: Back To Its Margin Expansion And Hyper Growth Path")

")

")

: Brand Name BDC Yield 10% With Defensive Portfolio")

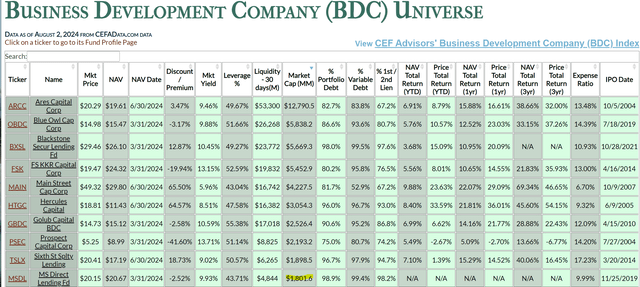

Several holdings in my Income Compounder portfolio include BDCs, which are attractive to income investors like me due to the requirement for them to distribute 90% of taxable income each year when they are registered as RICs (Regulated Investment Companies). Schwab offers more information on BDCs that helps to explain what makes them attractive as an investment and why there are so many of them popping up over the last few years. According to the BDC Universe website from CEFdata.com, there are now about 50 publicly traded BDCs available for investors to choose from.

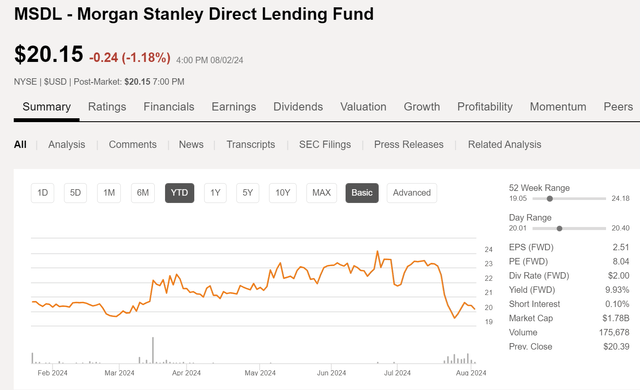

One of the newest BDCs to do an IPO in recent years is the Morgan Stanley Direct Lending Fund (NYSE:MSDL). The company was founded in 2019 and went public via an IPO in January 2024. According to the January 16 press release, the IPO price was $20.67 and 5M shares were issued with an allotment to issue another 750K shares.

Morgan Stanley Direct Lending Fund (“MSDL”), a business development company externally managed by MS Capital Partners Adviser Inc., today announced that it has commenced an initial public offering of 5,000,000 shares of its common stock, par value $0.001 per share (the “Common Stock”). The estimated price for the offering is $20.67 per share of Common Stock.

As of the market close on August 2, 2024, MSDL was trading for $20.15, or about $.50 below the IPO price and now offers a market yield of 9.9%.

Seeking Alpha

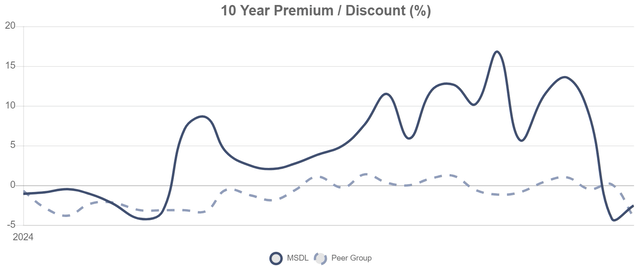

Part of the reason for the big price drop at the end of July was due to the expiry of the lockup period for some of the IPO shares. Also, the broader market correction in July and negative price action on BDCs in general due to expectations of headwinds from lower interest rates on the horizon likely contributed to the fall from $23 in mid-July down to the low $20 range in the past couple of weeks. The BDC had been trading at a premium to book value for most of the year up until mid-July as well. The chart below from cefdata.com shows the premium dropping from a high of about 13% (above NAV) to a low of -4% discount before rising to the current discount of -2%.

cefdata.com

Although the timing of the IPO may not have been ideal, the backing of Morgan Stanley (MS) and the defensive nature of the portfolio along with a high-yield quarterly distribution puts this new BDC on my watch list. This may be an investment worth considering if you believe that the economy in the US is not about to enter a recession, and you are looking to add a high quality, well-positioned BDC to your income portfolio. For me personally, I would like to wait and see what happens over the next few months before deciding whether to add shares of MSDL to my own income portfolio. First things first though, so let’s see what they have to say on the Q2 2024 earnings call scheduled for August 8 after the market closes.

Is MSDL a Compelling Investment Opportunity?

From the company website, this paragraph describes the BDC and its relation to Morgan Stanley:

Morgan Stanley Direct Lending Fund is a business development company with the objective to achieve attractive risk-adjusted returns by investing primarily in directly originated senior secured term loans issued by U.S. middle market companies. We are externally managed by MS Capital Partners Adviser Inc. (the “Adviser”), an indirect, wholly owned and consolidated subsidiary of Morgan Stanley. We are not a subsidiary of or consolidated with Morgan Stanley.

