")

")

The Yoga Master

A couple of months ago, I was invited to speak about investments at the Florence branch of a major national bank. I was facing about 30 young financial promoters, with whom I began my conversation by telling them this story.

Forty years ago, I played volleyball in the big leagues with the university team in my town. The club’s means were few, and for our trips to southern Italy we often used the train. During one of our long overnight sleeper travels, we made the acquaintance of a yoga master, who had a long talk with our coach, also interested in Eastern disciplines. It was the first time in my life that I heard of yoga, and the conversation was very informative, although we players were careful not to intervene. Then, having reached our destinations, we said our goodbyes and went our separate ways.

A few months later, I got on a train to visit my relatives in the Po Delta and happened to meet that yoga master again. I recognized him right away, but he did not remember me because he had talked almost entirely with my coach. He was, however, well aware of the long talk he had had with him and complimented me on recognizing him by saying this phrase, which has remained etched in my mind ever since: “When the pupil is ready, the master will appear.”

First Be Ready

When the pupil is ready, that is, when the fundamental condition is present. Not before. In this short sentence was condensed millennial knowledge, the knowledge that of the three verbs around which our lives revolve -being, doing and having- the first is the most important. It applies to food diets, which do not work if we do not first change our relationship with food, as it does to investments, which cannot succeed if we focus only on the technical aspects of financial instruments without having first understood how our brain reacts to the movements of our portfolio. In practice, without having understood who we are (“being”), before embarking on the path (“doing”) to get what we want from our investments (“having”).

In the years prior to the discovery of high-dividend stocks in the U.S. market, I had already experienced the benefits of a quarterly coupon flow from two Italian government bonds with yields around 4.5 percent. To these, I had added a couple of monthly dividend Franklin Templeton funds (including the Global Bond, the first of its kind in Italy), which had allowed me to better withstand temporary capital depreciation of my portfolio due to market fluctuations. In my mind, the feeling of relative well-being afforded by the periodic income stream generated by my investments outweighed interest in their capital appreciation, which I could obtain anyway through the reinvestment of dividends.

Even before I understood how high-yielding vehicles work and the proper tools to navigate them, I had focused on my character and set my priority: adopting a dividend strategy. Being, before doing. The pupil was ready and knew what he wanted. The journey could begin.

What Is Dividend

But what is a dividend? A dividend is the portion of earnings that a company distributes to its shareholders during the fiscal year. Based on this definition, according to Fidelity, “dividend companies are generally high-quality companies with resilient business models, strong balance sheets and stable cash flows that are not only able to pay attractive dividends, but also reinvest some of the cash back into their business to enable sustainable dividend growth in the future.” In two words, the perfect world.

Broadening the scope of analysis, I will use the generic term “dividend” to refer to the amount of money generated by an investment, without distinguishing between proper dividend, distribution or coupon, as in the case of income from CEFs, ETFs, and ETNs.

Now, in everyday life, if you go out to dinner every night and at the end of the month, your bank account has gone up, it means you earn more than you spend, but if it goes into the red it means you can’t afford it and some questions need to be asked. You don’t need square roots or Greek symbols to figure out what is wrong, just as you don’t need them in the case of any unsustainable dividends paid by our funds. What tells us that things are wrong is the NAV, i.e., the net value of the assets held in our securities: in the short run the NAV is subject to many variables (related, for example, to market fluctuations or dividend payments), but in the long run it casts a clear, shadowless light on their performance.

What a Dividend Strategy Means

Herein lies the point: in my opinion, for a dividend to be a “true” dividend, it must be self-sustaining. That is, the recipient must be able to dispose of it freely without having to worry about replenishing the initial capital, except by taking the necessary measures to protect its purchasing power. This is only the case if a security’s NAV grows over time, showing that the dividend payment does not hinder its appreciation.

In the different case where our securities lose value over time and require the continuous use of money to replenish the initial capital, the reinvestment of dividends takes, in my opinion, the form of an amortization schedule. That is, it takes the form of the gradual extinction of a debt, exactly as with car payments (and thus the exact opposite of an investment). This happens in the case of securities whose NAV shows a steady and inexorable decline over time, which is difficult to ascribe only to temporary and/or resolvable situations.

Of course, I am aware that a successful past does not automatically give a guarantee of an equally bright future, but if I wanted to root for the team most likely to win the next Champions League, I would choose Real Madrid and not Fiorentina (as I have done since childhood, alas… but there it’s a matter of heart). Thus, between a stock that has been growing steadily over the years and one that has always been in decline, common sense and Occam’s Razor lead me to think that the former may offer me a better chance of gaining even in the future.

For this reason, in recent years, I have increasingly turned toward selecting securities for my portfolio whose NAV shows a positive trend, demonstrating that dividend payments do not burden the value of the assets in any way, which even tends to increase over time. Among other things, I wonder what sense there is in buying a continuously losing stock with the purpose of trying to keep it (or bring it back) afloat, instead of acknowledging the mistake and accepting the consequences.

Yet, there are CEFs with extremely high distributions and disastrous NAV performances, even pricing at double-digit premiums. Perhaps underlying their success are tax reasons that escape me, as I am an Italian taxpayer who does not benefit from capital losses.

Weights, Numbers and Percentages

I had already alluded to this distinction in two articles published in December 2021 (“Everything You Always Wanted To Know About Total Return”) and January 2022 (“My Income Portfolio Total Return”). At that time, I had already begun to question the performance of NAV as a unit of measurement of a fund’s efficiency versus Total Return, which can be misleading when an unsustainable dividend drowns out NAV while giving the illusion of a positive return as invested capital slowly evaporates.

