")

(NASDAQ:META)")

")

I really liked AdvisorShares Pure US Cannabis ETF (NYSEARCA:MSOS) early on. This was not the first ETF for the cannabis space, but it was a great effort to help funnel investments into U.S. cannabis operators. The ETF is way down from its peak in early 2021 and from its initial offering price in 2020, but it’s up a lot from the all-time low set in August 2023. I warned investors to avoid MSOS in early August when the stock closed at $5.29, and it fell in late August to a low of $4.78. Of course, this was before the Department of Health & Human Services recommended that cannabis be rescheduled by the DEA, which has excited investors.

In that prior piece, I explained that while stocks seemed very cheap, MSOS, then down about 23% in 2023 and down a lot from when I warned in November of 2022, was not a good buy. The stock is now above $10, more than double off of that all-time low but still below the $11.54 when I explained why I wasn’t a fan of MSOS. In this follow-up, I explain why the ETF is not a good way to invest in cannabis for lots of reasons.

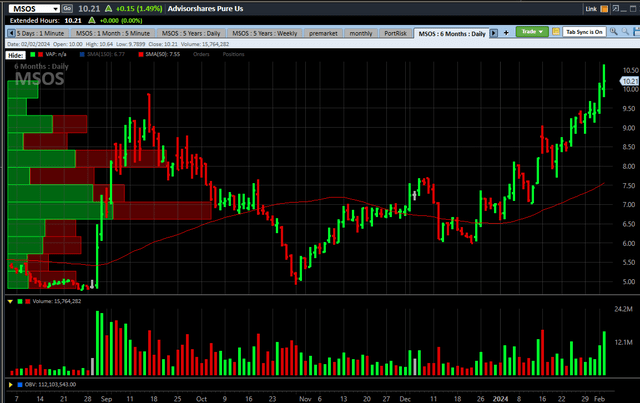

The MSOS Chart Is Scary

As I mentioned above, it is down a lot from the peak. The fund was started in September of 2020 with a small amount of shares. The first trade was at $23.92 on September 4th. It traded to over $50 in February of 2021 before collapsing:

Charles Schwab

The trading in shares has picked up a lot since the potential cannabis rescheduling was announced in late August. Of course, this is not yet a done deal. If the DEA moves from Schedule 1 to Schedule 3, 280E taxation would end. If it were to leave it or to move to Schedule 2, it would not. There is no timeline for the DEA to make a decision.

While the stock has soared over the past five months, it is still below its peak in late 2022. Looking at the shorter-term chart, the explosive rally is evident:

Charles Schwab

MSOS, which closed at its net asset value of $10.21 per share, has more than doubled from its all-time low. The New Cannabis Ventures American Cannabis Operator Index has increased 105.6% since 8/25, while MSOS has expanded by 108.3%. In 2023, MSOS gained 0.3%, while the American Cannabis Operator Index increased 7.6%.

MSOS Remains Poorly Structured

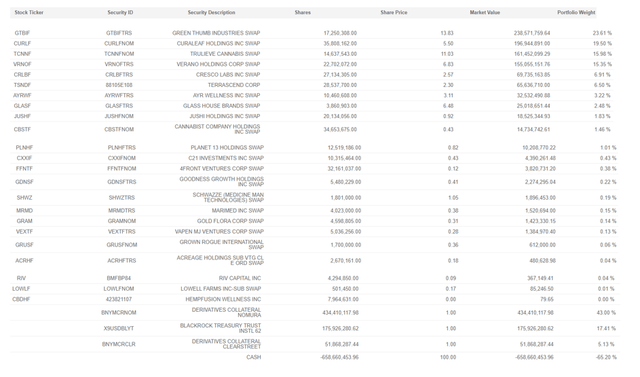

My main concern with the ETF is that it is not at all diversified. The top 2 names, Green Thumb Industries (OTCQX:GTBIF) and Curaleaf (OTCPK:CURLF), which I think is overvalued, make up over 43% of the ETF. The Tier 1 MSOs, which include these and also Trulieve (OTCQX:TCNNF), Verano (OTCQX:VRNOF) and Cresco Labs (OTCQX:CRLBF), are over 81% of the ETF. Adding in the other position above 5%, TerrAscend (OTCQX:TSNDF), brings the top 6 holdings to 88%. Here is the complete list of holdings from their website:

AdvisorShares

12 of the 22 stocks are at less than 0.5%! The fund still doesn’t own Ascend Wellness (OTCQX:AAWH), one of the four Tier 2 names that is up 49% in 2024 so far, well ahead of the top positions in MSOS, which are up less than 36%.

