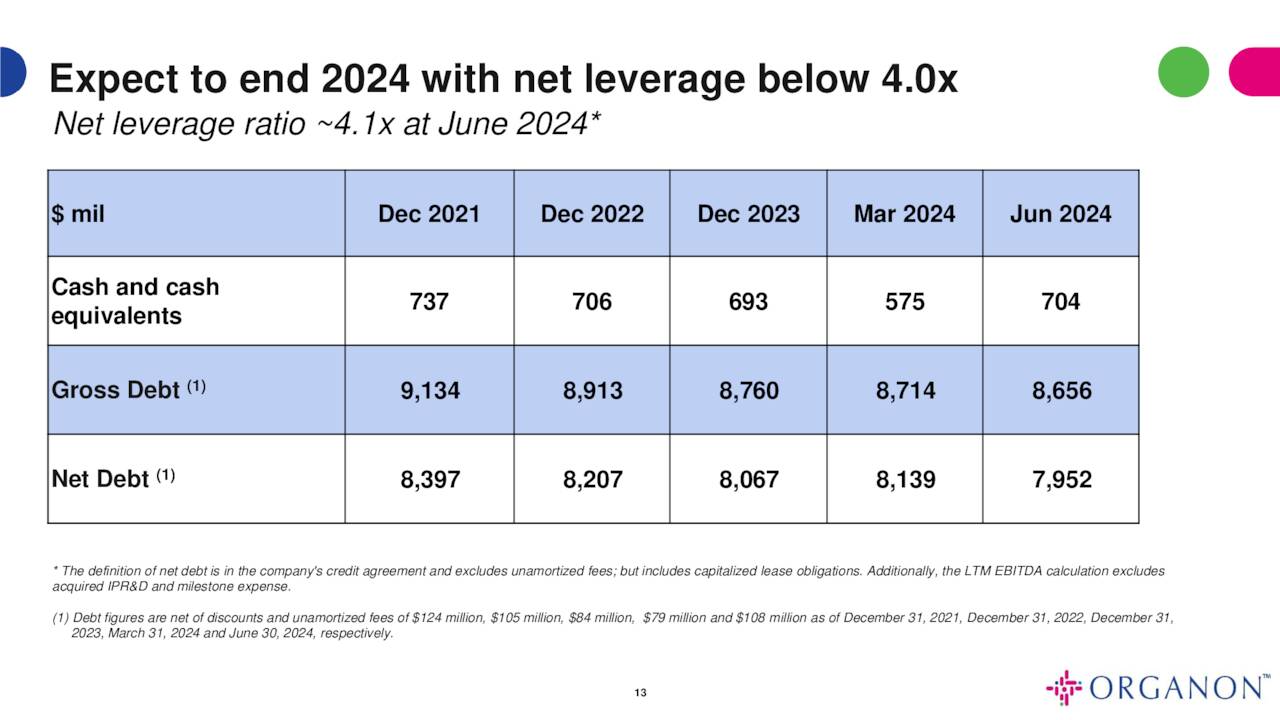

One of the reasons for the negative sentiment surrounding the company in late 2023 was its balance sheet. When Merck spun out Organon, it also saddled it with long-term debt of $9.3 billion. As of the end of the first half of 2024, the company held debt of $8.656 billion (almost all of it due 2028 or 2031) against cash of $704 million for net leverage of 4.1. In May 2024, management refinanced $1 billion of debt due 2028 with debt due 2034. With that level of obligation, Organon’s generous quarterly dividend of $0.28 a share (for a yield of 5.3%) has caused speculation that its cash could eventually be reprioritized to paying down debt. That said, management appears very committed to the dividend and currently has adequate cash flow to service it. That said, the company is on track to deliver approximately $1 billion in free cash flow in FY2024 before adjusting for spinoff costs.

August 2024 Company Presentation

The analyst community is not currently enthusiastic on Organon’s prospects. Since second quarter results have hit the wires, Goldman Sachs ($20 price target) and Morgan Stanley ($18 price target) have maintained hold ratings on the stock and Bank of America reissued its Sell rating on OGN. Only Barclays ($26 price target) has reissued a Buy rating so far, post earnings. On average, they expect the company to earn $4.36 a share (non-GAAP) on net sales of $6.38 billion in FY24, followed by $4.51 a share (non-GAAP) on net sales of $6.44 billion in FY25.

One insider bought nearly $50,000 worth of equity in February of this year. That is the only insider activity in the stock I can find since the spinoff.

Verdict

If Organon wasn’t so loaded with debt, its gambit of buying established brands or creating biosimilars and leveraging its commercial operations to market them would command much higher multiples. However, with ~$525 million in annual interest payments on its debt, multiples are compressed. The company’s stock trades at a microscopic PE on FY24E EPS of 4.8 and that is with it up over 90% since bottoming in December 2023 when its FY24E PE was 2.4. Even factoring in the company’s significant debt, its EV/TTM Adj. EBITDA is still just under seven. The recent rally and debt load are the two reasons OGN is not a name I would take a huge stake in. If the shares drift back down to the mid to high teens and/or management makes good progress reducing the company’s leverage, that may change in the future.

For the avoidance of doubt, under its business model, management will always be engaged in finding the right established brands to fit its commercial and manufacturing operations as generics eat into sales, adding a layer of uncertainty to its ability to execute, which also compresses valuation multiples. That said, as the adage goes, the easy money has been made in Organon, but with a safe current yield of 5.3%, and projected earnings and EBITDA metrics that suggest limited downside, it appears to be a solid value holding.

I have taken a small stake in OGN via covered call orders. The option premium obtained via this simple option strategy adds to the yield of this equity and provides a bit of additional downside protection.

Read the full article here

")

")