An awareness of this that I have tried over time to apply in the selection of securities for my portfolio, but unfortunately still far from efficient in this respect, although right now, the overall balance is around parity.

All of this being premised, let’s now try to take a closer look at my portfolio and the role of each security within it. As you may know, my assets today include 28 securities (19 CEFs, 5 ETFs, 3 BDCs, 1 ETN) organized into three different portfolios:

Cupolone Income Portfolio (named after Brunelleschi’s Florentine dome) consists of seventeen CEFs with monthly distributions:

- BlackRock Science and Technology Trust (BST)

- Calamos Dynamic Convertible and Income (CCD)

- Calamos Global Total Return (CGO)

- Eaton Vance Enhanced Equity Income II (EOS)

- Eaton Vance Tax-Adv. Global Dividend Opps (ETO)

- Eaton Vance Tax-Adv. Dividend Income (EVT)

- Guggenheim Strategic Opportunities (GOF)

- John Hancock Tax-Adv. Dividend Income (HTD)

- PIMCO Corporate & Income Strategy (PCN)

- PIMCO Dynamic Income (PDI)

- John Hancock Premium Dividend (PDT)

- PIMCO Corporate & Income Opportunities (PTY)

- Cohen & Steers Quality Income Realty (RQI)

- Special Opportunities Fund (SPE)

- Cohen & Steers Infrastructure (UTF)

- Reaves Utility Income Trust (UTG)

- XAI Octagon FR & Alt Income Term Trust (XFLT)

Giotto Income Portfolio (named after the fourteenth-century Florentine painter and architect) includes five ETFs and one ETN with monthly distributions that adopt a covered-call strategy:

- JPMorgan Equity Premium Income (JEPI)

- JPMorgan Nasdaq Equity Premium Income (JEPQ)

- Global X Nasdaq 100 Covered Call (QYLD)

- Global X Russell 2000 Covered Call (RYLD)

- Credit Suisse X Links Crude Oil Shares Covered Call ETN (USOI)

- Global X S&P 500 Covered Call (XYLD)

Masaccio Income Portfolio (named after the founder of Renaissance painting) contains three BDCs and two CEFs with quarterly distributions:

- Ares Capital (ARCC)

- Crescent Capital (CCAP)

- Fidus Investment (FDUS)

- Barings Corporate Investors (MCI)

- Royce Value Trust (RVT)

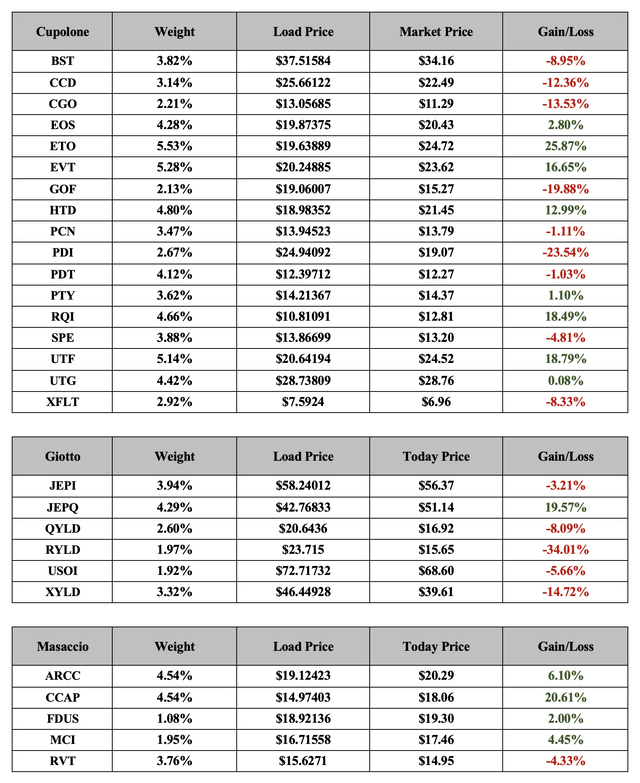

The following table shows the weight of each security (based on the current market price), the load price, the current market price and the gain or loss for each position.

Author

In my last article, I briefly mentioned my resolutions regarding some positions currently in the red for the moment they should break even again: which, however, I don’t think will be possible. The next paragraphs will report the NAV performance of the past five years (that is, since before the outbreak of the pandemic) for each security in my current portfolio, and from launch to present for the few born after 2019, so as to clarify the rationale for my evaluations and related intensions.

With all that happened, I believe that the last five years is a sufficient time frame to illustrate the trend of each stock without necessarily going back as far as the time of launch, thereby avoiding including in the analyses events that are now so far, back that they no longer have any influence on today’s developments.

Cupolone Income Portfolio

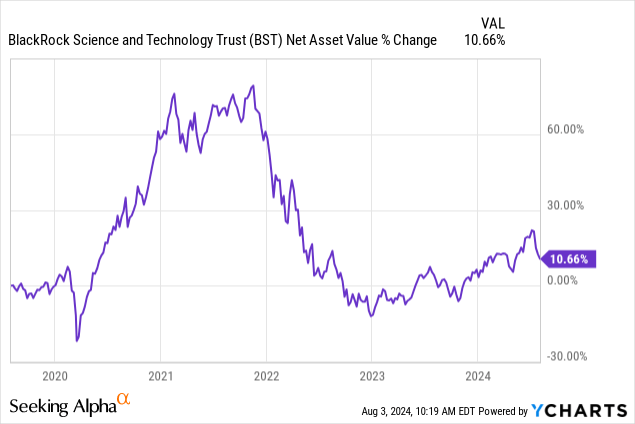

BlackRock Science And Technology Trust

Positive rating for long-term growth prospects (+90% since launch). Permanently part of my portfolio even if purchased at too high a price.

