")

")

")

NextDecade (NASDAQ:NEXT) is a pure LNG play that has expectations to export first gas by year-end 2027. The company is full steam ahead with Bechtel, their EPC (engineering, procurement and construction) contractor, to build out Trains 1-3. Earlier this week, Next had a contract in hand to execute the EPC contract for Train 4. NEXT remains on site of the potential 27 mtpa Rio Grande LNG project, despite DC Circuit overturning the Federal Energy Regulatory Commission (FERC) site permit on August 6th.

The permit being overturned is as a result of FERC not issuing a supplemental environmental impact study (EIS) after the committees did not allow for adequate hearings from locals about impacts nearby with findings. Shares remain in free-fall over the past week as NextDecade attempts to find a path forward to appeal the overturning of the permit. Shares are down 35% over the past week and down 40% from 52-week highs.

This could provide a significant buying opportunity for someone looking for a five to ten year long investment with massive upside. Risk is obvious that the company is unable to change the DC Circuit ruling and Next has to abandon the project. I continue to dollar cost average into the stock on the 1st and 15th of every month.

About NextDecade

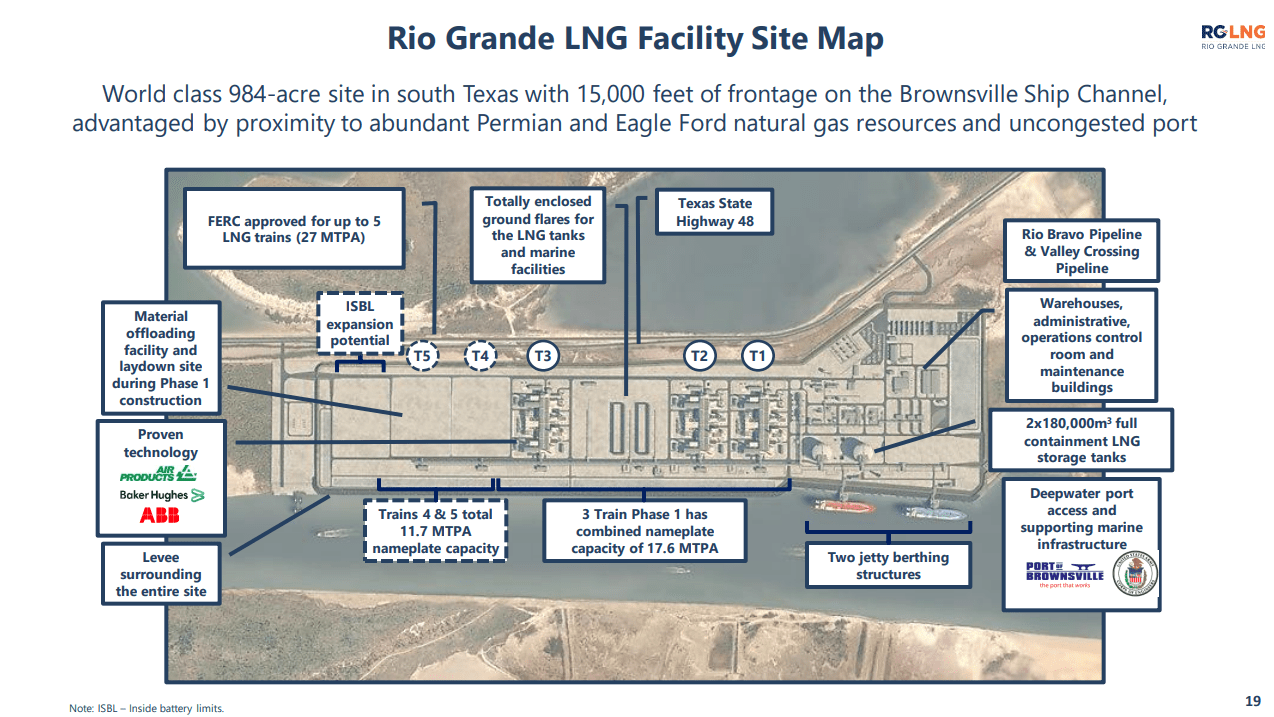

NextDecade is a Houston, Texas-based company and the owner and operating partner of the Rio Grande LNG project and its follow on Carbon capture and sequestration solutions group. Rio Grande is expected to be up to 27mpta of LNG once fully developed from 5 trains. Currently, trains 1-3 are sanctioned and being built by Bechtel, a world renowned LNG contractor, upon completion these trains will have 17.6mpta of export capacity (Phase 1).

