")

")

The stock price of Oaktree Specialty Lending Corporation (NASDAQ:OCSL) is down 8% as I am writing this, in response to the business development company reporting fourth quarter results.

The earnings snapshot showed a large increase in the BDC’s non-accrual ratio which in turn caused a panic sell-off that I exploited by increasing my position in Oaktree Specialty Lending by 25%.

I think investors overreact to the increase in non-accruals and with the yield now standing solidly above 11% again, I am modifying my stock classification to Strong Buy.

The premium to net asset value has almost completely vanished and I think the risk/reward relationship has quite considerably improved.

My Rating History

My most recent stock classification of Oaktree Specialty Lending was Hold with the reason being that the discount to net asset value disappeared.

Oaktree Specialty Lending’s earnings release pointed to some credit quality issues in the BDC’s debt investment portfolio, but the BDC deserves the benefit of the doubt as it continued to cover its 0.55 per share per quarter dividend with net investment income.

Portfolio And Credit Issues

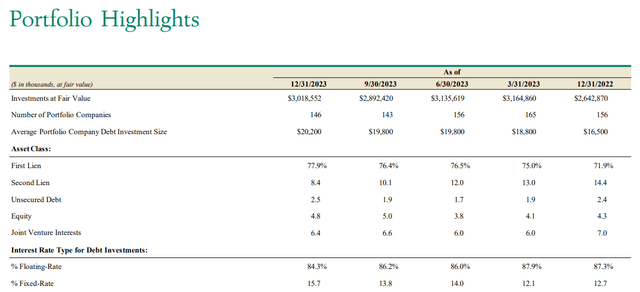

Oaktree Specialty Lending is a middle market-focused business development company organized under the Investment Company Act of 1940. The BDC invests primarily in First and Second Liens, Unsecured Debt and Equity and had 84% of its investments allocated to floating-rate investments as of the end of 1Q-24 (the December quarter).

Oaktree Specialty Lending’s total portfolio was valued at $3.0 billion and the BDC originated net new investments in the amount of $154.1 million in the last quarter. Robust originations were the reason why Oaktree Specialty Lending’s portfolio value was up 4.4% QoQ.

Portfolio Highlights (Oaktree Specialty Lending)

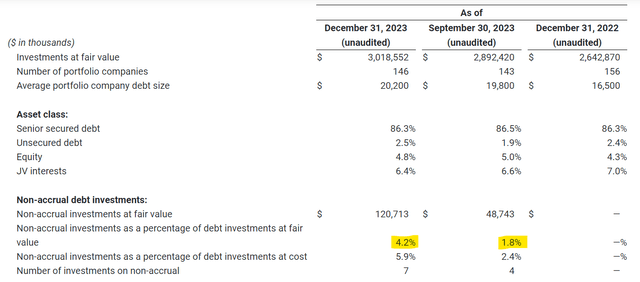

The biggest elephant in the room as far as Oaktree Specialty Lending’s earnings are concerned was a deterioration in the company’s credit quality: The BDC added a total of three investments to its non-performing roster in the last quarter.

Oaktree Specialty Lending’s non-accrual ratio, which is an indicator of loan quality and portfolio income stability, increased to 4.2% based on fair value, up from 1.8% in the prior quarter.

Non-Accrual Ratio (Oaktree Specialty Lending)

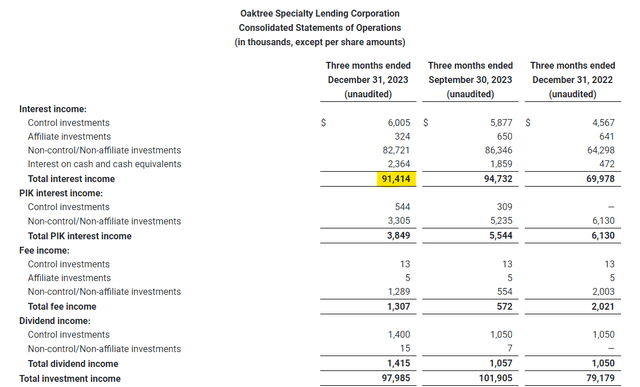

The increase in non-accruals triggered a decrease in Oaktree Specialty Lending’s total interest income which fell 3.5% QoQ to $91.4 million in the last quarter. All things considered, however, Oaktree Specialty Lending’s portfolio income was sufficient to cover its dividend pay-out of $0.55 per share per quarter.