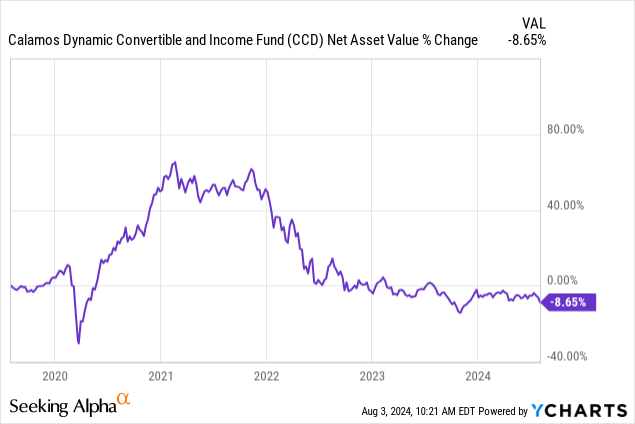

Calamos Dynamic Convertible and Income

Neutral rating for its sideways trend, which makes room for possible recovery. A position that I intend to keep open for the time being, hoping for an upcoming reversal of the trend.

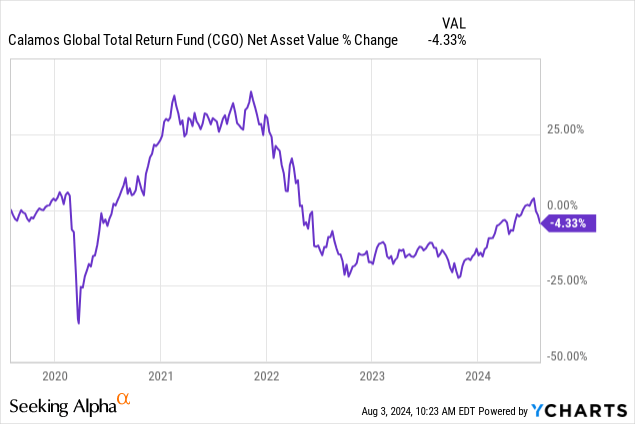

Calamos Global Total Return

Neutral rating for its lateral tendency. I probably bought it at too high a price, and its volatility at one point caused me to take a capital loss close to 40 percent. A microcap stock position that I would like to close the moment it breaks even in my portfolio.

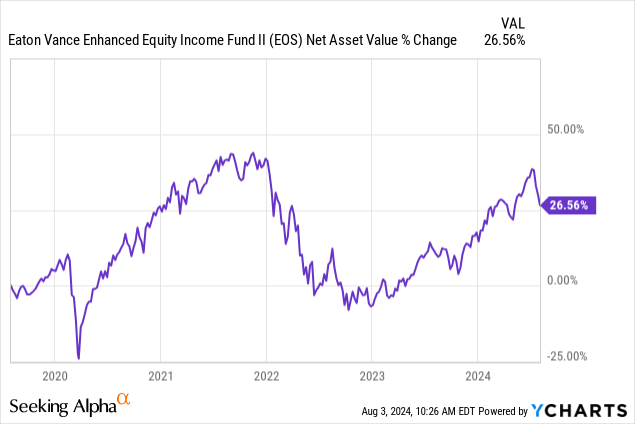

Eaton Vance Enhanced Equity Income II

Positive rating for its resumption of growth after the decline of the last two years. Confirmed as a stable presence in my portfolio.

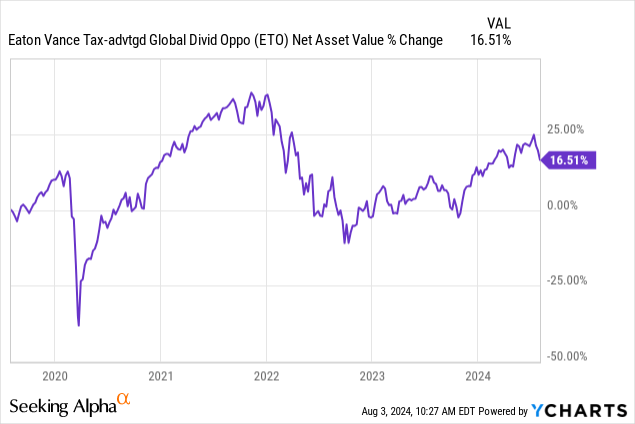

Eaton Vance Tax-Adv. Global Dividend Opps

Positive rating for its resumption of growth after the slight decline of the last two years. Confirmed as one of the best stocks in my portfolio.

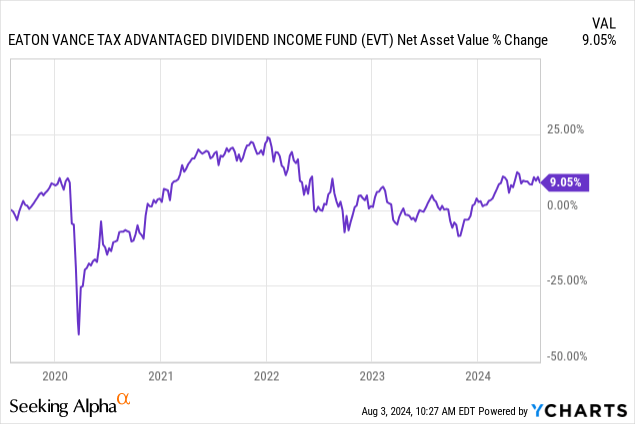

Eaton Vance Tax-Adv. Dividend Income

Positive rating for a stock that has returned to growth after a slight decline over the past two years. Confirmed as one of the best stocks in my portfolio.