Overview of Rio Grande LNG Project (NextDecade May 2024 Investor Deck)

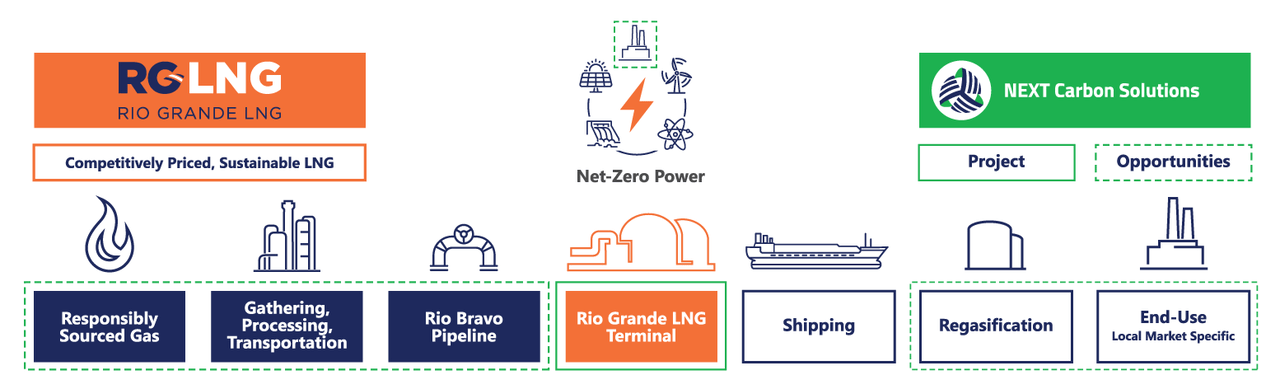

NextDecade formed on the back of the LNG terminal export race that began in the early 2010s after the United States began producing more shale oil and gas from combining horizontal wells with hydraulic fracturing to increase well productivity. The Rio Grande LNG project will take gas from the Eagle Ford and Permian fields and export as LNG to markets globally.

Rio Grande LNG is currently the first and only US LNG project that will have CO2 emissions less than 90% planned via carbon storage. Rio Grande previously owned the Rio Bravo pipeline until 2020 when it was sold to Enbridge.

Rio Grande LNG from supply to end (NextDecade May 2024 investor Deck)

Reasons To Stay Away From NextDecade/Risks

From my view, why should one stay away from NextDecade? Easy – it currently does not produce any income and will not until the first train of the LNG facility is up in running in late 2027 or 2028. To supplement, LNG projects are historically known for being massive undertakings, permit and cost overrun nightmares. Many companies without deep pockets or existing cash flow often go bankrupt or continue to pile on debt.

There is also potential that NextDecade does not find a way to appeal the DC Circuit ruling, which has overturned the FERC committee’s approval of the Rio Grande LNG project. In that case, pretty much all the value of the company is gone, since this is currently a single asset company.