MSOS Is Not Well Run

The ETF claims to be actively managed, but this appears to be not the case. I have followed it a long time, and the relative weightings don’t move that much. 15 months ago, MSOS held 75% in Tier 1 names. In 2023, it moved away from holding any ancillary names, and it was at 75% Tier 1 names in August.

The ETF continues to have no index, which makes no sense to me. On its website, AdvisorShares compares the performance to the North American Marijuana Index, which has a lot of different stocks in it that are not MSOs, and to the S&P 500. It is lagging both since inception. Investors deserve for an “actively managed” ETF to have a benchmark. They also deserve for it to be actively managed.

So, there are problems with MSOS, but that hasn’t stopped it from getting to $1 billion in valuation again. Shares have soared, and the non-diversified ETF has seen its shares outstanding grow 14.1% year-to-date and 57.1% since the end of 2022. Most of that growth has taken place since the potential rescheduling news hit, with shares outstanding increasing 52.2% since 8/25.

Alternatives to MSOS

For those who want to or need to invest in ETFs rather than individual stocks, I shared 15 months ago an alternative. I can no longer suggest that investors consider the ETF that I did then. Until August 29th, when that potential rescheduling news hit, the ETF I had suggested fell almost 47%, while MSOS fell 58%. Since then, MSOS has done better. Unfortunately, there are no good cannabis ETFs in my view.

I continue to believe that investors are better served by buying the 5 top holdings of the fund instead of the fund itself if they want to be in only MSOs. The second largest position, Curaleaf, can be avoided, and I would suggest being less concentrated than MSOS. I don’t include any Tier 1 MSOs currently in either of the model portfolios I offer to subscribers. I do own a Tier 2 name and a smaller one.

The best solution, in my opinion, would be to not invest exclusively in MSOs. While I believe that they can rally further if 280E gets wiped out, they have a lot of downside if not. I have shared some ideas from other sub-sectors that look attractive to me. For those looking to benefit from the rescheduling, my Canadian LPs won’t benefit, but the ancillaries will enjoy healthier customers in my view.

Conclusion

MSOS has soared as investors have piled in. This is apparent in the elevated trading volumes and the increased number of shares outstanding. The ETF is poorly structured, with 88% in just six stocks, a big bet on the largest MSOs. The largest MSOs have higher valuations than some that are a bit smaller, but they are facing issues that prevent them from using their stock to do M&A. Remember the Cresco Labs deal to buy Cannabist (OTCQX:CBSTF)? It was terminated after more than a year.

State regulatory issues are a big challenge, but the bigger risk right now is that 280E doesn’t go away. Not only are these stocks way up compared to the overall sector over the past six months, but there is no natural buyer if 280E remains. The industry is in bad financial shape now, with the balance sheets under pressure at some companies. Curaleaf has a lot of debt and a negative tangible book value. Debts are coming due in the next few years. Equity sales are very difficult right now for MSOs.

Cannabis should be rescheduled, in my opinion, but that doesn’t mean it will happen. If it does get rescheduled to Schedule 3, 280E will be eliminated. This will make MSOs go up even more, but I expect equity sales. If it doesn’t happen, these companies could trade to new lows, which is a big drop from here. Investors should understand that there is a big potential risk in this ETF’s holdings going down substantially. This would make it very difficult for MSOS if it were to face redemptions as it did at the end of 2022 and into 2023.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

(NASDAQ:META)")

")

")