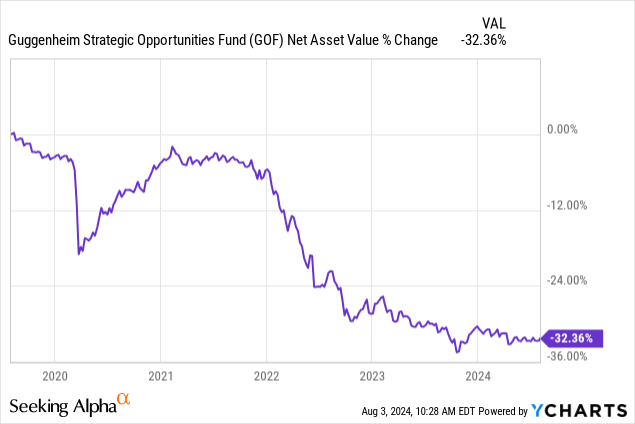

Guggenheim Strategic Opportunities

Negative rating for a steadily declining stock. I lightened my position over time because I imagine a recovery difficulty and have the intention of selling it in case of rebound favored by any rate cuts (incidentally, the stock is trading at a 27% premium).

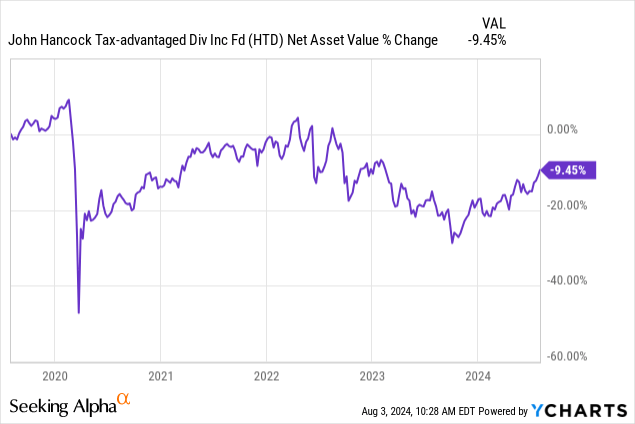

John Hancock Tax-Adv. Dividend Income

Positive rating for a stock that has been gaining since launch (+23.58%) but has been marking time over the past five years. Its sideways trend makes room for possible recovery, though. Confident in this stock that’s been stably in my portfolio.

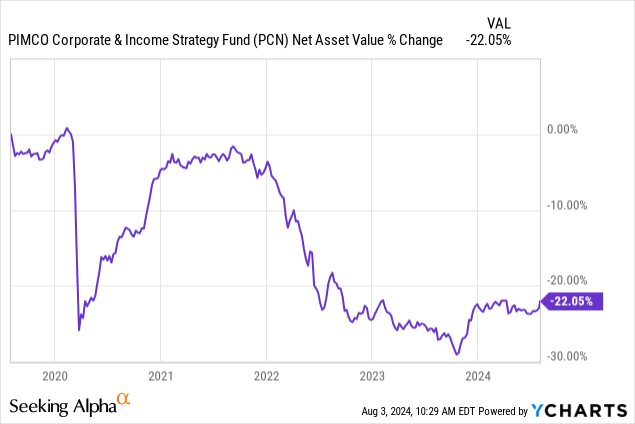

PIMCO Corporate & Income Strategy

Negative rating for a steadily declining stock, although my position is only losing a few percentage points and I intend to hold it at the moment. Possible bounce favored by any rate cuts.

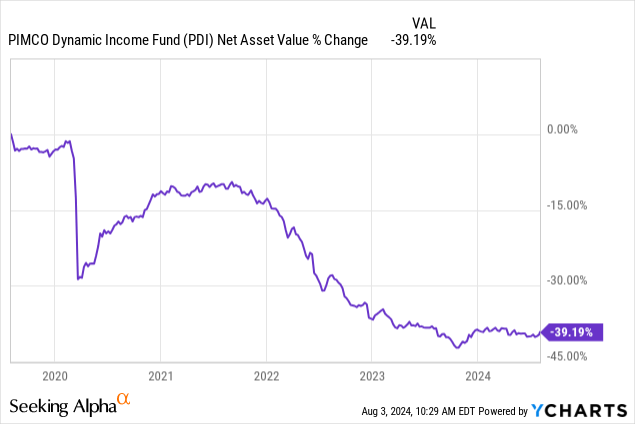

PIMCO Dynamic Income

Negative rating for a steadily declining stock, With a loss of more than 40 percent in the last five years. I lightened my position over time because I imagine a recovery difficulty and have the intention of selling it in case of rebound, favored by any rate cuts.

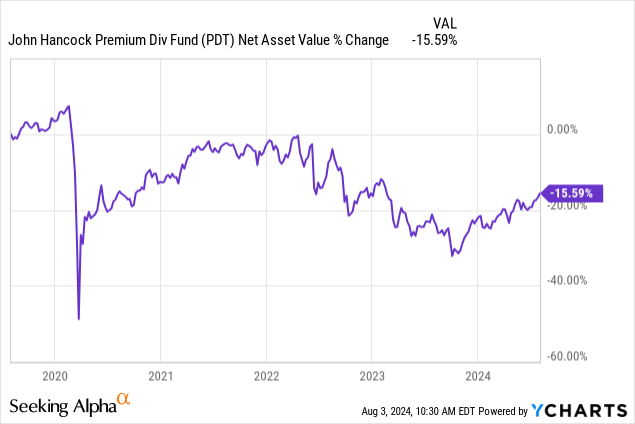

John Hancock Premium Dividend

Neutral rating for a stock that has been gaining since launch (+18.20%) but has been marking time over the past five years, although my position is only losing a few percentage points. Confident in resumption of growth for a stock stably in my portfolio.