Reasons To Contemplate A Position/Quantitative Valuation

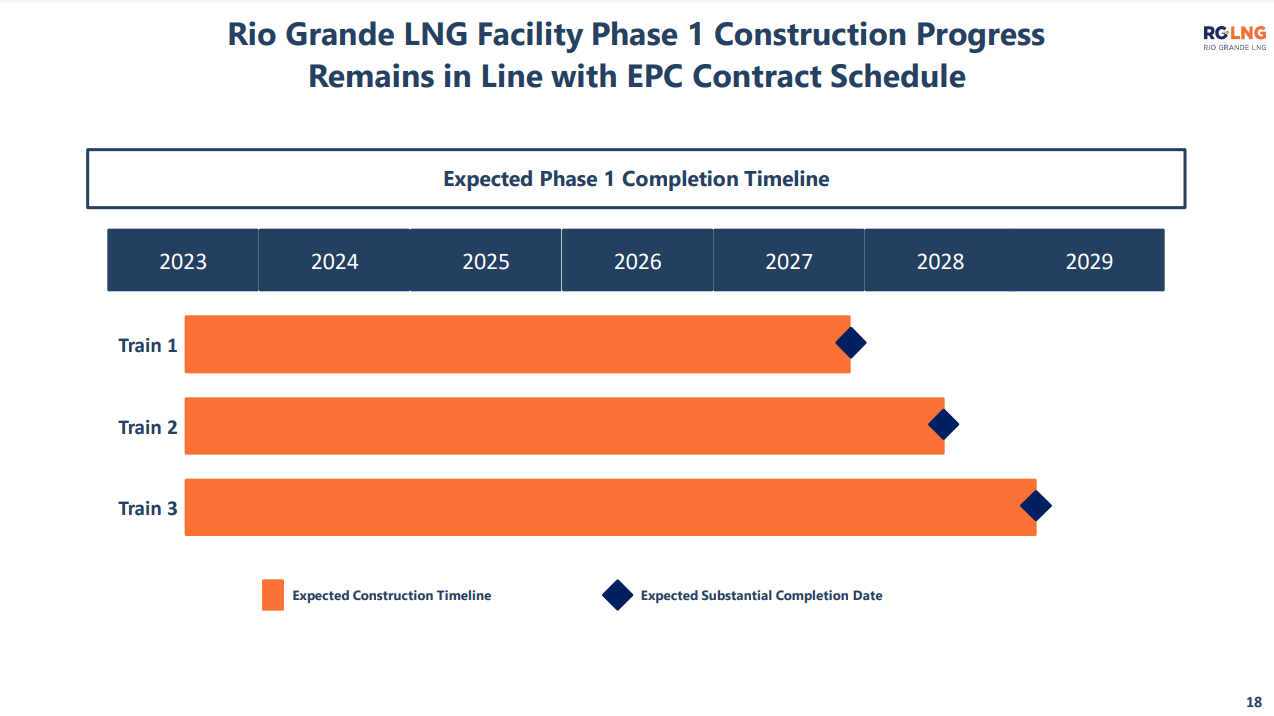

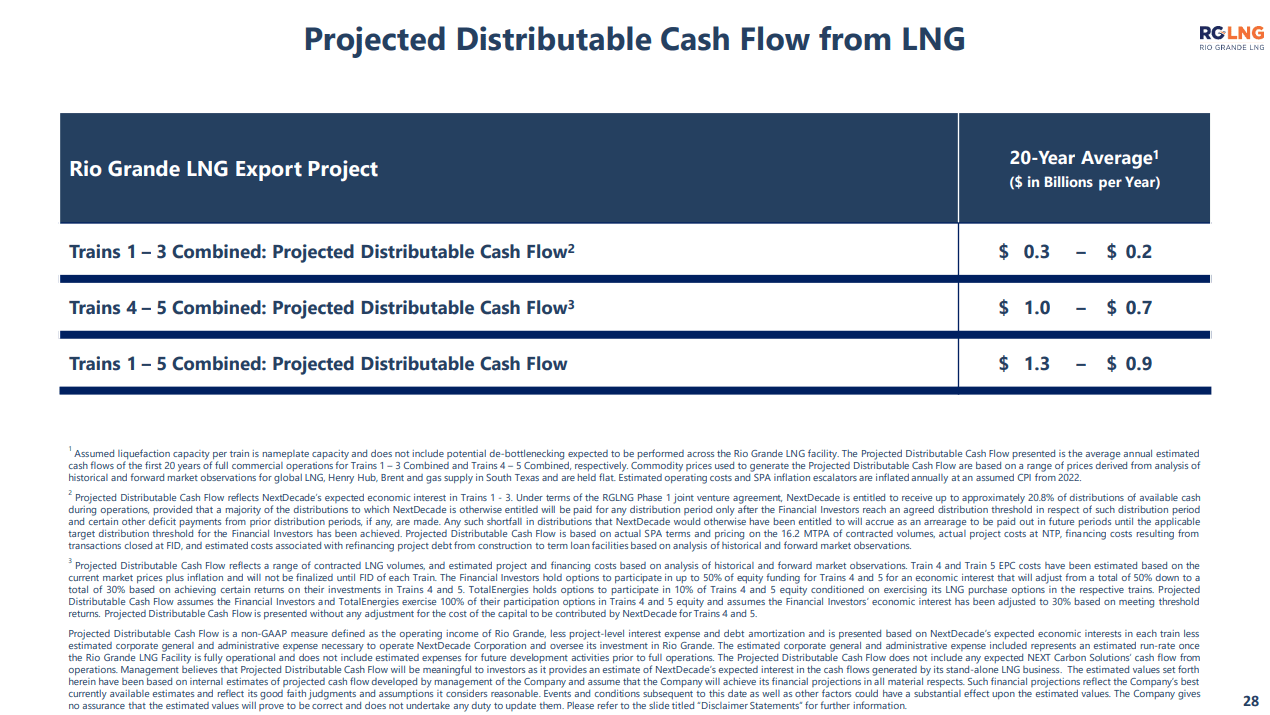

The Rio Grande LNG project has already sanctioned and achieved financing for Trains 1-3. Trains 1-3 are mostly being financed by partners, Global Infrastructure, TotalEnergies (TTE), GIC, and Mubadala, leaving NextDecade with an economic interest of just over 20%. Per NextDecade’s past several investor presentations, without sanction of follow-on trains, this would leave distributable cash flow between $200-$300m per annum.

