")

Q4 2024 Earnings Call Transcript")

")

")

Investment Rundown

The stock price of Noble Corporation plc (NYSE:NE) has been on quite the rollercoaster for the past 12 months. Back in late June of 2023, the company was rated as a buy from Citi and the impacts of the production cuts OPEC made began to show on the earnings reports and performance of companies, but also the price of oil on the global markets. This meant that the price of NE shot up from $38.5 per share to over $52 in the span of a few weeks. Since then, there has been a steady decline for a lot of energy companies as oil prices haven’t quite risen rapidly, much seemingly because of increased production outputs in the US, primarily the Permian Basin.

The dividend and the guidance by the company were raised significantly in the last report the company announced, and we are now less than a month out until the next one is released. I think the performance of NE has been strong, and following the steady decline of the stock price I think an appealing entry point has revealed itself right now. I am beginning to cover NE and my initial rating will be a buy for the company.

Company Segments

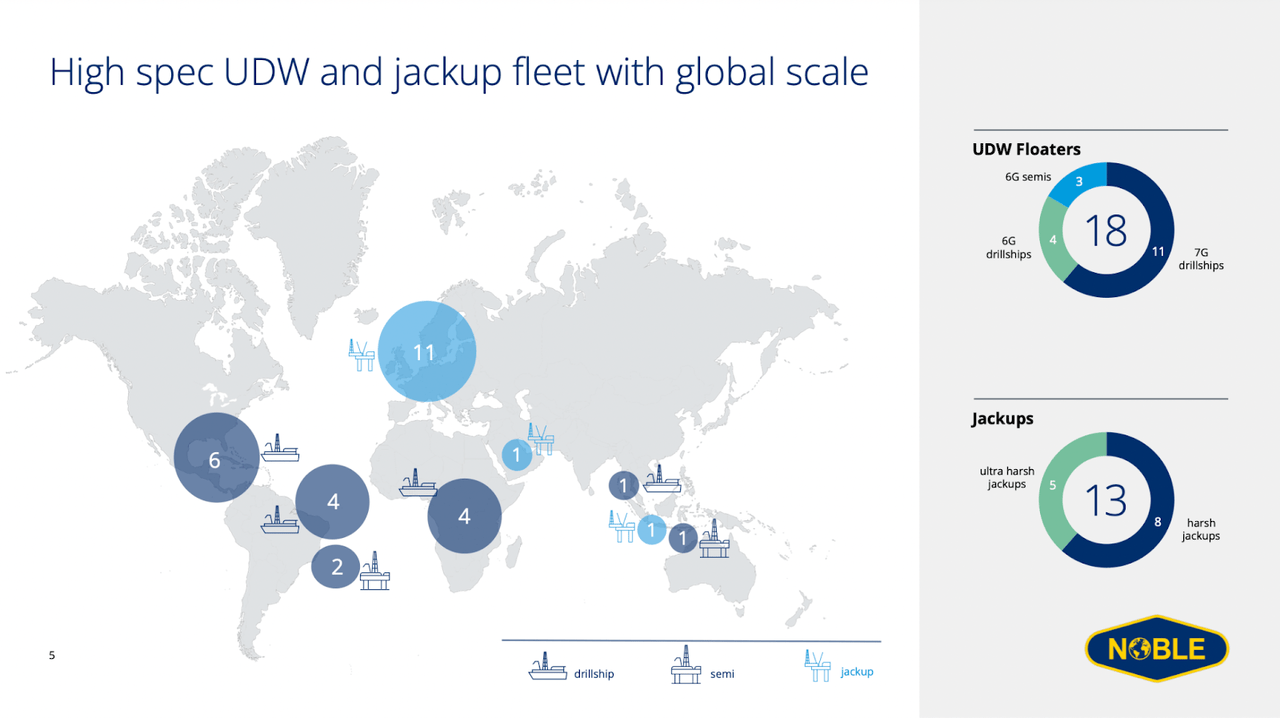

NE is a company operating as an offshore drilling contractor with operations spanning globally. The company was founded in 1921 and has been readily growing since to a valuation of $6.3 billion as of now. As far as operations go, the primary one is in the North Sea with partnerships like Aker BP following a successful deal in January of 2023. Now the jackup sites are 11 in the region which makes it one of the most important to follow I think.