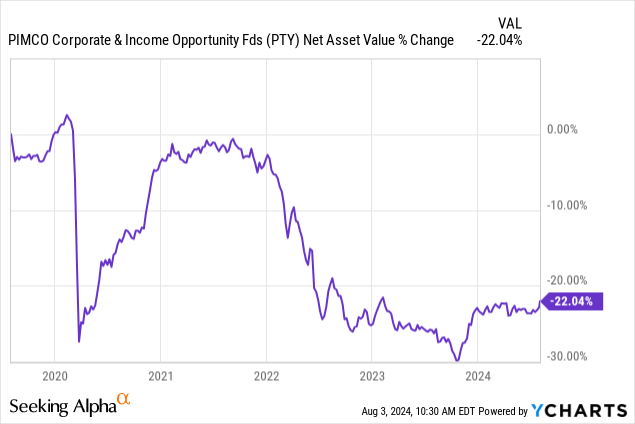

PIMCO Corporate & Income Opportunities

Negative rating for a steadily declining stock, although my position is barely in profit and I intend to hold it at the moment. Possible bounce favored by any rate cuts.

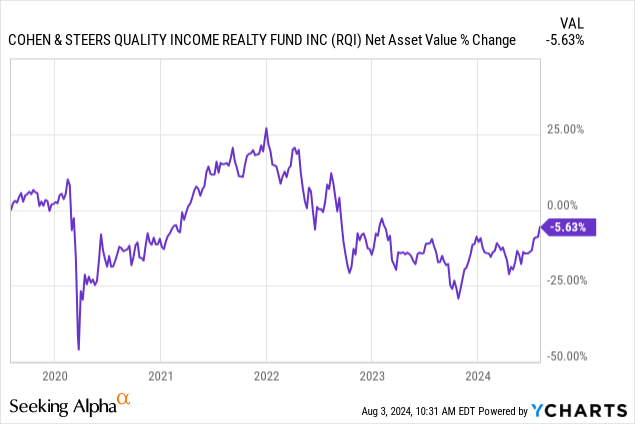

Cohen & Steers Quality Income Realty

Neutral rating for its sideways trend (although in negative territory at the moment), that makes room for possible recovery. A position that I decided to keep open for the time being, hoping for an upcoming reversal of the trend.

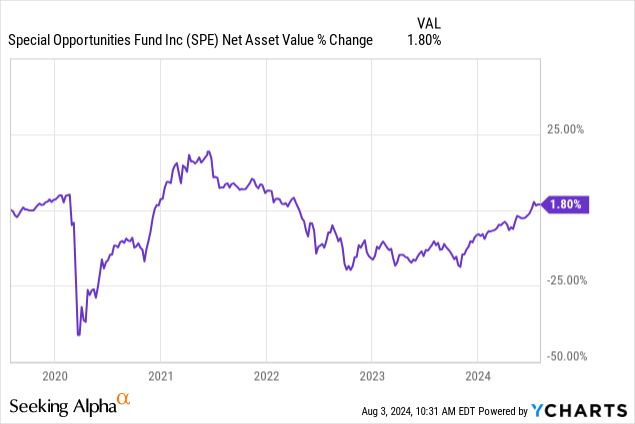

Special Opportunities Fund

Positive rating for its lateral tendency and the broad recovery in recent months. I probably bought it at too high a price, but it is a position that I decided to keep open for the time being, hoping for the maintenance of the trend.

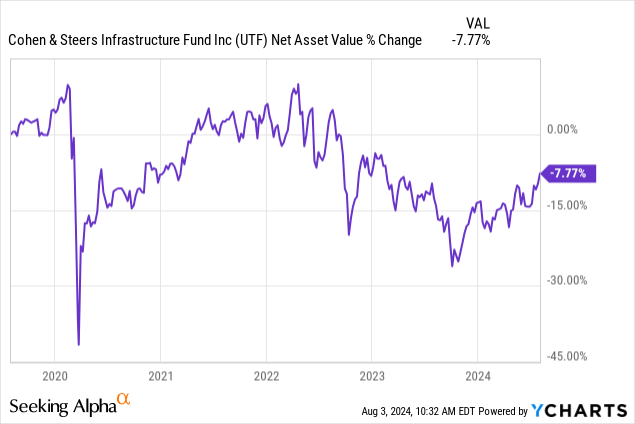

Cohen & Steers Infrastructure

Positive rating for a stock that has been gaining since launch (+28%) but has been marking time over the past five years, although my position is in good gain. Confidence in resumption of growth for a stock stably in my portfolio.

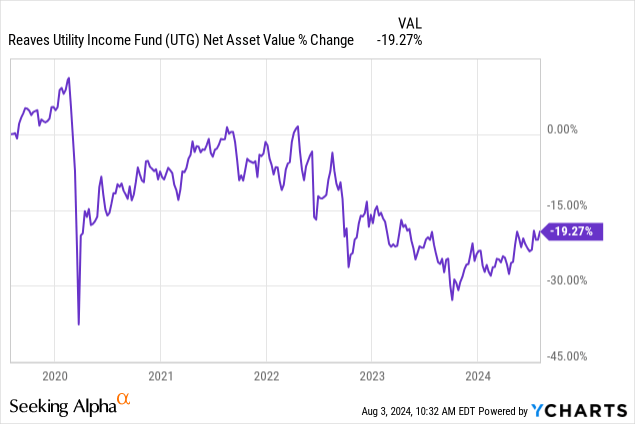

Reaves Utility Income Trust

Positive rating for a stock that has been gaining since launch (+48.5%) but has been greatly marking time over the past five years. My position is at a slight loss, but I have confidence in the resumption of growth for a stock stably in my portfolio.

