")

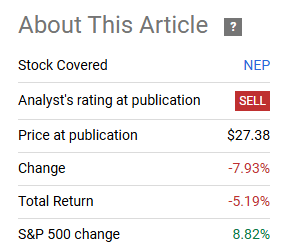

In our last update on NextEra Energy Partners, LP (NYSE:NEP) we had a non-consensus view on the high-yielding renewable play. While the income chasers were once again enamored with the dividend, we saw the risks as clear as day.

So we would not count on the current distribution becoming your annualized total return profile in the next 5 years. We rate NEP units a Sell and think there is a substantial downside once the distribution is realigned.

Source: Lower For Longer

Sure, the path did not go exactly as we envisioned, but we will take such a large underperformance from our Sell-rated stocks, any day of the week.

Seeking Alpha

Since then, we have had three developments that are going to influence the stock. We go over those and update our thesis.

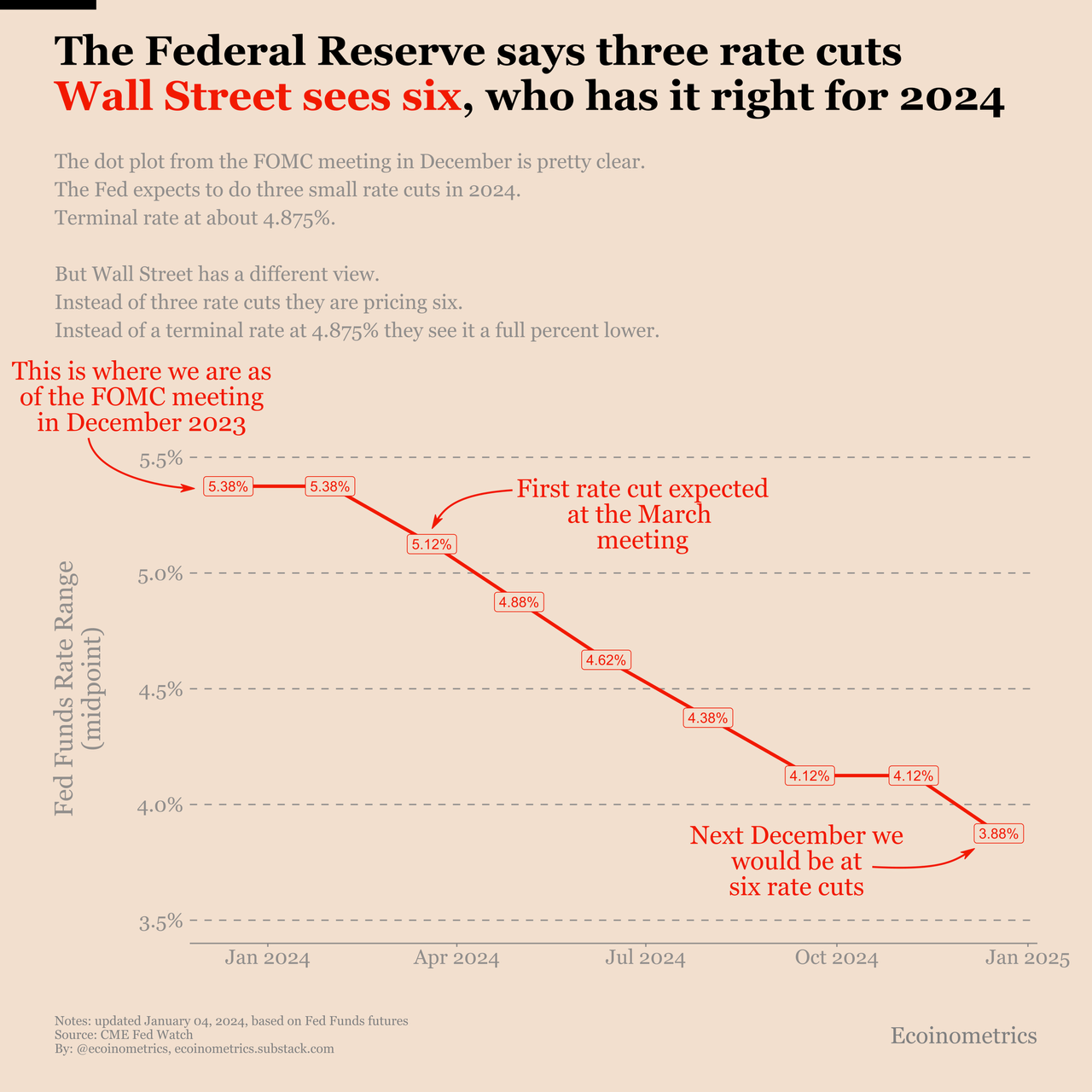

1) Interest Rate Cuts Going Out The Window

It was always our stance that the market euphoria in December 2023 would be proven incorrect. There would be no interest rate cuts coming to the rescue of bad investments. If indeed, the macro deteriorated far more than what we expected, and rate cuts were executed, it would bring a host of problems that would once again, not rescue bad investments. Wall Street began 2024 with a ridiculous expectation of 6 rate cuts.