Market Overview (Investor Presentation)

The company’s journey through corporate restructuring, acquisitions like Frontier Drilling and Pacific Drilling, and strategic mergers, including the merger with Maersk Drilling, has shaped its current stature in the industry. Despite facing challenges like filing for bankruptcy in 2020, Noble emerged stronger in 2021and revenues and earnings have been growing since. In 2015 the revenues for the company reached over $3.2 billion and right now it seems NE is heading right back to those levels once again as TTM revenues are $2.4 billion. The merger helped improve the company’s position in the market and likely led to successful backlog increases which boosted total asset value as well to just over $1 billion. As far as returns on these assets NE has an ROA of 8.87%, 22.85% higher than the energy sector’s average.

Markets They Are In

It seems one of the fastest growing markets in the energy sector, and more specifically related to oil is the offshore drilling market. Expected to reach a valuation of $65 billion in 2030 and grow at a CAGR of 8.7% from now until then. The primary tailwinds I think that are contributing to this is the increased need for energy in the world. Oil remains to be one of the primary ways of energy generation and it will likely stay that way for a very long time, even if there are a lot of investments going into renewables. Phasing out traditional ways of generating energy like oil and gas is expensive and time-consuming. For me, this all means there is still a lot of value to be had in the sector, through both appreciations of the value of a position, but also strong shareholder incentives like buybacks and dividends. These incentives are present with NE as they raised the dividend by 33% to $0.4 quarterly putting it at an FWD yield of 1.56%. Another key tailwind for the industry revolves around the reduction of costs for Unmanned Wellhead Platforms which should make offshore drilling even more profitable, and drive demand for a company like NE even higher.