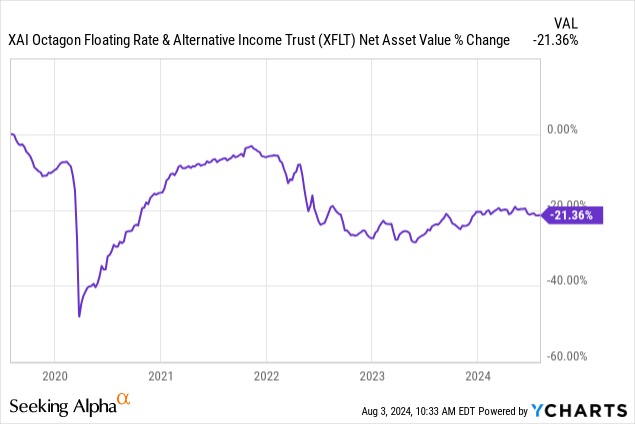

XAI Octagon FR & Alt Income Term Trust

Negative rating for a steadily declining stock, although my position is only losing a few percentage points. The sideways phase started two years ago gives me hope for a possible recovery that could allow me to get out of the position without loss.

Giotto Income Portfolio

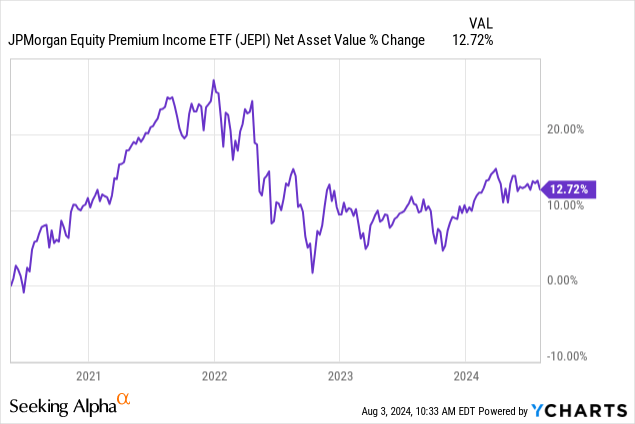

JPMorgan Equity Premium Income

Positive rating for a stock launched in 2020 and that has been gaining since launch, although with a slight decline in the last two years. My position is at a slight loss, but I have confidence in the continuation of growth for a stock stably in my portfolio.

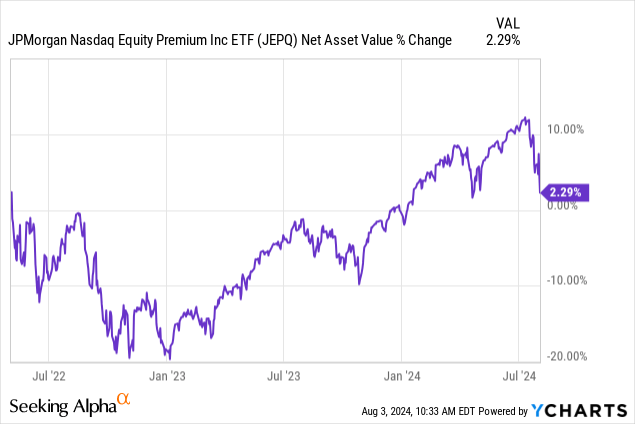

JPMorgan Nasdaq Equity Premium Income

Positive rating for a stock launched in 2022 and that has been gaining since launch, although it resumed growth in early 2024 after a year-and-a-half-long decline. My position is in strong gain for a stock stably in my portfolio.

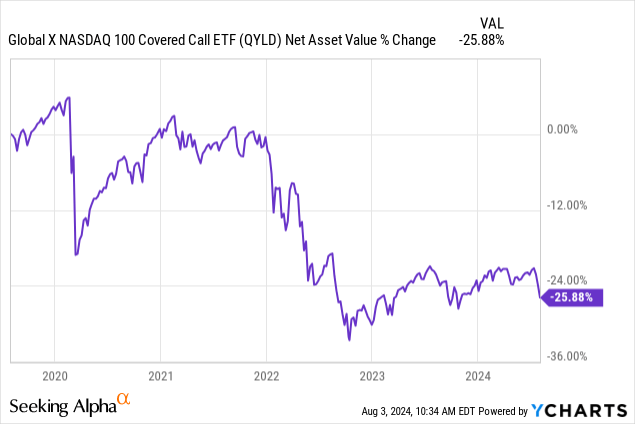

Global X Nasdaq 100 Covered Call

Negative rating for a steadily declining stock despite recovery from 2023 lows. My position is at a loss of more than 12 percent, but I have not given up hope for a possible recovery that could allow me to get out of it without excessive loss.

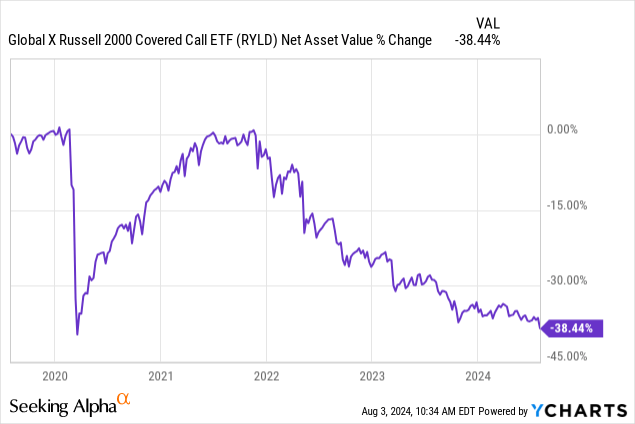

Global X Russell 2000 Covered Call

Negative rating for a stock that has been continuously losing since launch and shows no signs of recovery. My position has been lightened over time, and I would welcome a rebound that would allow me to get out of it while limiting the damage.