Econometrics Jan 4, 2024

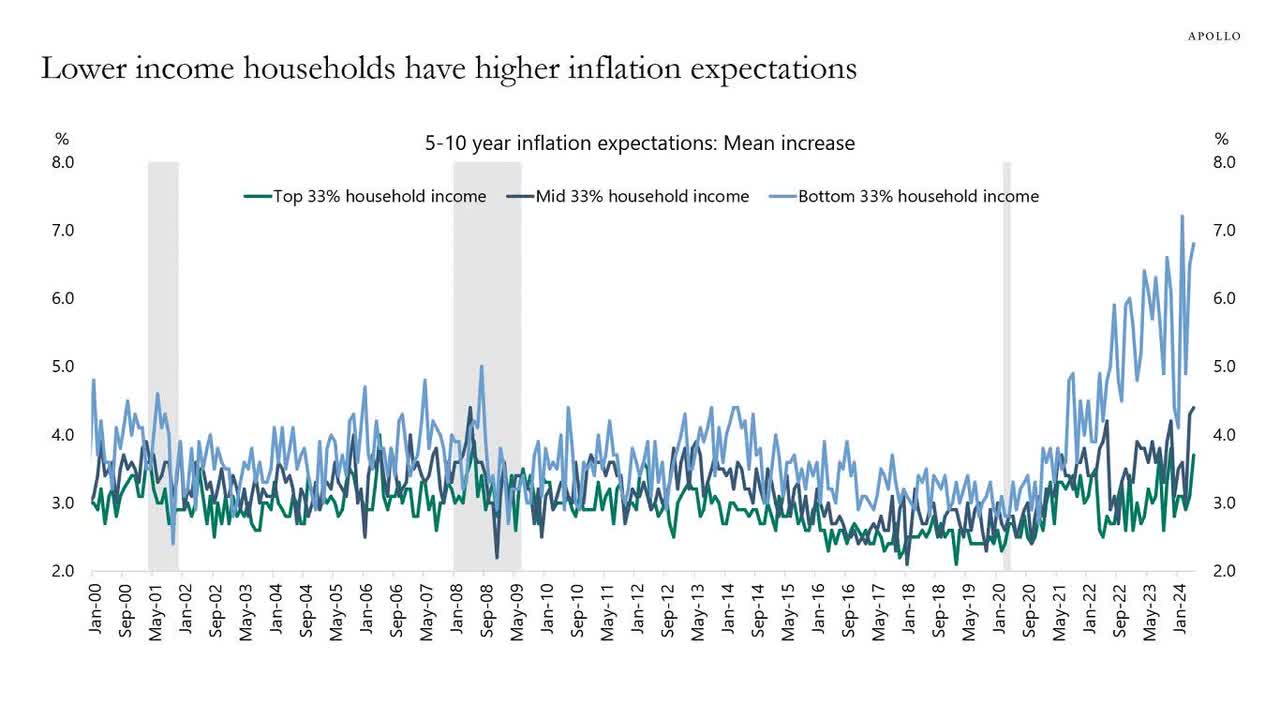

While the Federal Reserve projected just 3. Both have proven extremely optimistic and now we are down to a best-case scenario of just one. Even that is dubious so close to the election. Let’s not forget that inflation expectations are not exactly anchored for the low-income crowd.

Apollo Academy

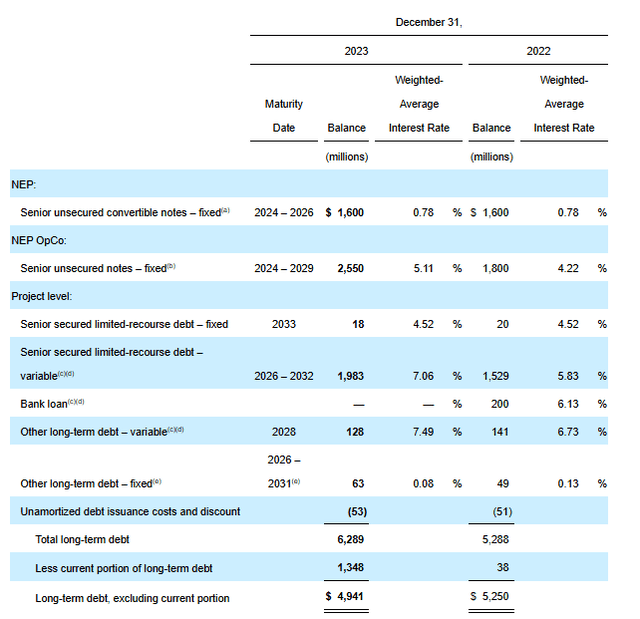

What all of this means is that NEP’s gambit of putting on a brave face and trying to ride things out till rates are lower is not going to pay off. The firm has challenges from both their debt refinancing and CEFP buyouts. The amounts are fairly large in relation to its market capitalization.

NEP 10-K

Some of this was refinanced recently, and the pipeline asset sale also addressed a portion, but the amounts remain unwieldy for a company with a 100% plus payout ratio. The top-level discussions will be ongoing as to when exactly they end this experiment of trying to increase the equity price by keeping the distribution high.