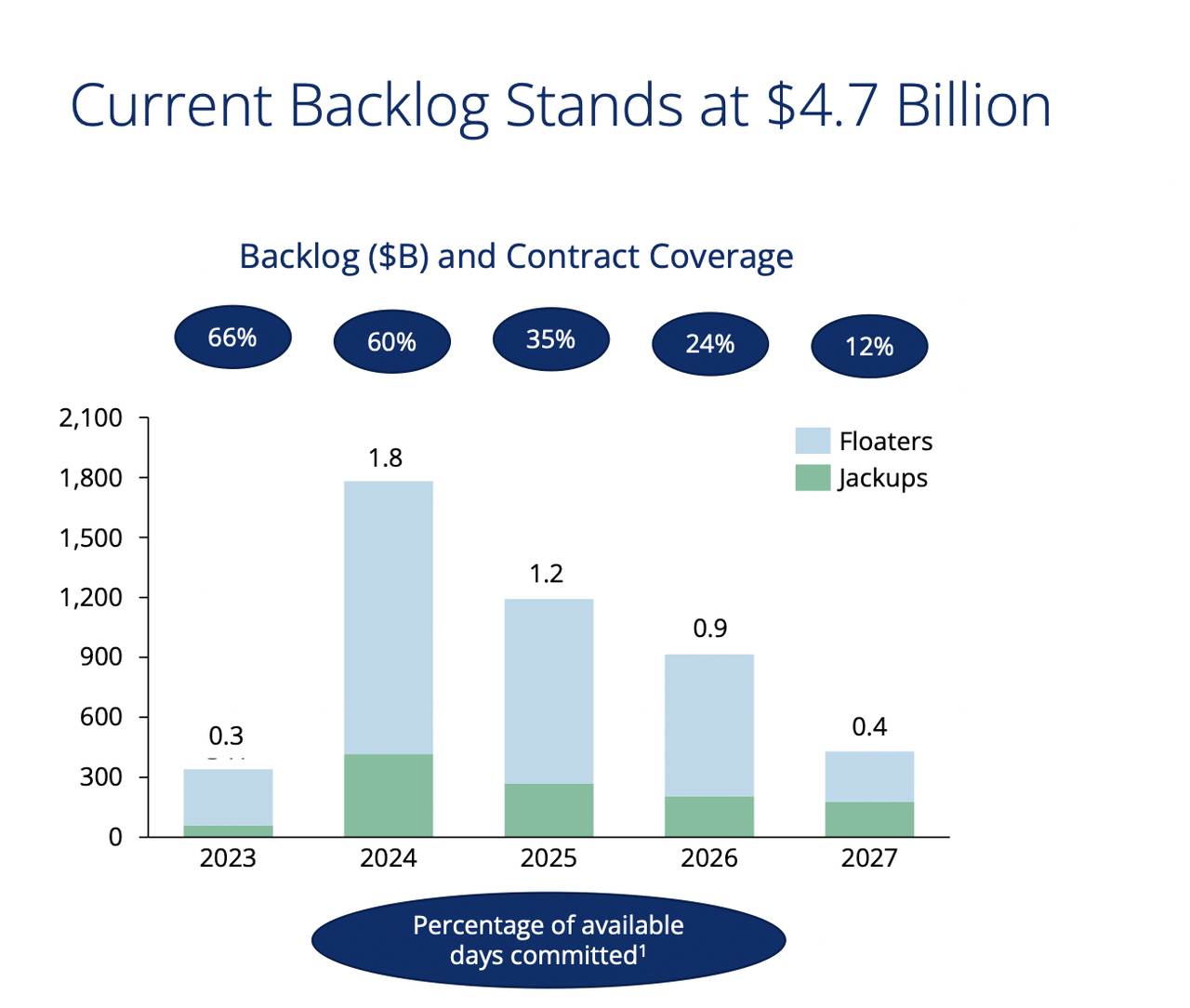

Backlogs (Investor Presentation)

One of the areas that has been a key focus for NE in the past years is building up a strong backlog. The backlog is now valued at $1.8 billion going into 2024. The CEO of the company Robert Eifler had the following to say about it last quarter: “Following the dividend initiation last quarter, we have signed additional contracts to bring our 2024 scheduled backlog to $1.8 billion currently with near-term visibility to additional bookings that could increase 2024 backlog to over $2 billion. So, we have decided to make this upward revision just one quarter after the dividend initiation”.

I think this comment displays the intuition that NE has taken to build out its reach and partner with big players in the industry like Exxon Mobil (XOM). NE received additional strong backlogs for operations in South America, a region where NE doesn’t have its primary operations, but a significant amount with 6 semis in the region. The comment the CEO made indicates strong demand in the industry which could lead to even higher backlogs to finish 2024 off. The start of the year had energy stocks struggle and many big companies are down YTD. I think there will be a recovery as most of the focus has been on big tech these last few weeks instead as earnings season is intensifying. Following that I think we might see a recovery for energy stocks, making NE right now a pretty decent bet on that I think.