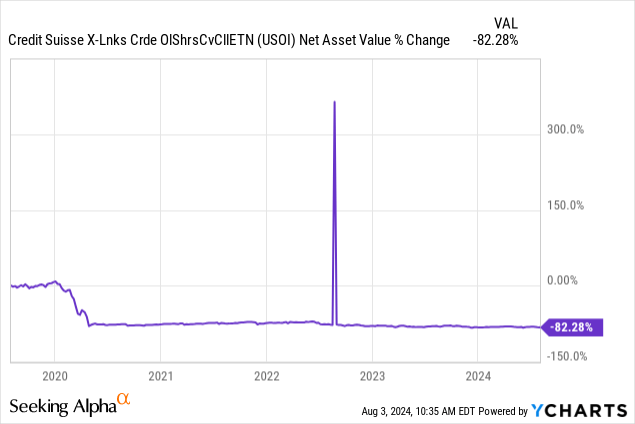

Credit Suisse X-Links Crude Oil Shares Covered Call ETN

Negative rating for its downward trend, but merits separate consideration for this ETN, which I hold more for fiscal reasons, being the only one in my portfolio whose monthly coupons allow me to offset past losses. My position is currently in slight loss, and for now, I intend to maintain it.

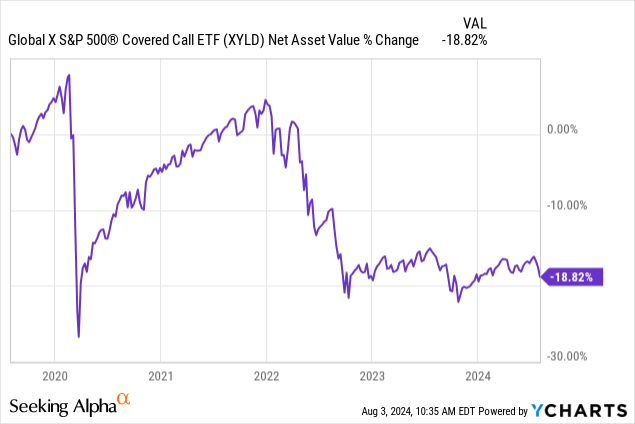

Global X S&P 500 Covered Call

Positive rating for a stock at a slight loss since launch (-1%) but has been greatly marking time over the past five years. My position is at a 12% loss, but I have confidence in a possible recovery.

Masaccio Income Portfolio

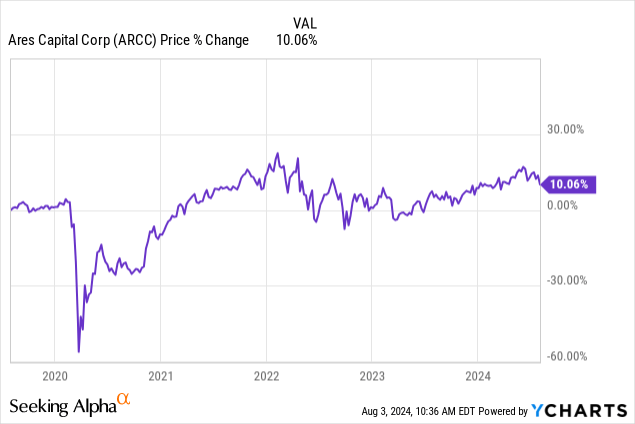

Ares Capital

Positive rating for a stock in good gain since launch, which has not slowed down even in the last five years after a sharp decline at the outbreak of the pandemic. My position is in gain for a stock stably in my portfolio (please note that the graph of this BDC refers to price and not to NAV).

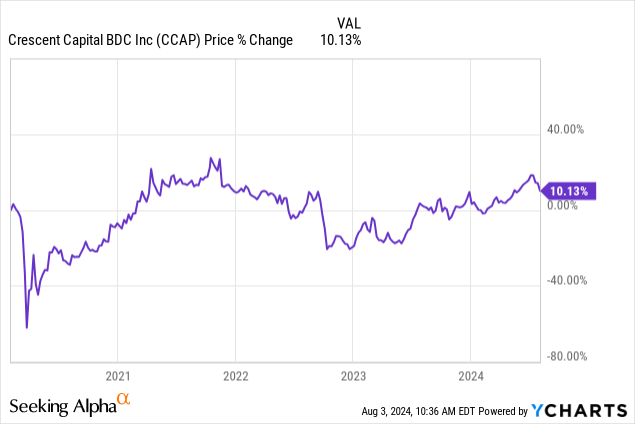

Crescent Capital

Positive rating for a stock launched in 2020, on the eve of the pandemic outbreak, and shows a good gain since then. My position is in strong gain for a stock stably in my portfolio (please note that the graph of this BDC refers to price and not to NAV).

