")

Investment Thesis

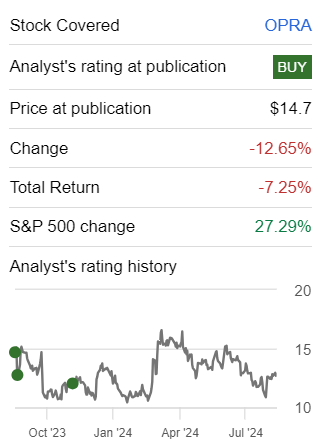

Opera Limited (NASDAQ:OPRA), which provides the contentious tier-3 browser, reported solid results that beat on the top line and the bottom line and raised its full-year guidance.

What’s more, the stock looks incredibly cheap at 10x this year’s EBITDA, with no debt, all the while paying out a 6.1% dividend yield.

But is this stock a value trap? I don’t believe so. As such, I remain bullish on OPRA as I’ve done for some time.

Rapid Recap

Last year, in November, I said,

I’ll get to the punch line first, and then you’ll see the reasoning behind my assertion. I believe that Opera is attractively priced at 14x forward free cash flows. Even though the investment thesis isn’t blemish-free, there’s a lot to like.

What’s more, given its annualized $0.80 dividend per share, which equates to nearly 7% yield, I believe this should further support my bull case.

Author’s work on OPRA

Opera is a stock that I’ve been bullish on for a while. And for a long time, this stock has failed to live up to my expectations. And even as I openly describe some concerns investors have with Opera, I maintain that this stock is reasonably priced. Here’s why I’m still bullish on Opera.

Why Opera? Why Now?

Opera Holdings creates web browsers that people use to surf the internet. Their browsers are designed to be fast and secure, offering features like ad-blocking, free VPN services, and a built-in cryptocurrency wallet.

Opera seeks to provide a more rounded browsing experience including AI-powered tools, aimed at improving users’ online experience.

Essentially, it’s often noted that Opera is better than its big competitors’ search engines when it comes to servicing users who value privacy online.

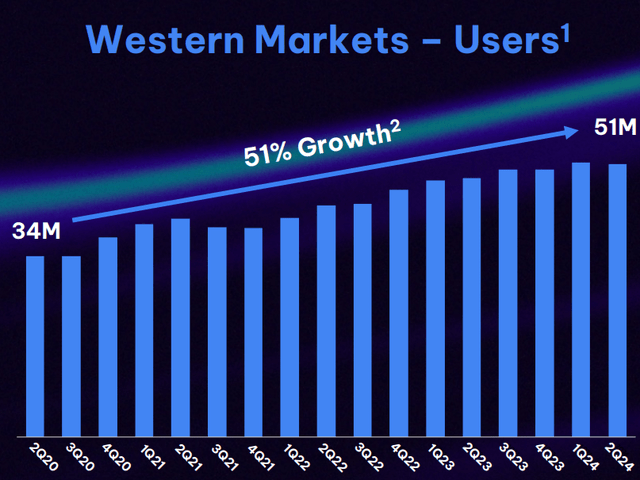

OPRA Q2 2024

And yet, despite all of management’s efforts to focus on its higher-valued Western Markets users, it appears that its user base has started to stagnate, see above.

But it’s not all bad when it comes to Opera. On the contrary, there’s a lot to like here.

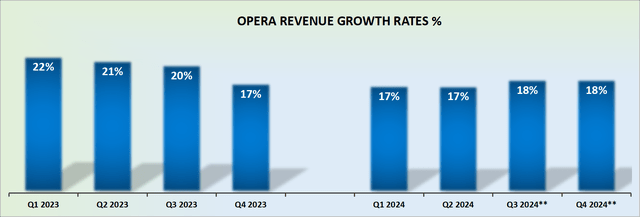

Revenue Growth Rates Stabilize

OPRA revenue growth rates

Opera raised its guidance yet again. It is now expected to deliver around 18% CAGR in the second half of 2024. What’s more, looking ahead to 2025, given the slightly easier comparable quarters, it’s highly likely that Opera could be growing in the high teens for some time.

With this framework in mind, let’s now discuss the crown jewel of this investment thesis, namely its valuation.

OPRA Stock Valuation — 10x This Year’s EBITDA

Right away, keep in mind that Opera’s market cap is made up of approximately 10% cash and cash equivalents, with nil debt. This provides the business with ample flexibility to either reinvest in its operations or to weather a slowdown in the economy.

Moreover, Opera pays out a semi-annual dividend that yields approximately 6.1%.

And finally, investors are asked to pay about 10x this year’s EBITDA. Altogether, this strikes me as a rather attractive multiple to get involved in this stock.

Risks to My Investment Thesis

Opera is not risk-free. That much is obvious. For example, tremendous competition from Google (GOOG, GOOGL) and Bing (MSFT) needs to be considered.

Case in point, Google’s dominance and its substantial resources allow it to consistently innovate, making it a formidable competitor, with an expansive moat.

For its part, Opera must continuously defend its small, low single-digit market share, and the pressure to differentiate its product offerings from Google’s is immense.

If Opera fails to keep pace with Google’s product innovations, no investors will put a high premium on stock, as investors’ confidence will be consistently in check.

This leads me to another key assumption. Sometimes stocks that are cheap for a reason and remain cheap.

While Opera’s stock might be trading at a lower price point compared to its Google, this does not necessarily imply that the stock is undervalued. The competition against Google could justify its present valuation.

Finally, Opera needs not only to defend its market position but also deliver strong positive growth surprises beyond expectations. Basically, investors need to buy into the idea that Opera could in the near and medium-term take market share away from Google. Because for now, this is a tier-3 browser, and it could be considered deserving of a low multiple.

The Bottom Line

Paying 10x EBITDA for Opera Holdings strikes me as a reasonably attractive proposition, especially given its solid financials, including no debt and a generous 6.1% dividend yield.

This valuation offers a fair entry point for investors who believe in Opera’s ability to maintain and grow its market position, despite the fierce competition from industry giants like Google. However, the key risks remain—Opera must continue to innovate and grow its user base, or it risks being overshadowed by competitors.

While the stock’s low price may raise concerns about a value trap, I believe Opera has the potential to hit the right “notes” for patient investors.

Read the full article here