")

")

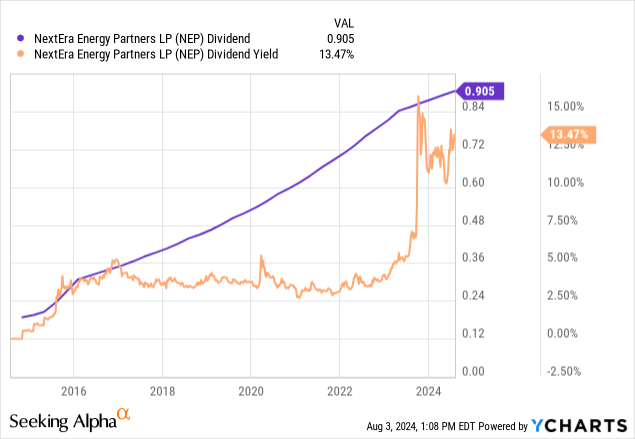

It’s not hard to see why NextEra Energy Partners (NYSE:NEP) is extremely attractive to dividend investors. The renewable energy company last declared a quarterly cash dividend of $0.905 per unit, kept unchanged from its prior distribution and $3.62 per share annualized for a 14% dividend yield. For some context, NEP’s 4-year average dividend yield stands at 5.7%. The yield was around 3% in the years preceding the pandemic. The current yield is extremely abnormal versus NEP’s historical range, reflecting well-formed fears over the sustainability of payouts against an outsized total debt position and a Fed funds rate that sits at a historical high. The fears come against NEP’s guidance to grow its distribution per common unit at a 5% to 8% range through at least 2026. The stock dipped after the recent raise. What gives?

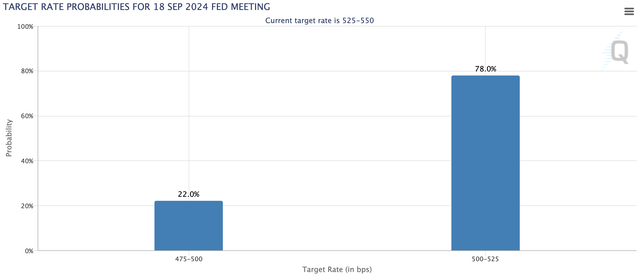

Morgan Stanley on downgrading NEP to underweight with a $20 price target cited a risk that the distribution will be cut as a core overhang on the stock. Hence, this is not an investment for the risk-averse, but I’ve taken a position here with the Fed set to deliver back-to-back interest rate cuts from September against US macroeconomic data that is increasingly flashing red for a recession. The debate around this has now shifted to whether or not the Fed will need a deeper 50 basis point cut, with the CME FedWatch Tool placing the probability of this at 22%. NEP’s dividend could be saved from a cut against this new upcoming zeitgeist that will disproportionately benefit companies with large floating rate debt. I last covered NEP last year in November.

CME FedWatch Tool

Is The dividend Safe?

Seeking Alpha

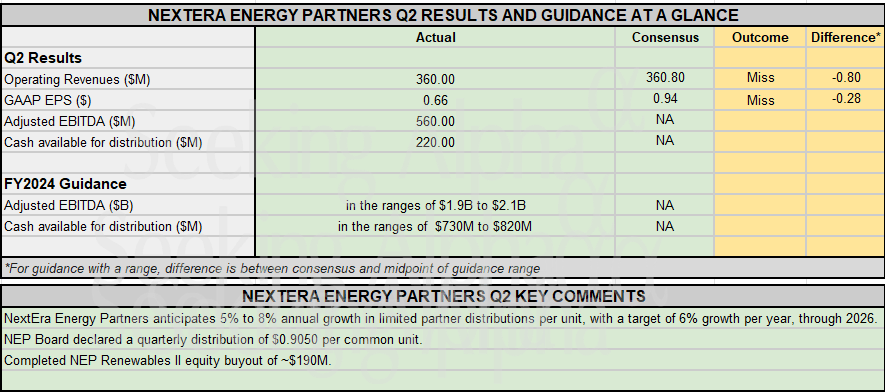

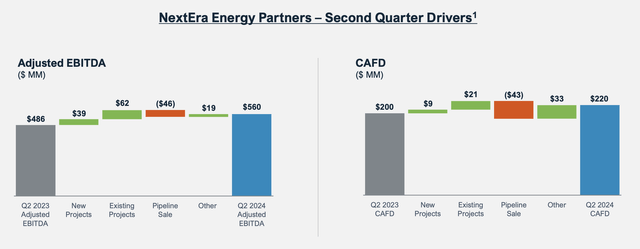

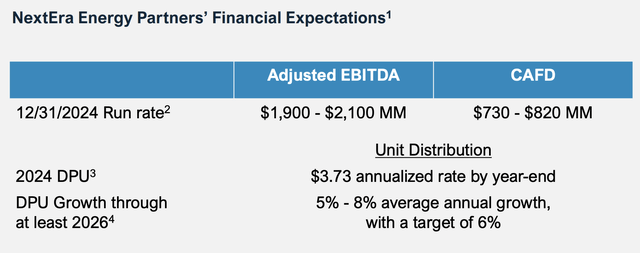

NEP’s fiscal 2024 second-quarter earnings saw the company bring in operating revenue of $360 million, up 22.9% over its year-ago comp but missing analyst consensus by $800,000. Critically, NEP generated an adjusted EBITDA of $560 million with cash available for distribution (“CAFD”) of $220 million. This was up 10% year-over-year. NEP has stated it won’t need an acquisition in 2024 to meet its 6% limited partner distribution growth target.