Earnings Highlights

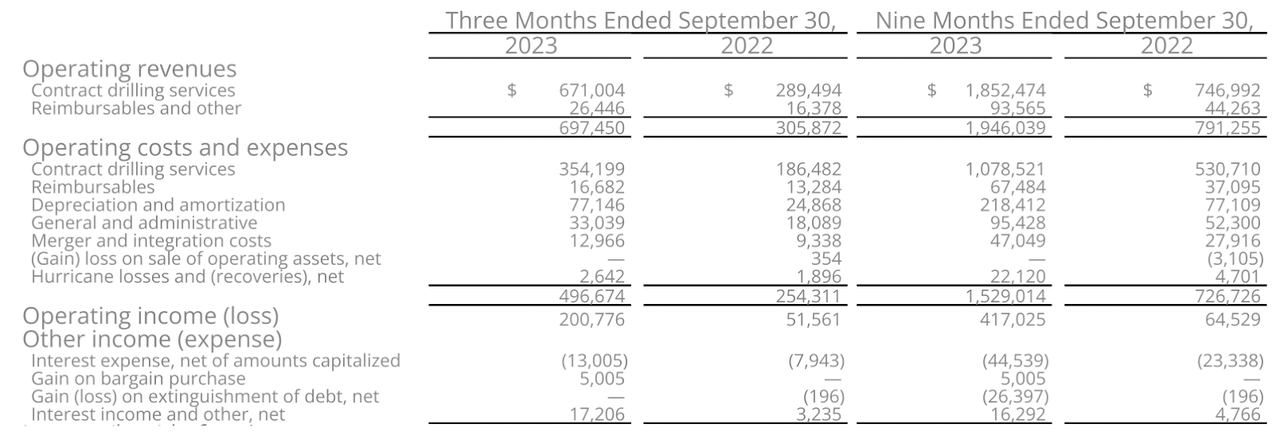

Income Statement (Earnings Report)

The third quarter meant strong results for NE as it increased both its dividend and its guidance for the year. The dividend was for example raised to $0.4 quarterly putting it an annualized dividend of $1.6 or a yield of 1.56%. The full-year adjusted EBITDA now is $775 – $825 million putting it at the top end of the previous range the company had.

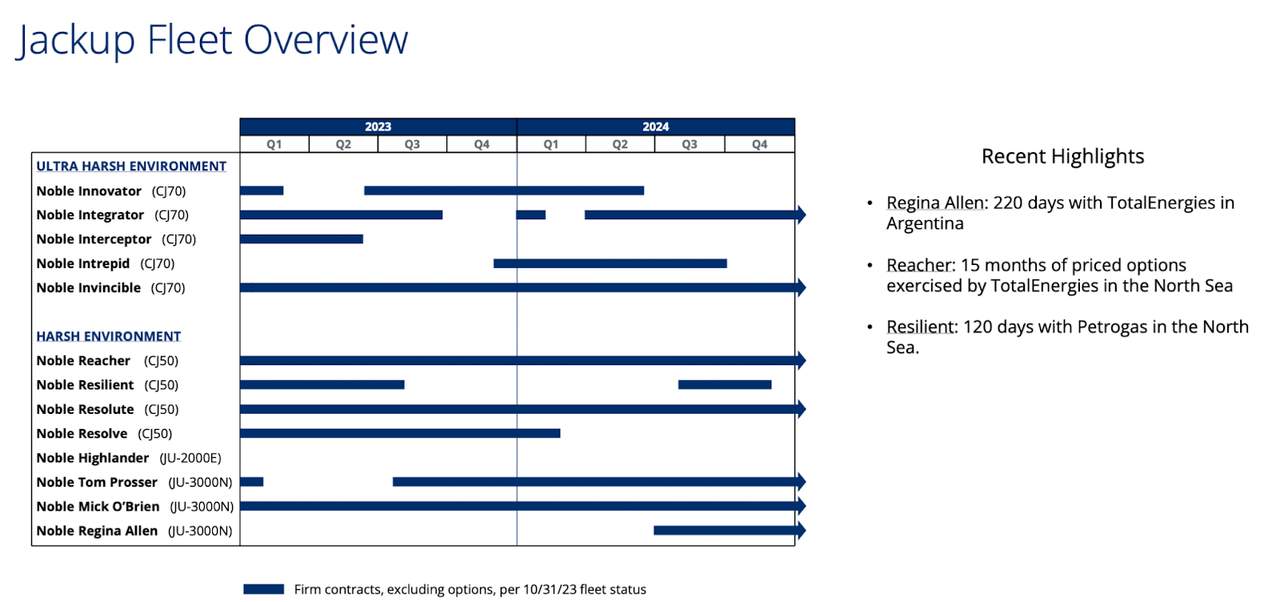

Fleet Overview (Investor Presentation)

One of the biggest and also one of the riskier segments of NE is its Norway operations. The CEO Robert had some comments to share in the last report about it: “Within Norway, the timing of demand recovery continues to be hard to predict. At this point, we remain generally cautious about the outlook for this market through 2024. Thus, our idle CJ70 jackup Noble Interceptor is still confronted with a limited opportunity set”. These struggles have been shown as the rig utilization rates have fallen quite a lot of jackups, which is by a big majority existing in Norway. Falling from 82% to 62%. Following the quarter end though, NE has continued to show strong results I think as EPS reached $1.09 diluted, up impressively from $0.41 the same quarter in FY2022.

