")

")

")

(NYSE:BABA)")

Summary

Following my coverage on MSCI (NYSE:MSCI) in Apr’24, which I recommended a buy rating as I believed the valuation was cheap (stock was oversold) and that the growth outlook was not structurally impaired, this post is to provide an update on my thoughts on the business and stock. MSCI continues to receive a buy rating from me as various indicators suggest growth will continue to be strong. Any slowdown in growth is pretty much due to the uncertain macro environment, which should get better as we get more clarity on the Fed’s decision to cut rates and the US election comes to an end. Valuation is also still cheap when compared to the market.

Investment thesis

On 23-07-2024, MSCI released its 2Q24 earnings, which saw revenue growth of 14% (organic growth was 9.7%), driving total revenue to $707.9 million, beating the street’s estimate for ~12% y/y growth. Every segment contributed to this growth on an organic basis, where index revenue grew 9.8% y/y; analytics revenue grew 11.2%; ESG & Climate revenue grew 10%; and private assets revenue grew 1.3%. By revenue type, recurring subscription revenue grew 14.4%, trending higher than the consolidated level as non-recurring revenue modestly dragged down growth performance (down 15% in 2Q24). EBITDA margins were flat vs. 2Q23 at 60.7%, resulting in an EPS of $3.64, beating consensus estimates of $3.55.

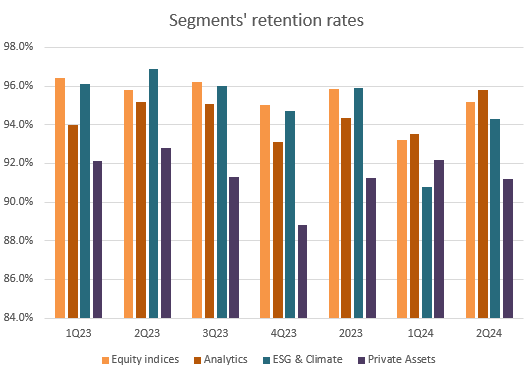

The main negative narrative, I believe, that is preventing the MSCI share price from going higher is probably the macro impact on active asset managers (MSCI’s clients). There is no doubt that MSCI is getting impacted as it leads to clients tightening their budgets, longer sales cycles, and weak index recurring subscription revenue growth of 8% y/y (this is below the historical trend of low-teens growth) due to elevated cancellations. However, I reiterate my view that growth is being delayed and not structurally impaired. If it was indeed a structural impairment to demand, the MSCI retention rate should see a hit as clients churn. However, that is not the case. In fact, retention rates rose across all segments except ESG & Climate (which I also think is temporary due to the US election, as discussed below).

Own calculation

2Q24 results continue to prove that MSCI can continue to grow healthily. Multiple leading indicators support my view. Number one, AUM in ETFs linked to MSCI indexes grew very strongly at 19% to a total of $1.63 billion, and this translated directly into index asset-based fee growth of 18% in the quarter, accelerating from 13% in 1Q24. Given that the market (using S&P as a benchmark) is up so strongly on a year-to-date basis (about 16%), this should continue to drive strong fund inflows into ETFs and non-listed products linked to MSCI indices.

Number two, the robust performance seen in MSCI’s Analytics segment (11% growth in 2Q24) shows that MSCI is also benefiting from the uncertain macro environment. Specifically, MSCI addresses investment managers need for analytical tools to better facilitate credit and liquidity risk in the current economic environment. My expectations are that the macro situation will stay uncertain at least until the end of this year, as the Fed has not specifically called out when they are cutting rates and the US election is in November. As such, Analytics segment growth should remain elevated.

Number three, to improve its private company ESG coverage, MSCI has entered into a partnership with Moody’s [MCO] private company database, Orbis. In return, MSCI will provide MCO with data on its ESG scores. This partnership doesn’t seem to be short-term as in 2025, both parties agreed to expand the partnership into private credit. This is a massive win for MSCI because it significantly enhances the value proposition of its ESG & Climate offering instantly to clients – which also makes MSCI stickier. Investors might be concerned that this segment’s growth has slowed by 100bps to 10% vs 1Q24, but I don’t think this is an area of concern. The reason for the slowdown is likely due to US clients pulling back their investments for the time being as they are uncertain about the upcoming US election – which will impact policies related to ESG. There is no structural impairment to growth at all, as other regions like EMEA grew 17% and APAC grew 20%. My view is that this segment growth will recover post the election, and overall segment growth will inflect upward again.