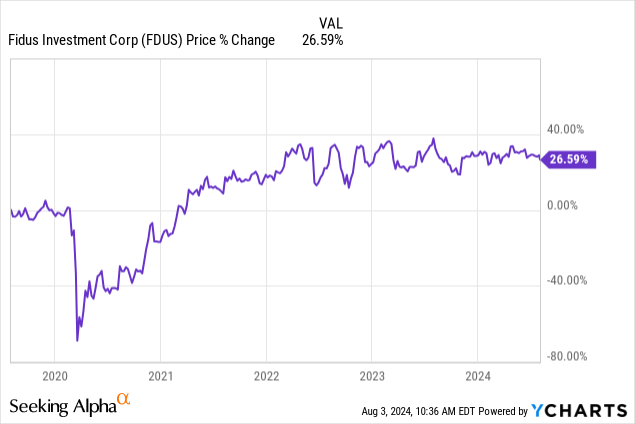

Fidus Investment

Positive rating for a stock in wide gain since launch, which has not slowed down even in the last five years after a sharp decline at the outbreak of the pandemic. My position is in gain for a stock only recently entered in my portfolio, and which I plan to increase (please note that the graph of this BDC refers to price and not to NAV).

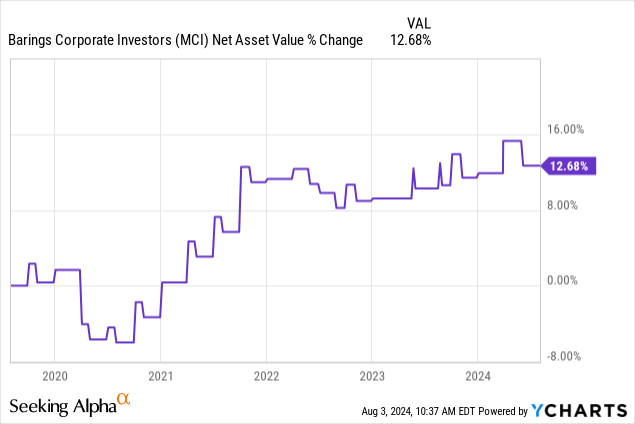

Barings Corporate Investors

Positive rating for a stock in enormous gain since launch, which has not slowed down even in the last five years. My position is in good gain for a stock only recently entered in my portfolio, and which I plan to increase.

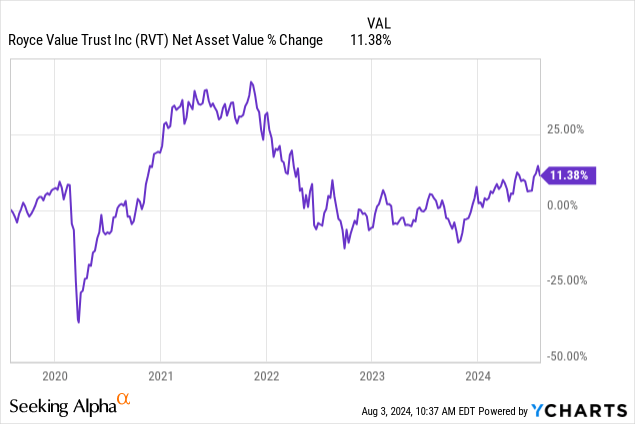

Royce Value Trust

Positive rating for a stock in very good gain since launch, which has not slowed down even in the last five years. My position broke even after a sharp decline due to a purchase made at too high a price. Stock stably in my portfolio.

Speaking Softly

And you know what’s going to happen now. You should admit your situation. There would be more dignity in it” (Anton Chigurh in “No Country for Old Men”.)

In a previous article, I have pointed out that the tax aspects of CEFs and ETFs are rather penalizing for us Italians, which has always led me to weigh any decision regarding loss-making stocks carefully, given the difficulty for me as an Italian in offsetting such losses. In a way, however, a (slightly) loss-making portfolio dispenses me from making decisions and in a way requires me to live day to day waiting for events to unfold.

Now that my portfolio is slowly returning to positive territory (at least until a few days ago) and even the biggest loss-making positions have reduced their exposure, sooner or later, some of the decisions I anticipated will have to be made. The further I get in years, however, the less inclined I am to put myself on the line, reset the past and start again on new adventures. Let’s say that a balanced portfolio, and therefore one that can be liquidated without loss, if need be, but provides a good monthly cash flow that can be partly enjoyed and partly reinvested, would be the most comfortable solution: the proverbial squaring of the circle. Unfortunately (or perhaps fortunately, who knows?) this is never the case.

So it happens that in real life and investing, one has to make sometimes painful decisions, hoping to get out of losing situations or positions in the most dignified way possible. As I said, there are six stocks in my portfolio in which I have lost confidence and would plan to liquidate, hoping I can do it without too much damage.

These are CGO, GOF, PDI, QYLD, RYLD, and XFLT, which I would like to replace both by increasing my positions in FDUS and MCI and by adding one or two new CEFs to the portfolio, among those reviewed in my October 2023 article “38 CEFs Worth Exploring.” In my choices I must also keep in mind the tax aspects, which for me as an Italian are often penalizing, as I had the opportunity to illustrate in an article published in April 2023. There will be time to think about it, but the idea is to streamline my fleet and take further steps toward (hopefully) greater portfolio efficiency.

Final Relaxation

As in yoga sessions, here we come to the final relaxation. My overall portfolio this month returned 9.34% on an annual basis, calculated on the last paid or announced dividends/distributions. Although many stocks are still in the red (as you have seen), the overall performance is today around parity, thanks to the different weight given to each security in my portfolio, which has been modeled following my current selection criteria, based on NAV performance.

In recent years there were hard times, but little by little my portfolio as a whole has broken even, proving that financial shortsightedness is not a good counselor and that, in the long run, holding on can be the most profitable strategy for staying alive. But to hold on, one must first know oneself and how our brain reacts in relation to the movements of our portfolio.

We’re back to square one. It is again a matter of “being” before “doing,” as the master I met on the train taught me when I was still a pupil of high hopes. And it will always apply.

Read the full article here

")

")

")