2) Q1-2024 Results Were Poor

Our article came a bit before the Q1-2024 results, so we missed that exciting piece of news. Investors seemed to focus only on the distribution increase.

Seeking Alpha

But the results were fairly bad and missed analyst consensus adjusted EBITDA and cash available for distribution, i.e. CAFD, numbers. We estimate that the miss was around 5%. Since non-GAAP CAFD numbers have so many adjustments, it is hard to be certain. Also, unlike EPS numbers, it is hard to compile analyst’s consensus for such metrics. What we do know is that CAFD per unit was 84 cents, and that comfortably threw the payout ratio well over 100% again. Wind energy numbers were well below expectations, and slightly higher tax credits helped offset those segment results. NEP reiterated 2024 guidance and proudly announced that there was no real growth coming anywhere except in the distribution. This was NEP’s version of we will keep the income investors interested until the “rug-pull”. They are clearly not covering this distribution even by their own metrics. Even ignoring the massive refinancing challenges ahead, the distribution is in trouble. At the minimum, they should freeze it. Instead, they raised it once more. We have seen this movie before, and you don’t want to stay till the end credits.

3) Atlantica Sustainable Infrastructure plc (AY) Shows What NEP Might Be Worth

We had gone long AY at $22.47 about a year back. Between the covered calls and the distributions, we did relatively ok. This was despite the company agreeing to a buyout near the lows. But what is really important here for investors, is the multiple being paid for AY. On an EV to EBITDA basis, AY was sold near 8.5X on 2025 numbers. They shopped around for a long time and likely had help from Algonquin Power & Utilities Corp. (AQN) which owned about 44% of the equity. All they got was 8.5X EV to EBITDA.

AY was and still is a relatively clean setup. There were no CEFPs to deal with. Unlike NEP, AY realized the challenges early and froze its dividend, much to the dismay of the income chasers.

Seeking Alpha

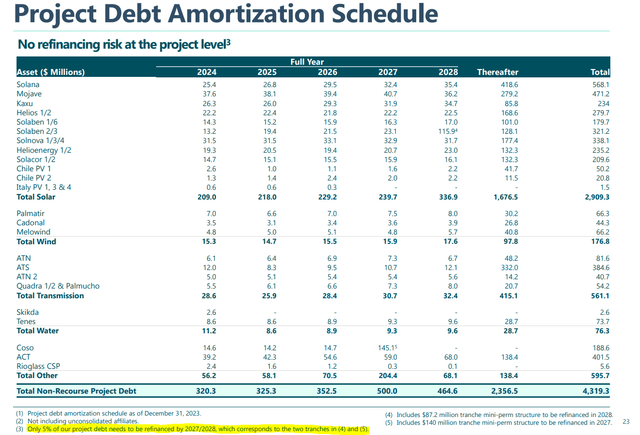

The bulk of AY’s debt is project-level and self-amortizing. Very little needs to be refinanced (5% as highlighted, by 2027-2028).

AY June 2024 Presentation

All of this is in stark contrast to NEP and yet, NEP trades at over 10X EV to EBITDA on 2025 numbers versus AY’s buyout at 8.5X. This may seem like a small difference, but it’s quite massive when we take into account the debt that remains constant in this equation. We estimate for NEP to trade at the same multiple after accounting for minority interest, it would have to move to around $19-$20 per share.

Verdict

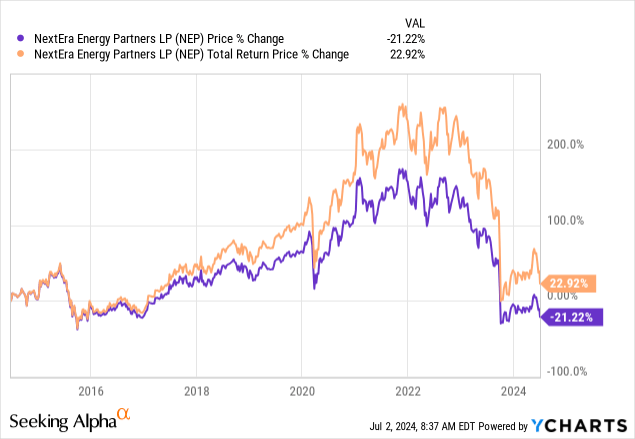

With these three factors firmly in our favor, we are sticking with our theme that NEP is likely to go lower. For those who have not read our “The Five Stages Of Grief”, we recommend you catch up on it with a nice cup of coffee. The parent NextEra Energy, Inc. (NEE) will swoop in to buy, but only after all the carnage has been unleashed on this income story. So far, the stock has delivered 22.92% total returns including distributions since inception.

A reminder here that the 10-Year Treasury yielded 2.4% around that time and would have beaten NEP since then, is appropriate. We are reiterating a Sell rating and would get more constructive once distribution is cut and the stock trades near 8.5X EV to EBITDA.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Read the full article here

(NASDAQ:RIVN)")