")

")

In my previous article published in March 2024, I discussed Motorola Solutions’ (NYSE:MSI) growth in APX NEXT replace cycle for FY24. Motorola released its Q2 result on August 1st, reporting a record sales and operating profits. I like the company’s leadership in both the Video and Land Mobile Radio Communications markets, and their new product launches could drive the company’s future growth. I reiterate a ‘Buy’ rating with a fair value of $460 per share.

Video and LMR Growth

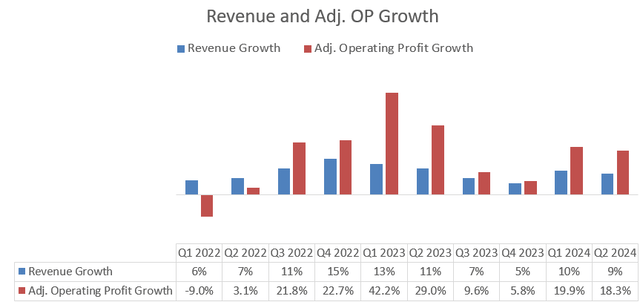

Motorola continues to deliver robust growth in both Video Security and Access Control (Video) and Land Mobile Radio Communications (LMR), with year-over-year growth of 10% and 9%, respectively. Thanks to the strong growth in video security and LMR, Motorola achieved a 9% growth in revenue and an 18.3% in adjusted operating profits, as shown below.

Motorola Quarterly Earnings

I anticipate the strong growth in Video and LMR will sustain in the near future. Key reasons are:

- As discussed in my previous coverage, video business represents a very important growth opportunity for Motorola, encompassing both fixed and mobile video products and solutions. These video products can provide end-to-end security ecosystem for the public sector, offering capabilities to detect, analyze, communicate and respond. The structural growth driver is the increasing demand for public safety from government and public safety customers. Motorola has been investing heavily in their Video business lines, launching several innovative products such as video recorder offering on both on-premises and cloud platforms.

- Motorola has a huge install base for their LMR products, with customers increasing relying on Motorola’s upgrades and services, as indicated over the earnings call. Motorola is a global leader in the two-way radio category among several solutions including Project 25 etc. As analyzed in my previous article, Motorola is benefiting from the multi-year APX NEXT refreshment cycle. The replacement of outdated technology could help Motorola generate higher revenue in the near future.

- On June 27th 2024, Motorola announced the launch of VESTA NXT, a powerful 911 software designed to maximizes call handler speed and efficiency. In addition, on May 20th, the company launched the new TETRA radio MXP660 solution, which enables the first responder to automatically switch between walkie-talkies and broadband networks. I favor the company’s efforts to launch innovative products to further monetize their customer base and gain market share.

Outlook and Valuation

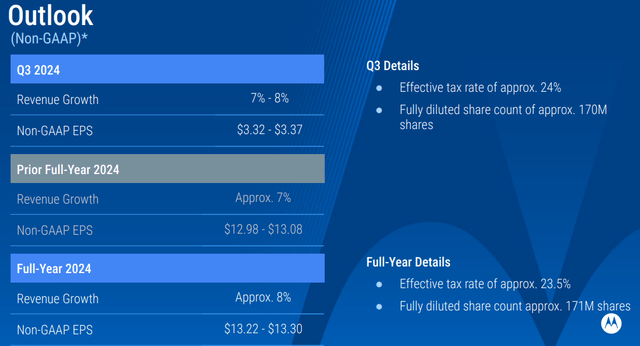

Due to the strong backlog and past performance, Motorola is raising the full-year revenue growth guidance to 8%, as detailed in the slide below.

Motorola Investor Presentation

I believe Motorola will deliver high-single-digit revenue growth in the near future for the following reasons:

- LMR: The future growth in LMR will be primarily driven by refreshment cycle, as discussed in my previous article. Last year, Motorola faced challenges with their global supply chain, but they have gradually resolved the problem, resulting in improved LMR supplies in Q2. As a result, Motorola has been able to reduce lead times for shipment and deliveries. Considering the strong performance in the first half, I estimate the LMR will grow by 10% in FY24.

- Video: Motorola launched their Avigilon Unity Video 8 software, formerly known as Avigilon Control Center, a leading solution for surveillance and security systems. The next-generation ACC 8 video management system could reinforce Motorola’s market leader position. Additionally, Motorola is advancing their cloud solutions for the video management, which could potentially make their business more recurring in nature. I forecast the business will grow by 12% in FY24.

- Command Center: I expect Motorola will maintain its growth momentum, delivering an 8% year-over-year growth in revenue.

From FY25 onwards, I estimate that Motorola will grow its revenue by 9% assuming: 9% growth in LMR, 9% in Video and 8% in Command Center, all aligned with historical average.

My biggest takeaway from the quarter is their robust margin expansion, delivering 210bps margin expansion in Q2. The management is guiding for 100bps margin expansion for FY24. I model 40bps normalized margin expansion assuming: 20bps from gross profits due to new product launch and an increasing mix towards software/services, 10bps from operating leverage in R&D, and 10bps from operating leverage in SG&A.

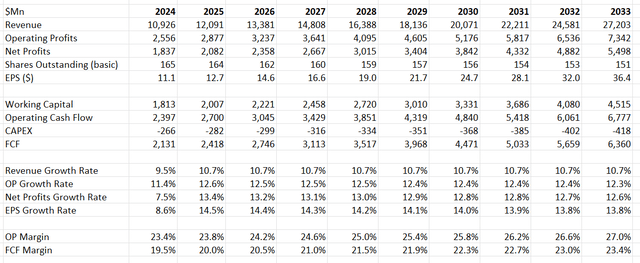

The DCF can be summarized as follows:

Motorola DCF

The discount rate is calculated to be 9% assuming: risk-free rate 3.8%; beta 0.8; equity risk premium 7%; cost of debt 7%; equity $71 billion; debt $6 billion; tax rate 23.5%.

The fair value is calculated to be $460 per share after discounting all the future FCF and adjusting the net cash balance.

Downside Risks

In October 2021, the CMA opened a market investigation into Airwave, which was acquired by Motorola in 2016. Airwave provided voice and data communications to emergency services in the UK. As disclosed by the company, Motorola’s backlog for Airwave services contracted with the U.K. Home Office through December 31, 2026, was reduced by $777 million. Currently, Motorola is still filing proceedings against the Home Office in UK, and the outcome of the lawsuit remains uncertain. During the recent earnings call, most financial results were disclosed excluding the impact from the Home Office. However, the Home Office headwinds might persist for years.

Closing Thoughts

Public safety is a highly attractive sector for investments, and Motorola’s global leader position enables them to sustain high-single-digit revenue growth, in my view. I reiterate a ‘Buy’ rating with a fair value of $460 per share.

Read the full article here

")

")