Total Interest Income (Oaktree Specialty Lending)

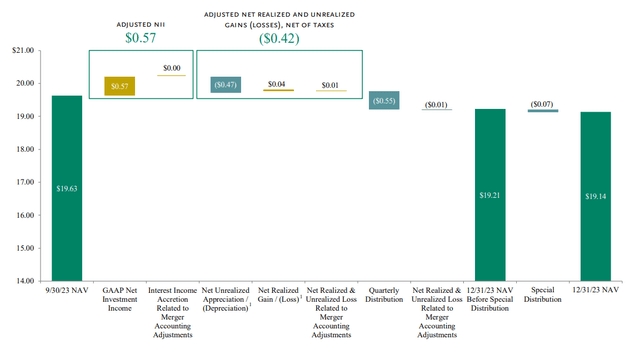

Though the dividend remained covered by net investment income, the credit issues affected the company’s net asset value due to the impact of realized/unrealized investment losses in the amount of $0.42 per share. Mainly because of the deterioration of credit quality, Oaktree Specialty Lending suffered a 2.5% QoQ drop in its net asset value.

With that being said, I think the increase in the non-accrual ratio triggered an overreaction in the market that passive income investors can now take advantage of.

Net Asset Value (Oaktree Specialty Lending)

Dividend Coverage Ratio Deteriorated

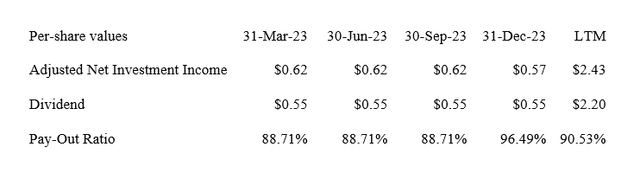

Oaktree Specialty Lending earned $0.57 per share in adjusted net investment income in the last quarter which reflected a decline of 8% compared to the prior quarter. In 2023, Oaktree Specialty Lending earned $2.43 per share in adjusted net investment income while paying out $2.20 per share in dividends.

Due to Oaktree Specialty Lending’s credit issues, the BDC suffered an uptick in its dividend pay-out ratio which rose from a stable 88.7% to 96.5%. Though the increase in the pay-out ratio is not great, obviously, Oaktree Specialty Lending did cover it with net investment income and the dividend is not imminently at risk, in my view.

Dividend (Author Created Table Using BDC Information)

OCSL Is Selling At A Much Lower Premium To Net Asset Value Again

One reason why I modified my stock classification for Oaktree Specialty Lending to Hold in November was that the stock was no longer trading at a discount to net asset.

Oaktree Specialty Lending’s net asset value at the end of the last quarter was $19.14 which means the premium to net asset has almost completely disappeared.

With a stock price of $19.48, Oaktree Specialty Lending is selling for a mere 2% premium to net asset value as opposed to a 10% premium two days ago.

I think that Oaktree Specialty Lending has a very compelling valuation here and I am modifying my stock classification to Strong Buy as a consequence.

Most BDCs that I have in my portfolio, or for which I provide coverage, are selling for about net asset value.

Headwinds To The Oaktree Specialty Lending Investment Thesis

Passive income investors that are buying the drop have to pay close attention to Oaktree Specialty Lending’s non-accrual ratio moving forward because it could indicate that they will see a further deterioration in the dividend pay-out ratio. If the pay-out ratio exceeds the dividend pay-out, the dividend might get slashed.

My Conclusion

Oaktree Specialty Lending’s stock is taking a beating right now in response to the BDC disclosing some credit issues in its debt investment portfolio which in turn led to an increase in the BDC’s non-accrual ratio.

Though the jump in the non-accrual ratio was a negative, I think that the earnings release as a whole was not that bad as the BDC continued to cover its dividend with net investment income and the increased risk in the portfolio is now reflected in a more attractive NAV multiple.

If you pull the trigger on OCSL today (as I just did), you can get an 11% dividend yield again, which as I said, is still covered by net investment income. Strong Buy.

Read the full article here

")

")