With less than a month away from the fourth quarter released, I will be looking at how NE manages to guide investors regarding its Norway operations. A positive outlook here I think will help boost the share price in the short-term, and strong results will lead to a more concrete valuation increase.

EPS Estimates (Seeking Alpha)

Speaking of valuations, NE is sitting quite high right now at a FWD p/e of 18, but with estimates that it will fall to 10.3 in 2024. These are estimates based on that NE can see both decreased operational expenses and for order backlogs to rise, whilst NE is also capable of finishing and delivering on a lot of it too. I lean towards this being a reasonable assumption given the positive outlook given by the management along with strong partnership announcements the past few years. With this type of growth, NE could deliver a very satisfying return of 10 – 12% over the long term in my opinion.

Risks

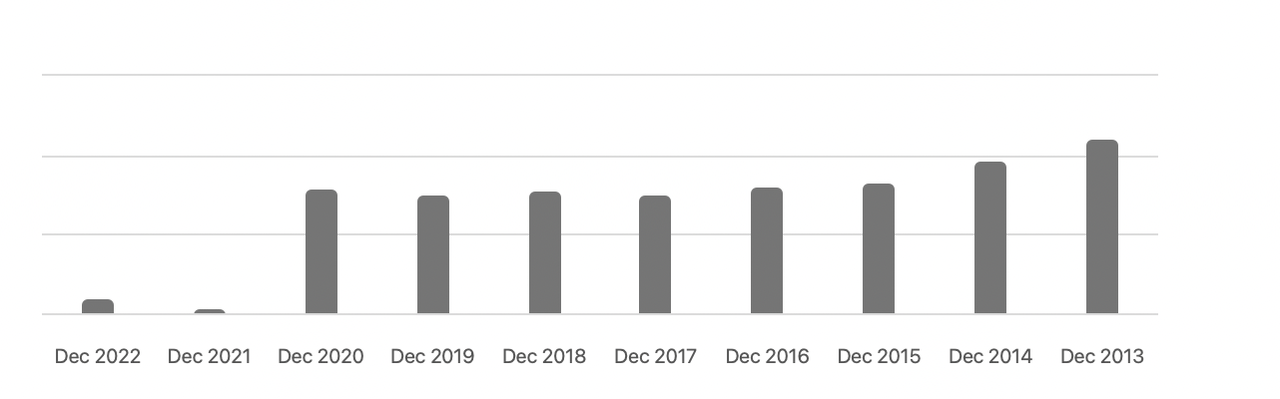

One of the primary concerns that investors had before 2020 was the extremely high debt levels of the company. Following the merger with Maersk Drilling, it helped heavily de-leverage the balance sheet and debt plummeted from $3.9 billion to under $300 million. But since then it has once again ballooned up to $585 million and this isn’t necessarily the move that I want to see NE making again.

Debt Levels (Seeking Alpha)

The company filed for bankruptcy and managed to erase $3.4 billion in debts as the price of crude oil plummeted during the pandemic. This brings me to the primary risk with an offshore drilling company. The expenses to run these operations are high and if prices are unstable on the markets it creates a lot of difficulties for expansion and paying down expenses of the business. NE experienced this in 2020 but I think they are in a better place now both financially and operationally. The backlog supports them very well and they have strong partnerships that will support them as well. Nonetheless, the primary risk with NE is about market volatility in crude prices, and investors should account for similar volatility in the stock price of NE too.

Final Words

I haven’t been covering NE before at all, but it’s an interesting company that is operating in the offshore drilling sector. In the past few years, the company has undergone quite a lot of changes, like emerging from a bankruptcy filing that helped deleverage the balance sheet by a large portion. But, NE has also managed to increase its backlog in a very healthy manner, now sitting at $4.9 billion. The energy sector has struggled so far in 2024 but I think NE stands as a very strong opportunity over the long term, even more so after falling from the 52-week high of $55.

Read the full article here

")

Q4 2024 Earnings Call Transcript")

")

")

")