NextEra Energy Partners June 2024 Earnings Presentation

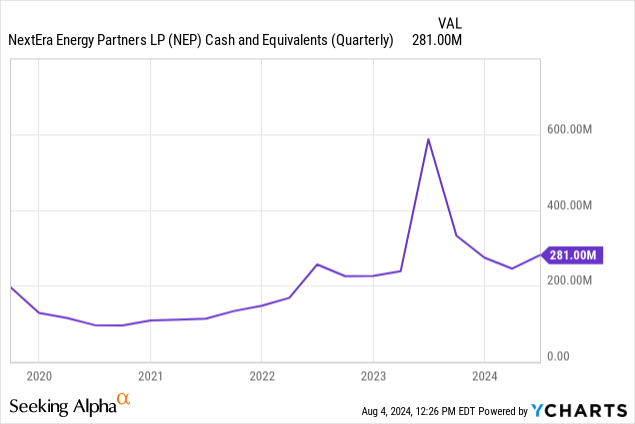

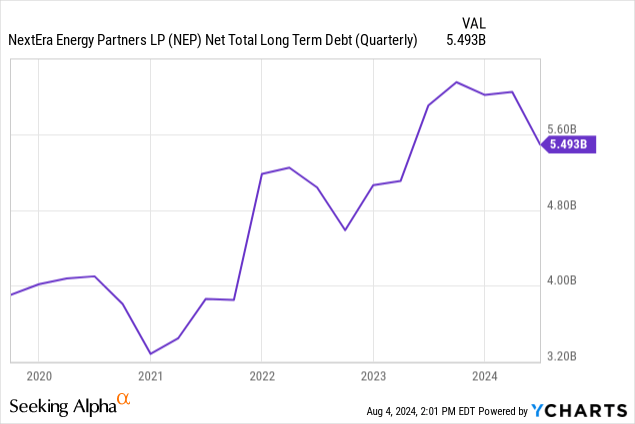

The company had 93.4 million common units outstanding at the end of its second quarter, placing its CAFD at around $2.35 per common unit for the second quarter. CAFD varies per quarter but CAFD generation during the second quarter was robust with NEP ending the quarter with total cash and cash equivalents of $281 million, down from $587 million a year ago but up $36 million sequentially from the first quarter. This is set against total debt of $5.77 billion.

NEP’s total debt balance drove an interest expense of $54 million for the quarter, up from $12 million a year ago. This forms the core headwind for NEP, with the renewable company set to face increased interest payments as it refinances maturing debt against a Fed funds rate that remains at a 23-year high of 5.25% to 5.50%.

However, NEP has already guided its distribution to shareholders to see growth for the next two fiscal years until the end of 2026. The company also held liquidity of $3.41 billion at the end of the second quarter, with the bulk of this constituted from a $2.5 billion revolving credit facility.

NextEra Energy Partners Fiscal 2024 Second Quarter Form 10-Q

Expectations Of NEP’s Future As Fed Rate Cuts Kick Off From September

NEP’s full-year 2024 guidance has CAFD at $730 million to $820 million, up from CAFD of $689 million in 2023. The midpoint of the 2024 guidance range at $775 million would represent CAFD growth of 12.5% on a year-over-year basis. While NEP’s cost of capital forms its core headwind, the company has stressed repeatedly that it’s set to grow the dividend through 2026 at a minimum. NEP’s management overlaps with NextEra Energy (NEE), the largest utility in the USA by market cap. If you don’t believe their guidance, then NEP is clearly not a buy.

NextEra Energy Partners June 2024 Investor Presentation

Investor confidence in NEP’s ability to maintain the dividend is low, this negative spectrum will shift to the betterment of current unitholders once the Fed starts cutting rates. This forms the most salient catalyst for the company’s common unit, as it could boost the 2024 CAFD guidance, also improving underlying dividend coverage. NEP offers a significant risk profile and should be out of the portfolio of the more risk-averse investors. To be clear, the market has not assigned a 14% yield to a company that was once priced at a 3% yield for no reason. NEP faces material risks, and a potential salvo from the Fed could still be deferred or not come at the intensity required to salvage NEP’s balance sheet. I’m taking on the risk here through with NEP rated as a hold.

Read the full article here

")