At a current market cap below $2bn, that would leave P/DCF (distributable cash flow) to be 6.5 to 10x, keeping in mind that the full stream of cash flow is not available until start-up of all trains 1-3, which would likely not be until 1H2029, potentially later with this DC Circuit ruling.

Rio Grande LNG Phase 1 Start-Up Schedule (NextDecade May 2024 Investor Deck)

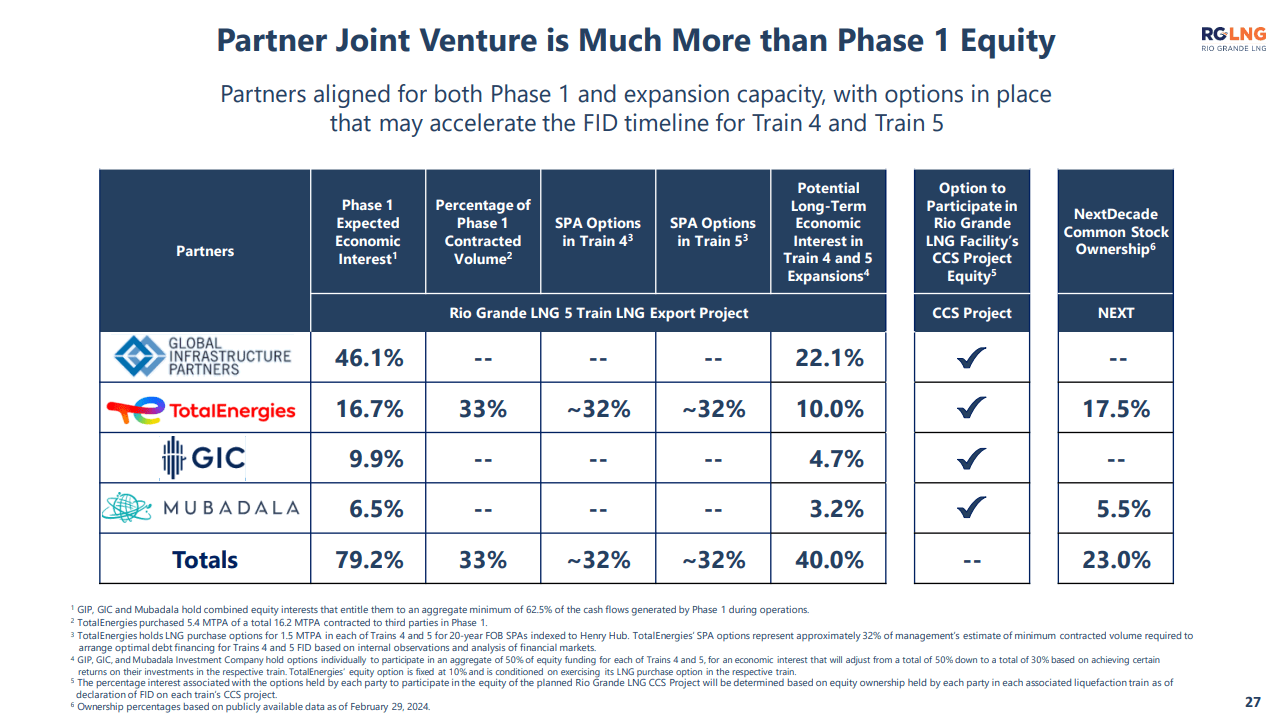

The real upside for NextDecade can be realized if they can secure their 60% ownership in trains 4 and 5 without further dilution. At the moment, Global Infrastructure Partners, GIC and Mubadala are on the hook for 50% of the equity payments in Trains 4 and 5, while Total is responsible for the remaining 10%. This means that the majority of funding for Trains 4 and 5 comes from partners, leaving 40% of the cost to NextDecade. These two trains alone, with their increased equity position for NextDecade net them an incremental $700m-$1bn in distributable cash flow once all trains are up and running.

So how does NextDecade end up with 60% ownership and the addition of $700m-$1bn in distributable cash flow? Their equity contribution is only 40%?