Valuation

Own calculation

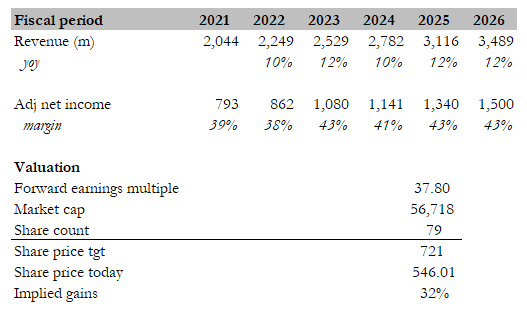

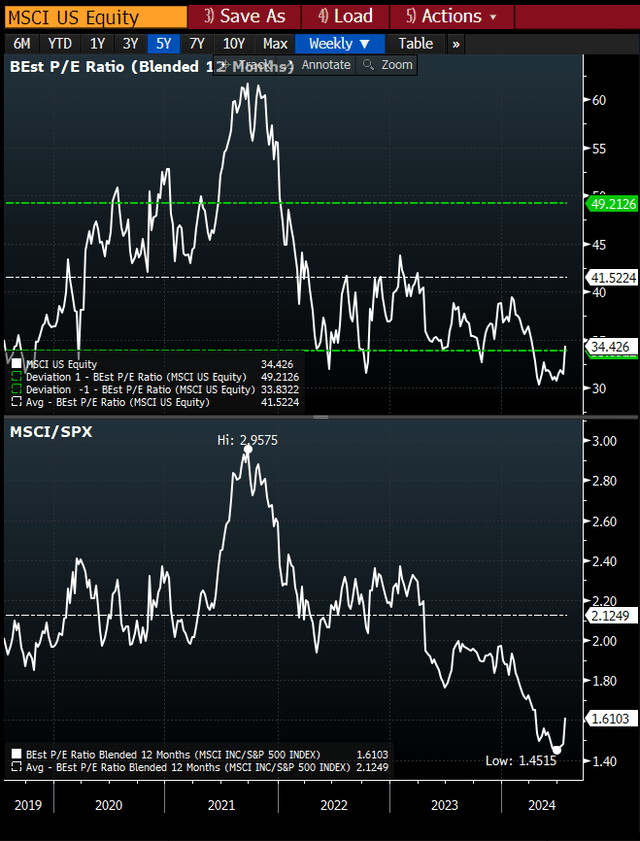

Even after the sharp increase in the share price, I still believe there is an attractive upside to the share price. My revisited price target is now $721 based on FY26e estimates (my previous price target was $552 based on FY25e estimates). In this revised model, I have brought down my FY24 estimates as I recognize the current uncertain macro situation will likely persist until the end of the year. However, post FY24, I am expecting MSCI to revert back to its normalized growth and margin profile (12% growth and 43% net margin). The variable here is what multiple MSCI should trade at, and I think the best way is still to anchor expectations against the S&P500 multiple. My previous view was that MSCI would trade back to ~1.8x of S&P’s average PE multiple, and this ratio has moved in my expected direction after the market recognized MSCI’s strong 2Q24 results. In a normalized environment, I believe this ratio will continue to trend back to the average level of 2.1x. Doing the same math and attaching 2.1x to the S&P average multiple of 18x, I believe MSCI will trade up to 38x forward PE. This is roughly the average the MSCI has been trading at over the past 5 years if we remove the COVID period where multiples went above 41x.

Bloomberg

Risk

The US commercial real estate industry is at risk of falling even further, and so far, the impact has been prominent in MSCI’s results, where private assets organic revenue growth came in weak at 1% y/y in 2Q due to a commercial real estate slowdown, which impacted demand for MSCI’s transaction data products. If the industry blows up, it could drag down overall topline performance for MSCI. This could put a ceiling on how high valuations could potentially rerate in the near term.

Conclusion

In conclusion, I reiterate my buy rating for MSCI. While the macro environment is impacting active asset managers, my view is that MSCI’s growth is delayed, not impaired, as evidenced by rising AUM in ETFs and client retention. The uncertain environment until the US election also benefits MSCI’s Analytics segment. As for the slight weakness in ESG & Climate, it is likely temporary due to investors’ concerns about how policies related to ESG may change after the election. Lastly, valuation remains attractive with upside potential.

Read the full article here

")

")

")

(NYSE:BABA)")