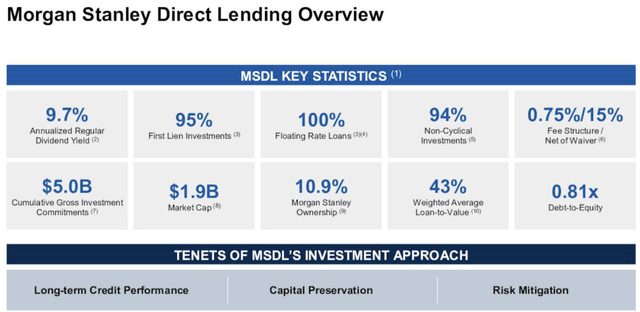

According to company Q1 2024 presentation materials the factors that make MSDL stand out as a BDC that you may want to invest in include: brand recognition with the Morgan Stanley name, a defensive portfolio focused on first lien and floating rate loans, a rigorous investment process and experienced management team, strong financial position, shareholder friendly with its 10% yield, and is well positioned in attractive direct lending opportunities.

Furthermore, the tenets of the BDC’s investment approach are laid out in this overview slide of MSDL and include long-term credit performance, capital preservation, and risk mitigation.

MSDL Q124 earnings presentation

Brand recognition with the MS connection is a significant selling point based on comments made by President and CEO Jeff Levin:

I would also highlight that we believe the quality of our origination activity remained high and we served as the lead or joint lead arranger on about 80% of Morgan Stanley direct lending new platform originations during the first quarter. We believe this showcases our ever-increasing presence in the marketplace and private equity firms’ preference for us as a partner.

We believe sponsors want to work with us, not just because of the extensive experience of our investment team, but also due to the strategic benefits that come with partnering with Morgan Stanley and that this structure is unique in the direct lending ecosystem and will continue to differentiate us as investors.

With a current market cap of about $1.8B (the slide above shows $1.9B, but that was as of 3/31/24), according to the BDC Universe website that ranks MSDL #10 based on size, just behind TSLX.

BDC Universe

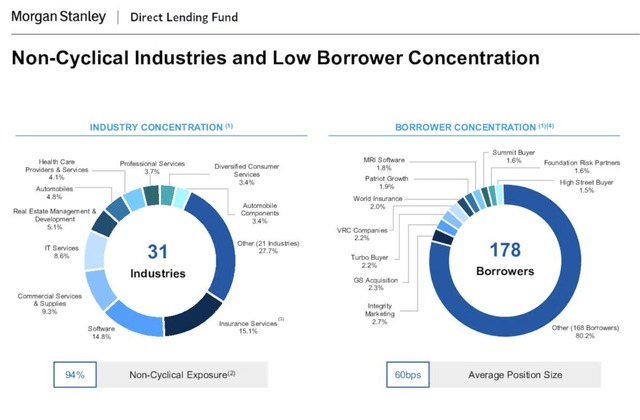

The defensive nature of the portfolio includes holdings that are somewhat recession resistant and have a high degree of exposure to non-cyclical industries like software and insurance.

MSDL Q124 presentation

The BDC has access to private equity, and according to CEO, Levin, those private equity sponsors are sitting on record levels of cash that they are itching to invest:

Private equity sponsors are sitting on record levels of dry powder and they are motivated to put that capital to work. The fact that debt financing is abundant as well, both in terms of private debt capital, as well as due to the fact that the broadly syndicated loan market is functioning, could serve as another catalyst to help jumpstart sponsor-related M&A activity.

The loans that MSDL makes to middle market companies include mostly floating rate, first lien (94%) assets. The defensive nature of the loan portfolio is evident from the summary provided by CFO David Pessah regarding Q1 results:

At the end of the first quarter, our weighted average loan-to-value was 43% and the weighted average EBITDA of our portfolio companies was $155 million. Additionally, the median EBITDA of our portfolio companies was $82 million. As of March 31st, our weighted average yield on debt and income-producing investments was 12% at fair value and 11.9% at cost.

With respect to our internal risk ratings, as of March 31, 2024, over 98% of our total portfolio had an internal risk rating of 2 or better, which is unchanged relative to the December 31, 2023 period. Additionally, we had three investments on non-accrual status, representing approximately $12.4 million or 40 basis points of the portfolio at cost, which is down from 60 basis points as of December 31, 2023.