Upon return-based performance of train 4 and 5 individually, the equity interest of several of the partners will drop to 30%, allowing NextDecade to capture that additional 20% in equity for trains 4 and 5. Total’s equity interest remains at 10% as they have long-term LNG contracts that assist with stabilizing funding for the expansion project.

Rio Grande LNG Train Breakdown (NextDecade May 2024 Investor Deck)

So how does the valuation look in the early 2030s with the addition of Trains 4 and 5? Meeting performance expectations and without further dilution, distributable cash flow is $900m-$1.3bn. At a current market cap of $2bn today, this leaves P/DCF in the future to be 1.5 to 2.25x.

The valuation is paying for three things, for you to wait, for the company to meet performance expectations and thirdly, that the DC Circuit does not completely shut down construction.

NextDecade’s Distributable Cash Flow from Rio Grande LNG (May 2024 Investor Deck)

Where Does The Street Value NEXT?

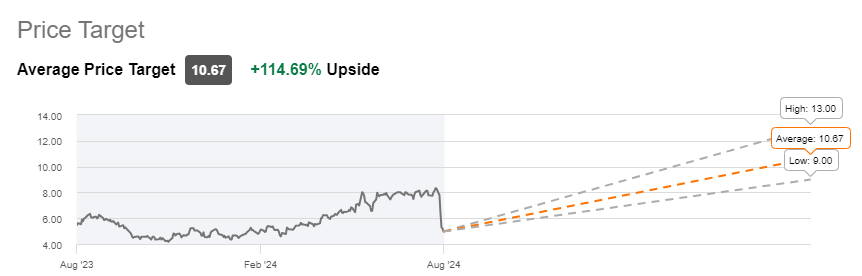

Over the past 12 months, Street analysts have consistently rated NEXT a 4.0, which is a buy rating with an average price target north of $10.50. One analyst has the stock rated as a strong buy, one a buy, and one hold.

NEXT 12-month Price Target (Seeking Alpha)

Fellow Seeking Alpha analysts have wavered on the stock over the past twelve months, with sell to hold orders. There has been 1 analyst rating the stock a hold in the last 90 days.

Quant rating has maintained a hold rating over the last 12 months with a 3.32 on the stock. With the price drop to $5, quant valuation has been re-rated from a D+/C- to a B-, with the main drag on the stock being profitability, at a D-.

I do not have a solid price target on the stock due to its speculative nature and long-time horizon, that said I am accumulating at these prices and was accumulating even in the $8 range prior to the DC Circuit ruling.

I would likely pull back on my contributions if the stock went too much further north of $8 without solidifying the 4th train sanction.

Conclusion

This stock is a unique bet on US liquified natural gas (LNG) assets in their infancy, with expected cash flows from 2030-2050+. Investors in NextDecade need to have a long-time horizon in mind, as cash flows do not start until 2H 2027.

Recent rulings from DC Circuit overturning the Federal Energy Regulatory Committee’s approval of the Rio Grande LNG project caused the stock to plunge 40% from recent highs. Despite this ruling, NextDecade moves forward with the construction of trains 1-3 in the Rio Grande Valley. Even during litigation, NextDecade is hard at work awarding EPC (engineering procurement and construction) contracts to Bechtel, and is imminently awaiting the final investment decision on Train 4.

That said, the overturned permit puts significant risk on NextDecade as it is a single asset corporation focused strictly on the Rio Grande LNG project. If Next fails to appeal the DC Circuit ruling, the company may be forced to abandon the project and cease to exist. With that key risk overhanging, Rio Grande LNG stands to become one of the first US LNG projects with significant carbon capture and sequestration, leading to over 90% reduction in carbon emissions. The already financed trains 1-3 provide an okay opportunity to buy shares and attain cash flow from dividends or buybacks in the future, but lack of profit or income today may drive value investors away.

Upside opportunity for those willing to take on the risk comes with future cash flows from trains 4 and 5, which add 11mpta to the Rio Grande LNG project. NextDecade’s 60% equity ownership in these trains, add between $700m and $1bn in incremental distributable cash flow. This brings the valuation of the company to a 1.5 to 2.25x price to distributable cash flow in the early 2030s.

As the project is in early days and has no income, few analysts rate the stock a buy, and many analysts from the Street and Seeking Alpha seem hesitant to invest; however, the potential upside is clear for those who are looking for a stock needing a longer time horizon and higher risk tolerance.

Read the full article here

")

")