Peer BDC Comparisons

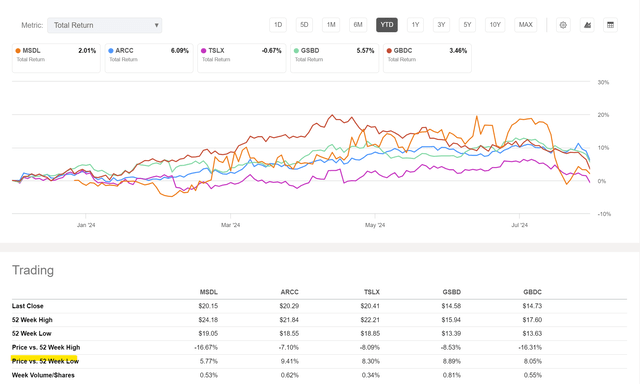

Although Ares Capital (ARCC) is a much larger BDC and has been around much longer, MSDL compares favorably on a YTD basis, which is the only way to compare them since MSDL has only been trading on the NYSE since January. It has also performed more or less in line with other peer BDCs such as TSLX, GBDC, and GSBD on a YTD total return basis, all of them within 10% of their 52-week low price.

Seeking Alpha

Yet, even though prices have been getting hammered in July many BDCs continue to perform well into Q2, and if ARCC is any indication based on its earnings report MSDL should likely benefit from the same strong credit market and a more active environment for direct lending. From the ARCC Q2 2024 earnings call, CEO Kipp DeVeer explained that the current market environment at the end of Q2 remained strong and activity picked up over the prior quarter.

Throughout the second quarter of 2024, we saw a healthy and improving market environment for companies seeking our flexible capital solutions. And we observed a particularly clear acceleration in private equity sponsor activity as most sponsors are seeking capital to support the growth of their portfolio companies and exit investments as they work to increase distributions from aging fund vintages. Against this backdrop, direct lenders have continued to represent a meaningful part of leverage buyout transactions during the quarter, underscoring the importance of direct lending solutions in the current market.

It is difficult to compare a new BDC like MSDL that just did an IPO seven months ago to ARCC, which has been around for 20 years and has a market cap about 7 times larger. However, ARCC also takes a defensive approach to portfolio construction with strong origination activity, a well-covered dividend, and a similar focus on first lien, senior secured loans. In time, perhaps MSDL can build its way up to become a true peer to ARCC.

Risks to BDC Future Performance

The biggest risk to not only MSDL but to most BDCs right now is the sudden slowdown in the US economy as evidenced by recent news reports of a weakening labor market, slowing consumer spending even as inflation cools off, and lower than expected sales traffic across industries.

While this is good news for interest rates and the likelihood of a Fed cut in September, which could stimulate growth stocks and lead to more lending opportunities as loans get refinanced or extended, a weaker consumer and slowing economy overall would likely lead to a continued selloff in the stock market for most BDCs. Even if MSDL reports a strong second quarter, the writing might be on the wall for a less vibrant economy in the second half of 2024, especially with all the uncertainty around the November elections.

On the other hand, MSDL could be ramping up the portfolio by taking advantage of all the dry powder in private credit that is looking for a home. If the economy does slow down, MSDL may be able to get through a rough patch without too much (more) damage to the stock price.

There is also increasing competition in the BSL (Broadly Syndicated Loan) market that could pose a competitive threat to MSDL. In fact, a question was asked by one analyst on the Q1 earnings call specifically about that risk. The response from CEO Levin acknowledged that threat:

Q: It seems there’s been some proactive repricing on some investments, particularly some outperformers in portfolios where they might have other options as the BSL market has opened up. I’m curious how you’re thinking about that.

A: It’s certainly no secret that the syndicated loan market has become extraordinarily strong and is a, I’d say, a significant competitive threat to the largest end of the private credit market. So the businesses that have access to the syndicated loan market now, of course, are actively contemplating what the right product is.

I think private credit, from a macro standpoint, will continue to grow over time, irrespective of the health of the public credit market, for a lot of the reasons why businesses of all sizes, including large, do use private credit.

But repricing volume unquestionably has picked up in Q1. I think it’ll continue to over the course of the year, assuming the public markets stay as healthy as they are today and maybe they tighten further. Who knows? So that’s something that we’re watching closely. I think one way that we’re somewhat well positioned relative to some of our competitors is that, our portfolio does span up and down the size spectrum.

Summary: Wait, Listen, Observe

For now, I am happy hanging on to several BDCs that I currently hold in my Income Compounder portfolio, three of which I discussed in a previous article. I also now hold a position in the Putnam BDC Income ETF (PBDC), which has several top performing BDCs in its portfolio, including ARCC, MAIN, OBDC, BXSL, HTGC, FSK, and a few others. PBDC also acts as a sort of proxy for the broader higher quality BDC universe (in my opinion) and although it is also relatively new to the public market, it has demonstrated strong performance so far in 2024.

While MSDL has a strong pedigree and what appears to be a rigorous defensive portfolio positioning strategy with a well-covered $0.50 quarterly dividend, I am not yet convinced that this is a good time to pull the trigger and buy shares just yet. I expect to learn more when the company reports Q2 earnings on August 8 and will re-evaluate my thesis at that time. Meanwhile, I am holding shares of several existing BDCs in my portfolio and collecting the income from them each quarter.

Read the full article here

: Back To Its Margin Expansion And Hyper Growth Path")

")

")

")