")

By Kevin Flanagan

This blog post represents the third installment in my Money in Motion series. With rate cuts now definitively expected by the bond market at the September Federal Open Market Committee (FOMC) meeting, some perspective is in order. Specifically, even when the Federal Reserve begins their rate-cutting process, the starting point for U.S. Treasury yields is far above where they stood during the Fed’s last, pre-COVID, round of policy easing. In other words, money will be in motion in a new rate regime.

For investors, that means bond portfolio decision-making will be occurring against a rate backdrop that many market participants have not experienced before. There is one asset class that specifically stands out in this investment landscape as being the highest-yielding Treasury security…floating rate notes.

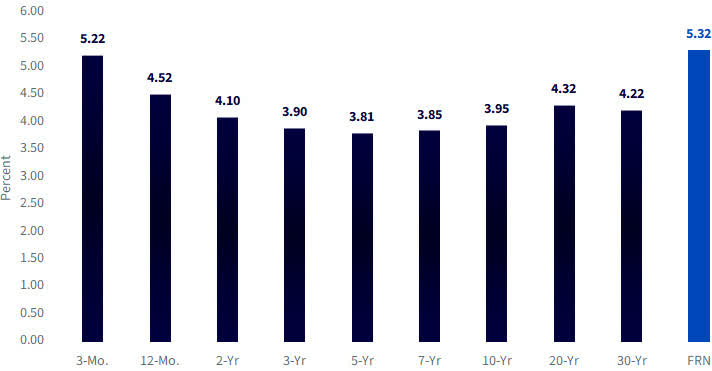

U.S. Treasury Yields

Source: Bloomberg, as of 8/15/24.

Without a doubt, the recent rally in the Treasury market has been rather noteworthy, with yields visibly declining from the 12-month t-bill all the way out to the 30-Year bond. These declines have been the direct result of continued disinflationary trends, but perhaps more importantly, concerns that the labor market may finally be weakening. This narrative has given rise to a more aggressive expectation for Fed rate cuts.

Arguably, the UST market is perhaps the most well-known discounting mechanism on the planet, i.e., a platform that quickly prices in changes in global investor expectations. This is why I believe UST yields are at their current readings. However, as I pointed out in last week’s blog post, at some point, validation needs to occur.

Interestingly, there is one sector of the Treasury market that is not based on speculation: FRNs. UST FRNs are priced based on changes in the weekly 3-month t-bill auction, with a spread. As a result, the yield for FRNs is tied more directly to the actual Fed Funds trading range. As expectations for a Fed policy move come into better focus, as is presently the case, the weekly auction yield can reflect what is expected at the next FOMC meeting… not what is expected months from now. So, while the UST 2-Year yield has plunged by nearly 90 basis points (BPS) since late May, the UST FRN yield has declined only 15 bps over this same period. This development has not only kept the FRN as the highest-yielding Treasury security, it has widened the gap versus the 2-Year by 70–75 bps.

As I mentioned in my opening, rate cuts are now definitively a part of the investment landscape, but as we have seen over the last couple of weeks, expectations regarding where the Fed rate-cutting cycle policy will be heading can change quickly. With disinflationary trends intact, Fed rate cut decisions (25 or 50 bps) will most likely be centered on jobs, jobs, jobs. This type of investment setting will more than likely remain a key part of the overall landscape, keeping the magnitude for Fed rate cuts fluid.

Solution

With Treasury FRNs already discounting a 25-bps rate cut at the September FOMC meeting, the yield is still head and shoulders above the other securities on the UST maturity spectrum. The WisdomTree Floating Rate Treasury Fund (USFR) offers investors a solution to try and take advantage of this yield discrepancy.

Important Risks Related to this Article

There are risks associated with investing, including the possible loss of principal. Securities with floating rates can be less sensitive to interest rate changes than securities with fixed interest rates, but may decline in value. Fixed income securities will normally decline in value as interest rates rise. The value of an investment in the Fund may change quickly and without warning in response to issuer or counterparty defaults and changes in the credit ratings of the Fund’s portfolio investments. Due to the investment strategy of this Fund it may make higher capital gain distributions than other ETFs. Please read the Fund’s prospectus for specific details regarding the Fund’s risk profile.

Kevin Flanagan, Head of Fixed Income Strategy

As part of WisdomTree’s Investment Strategy group, Kevin serves as Head of Fixed Income Strategy. In this role, he contributes to the asset allocation team, writes fixed income-related content and travels with the sales team, conducting client-facing meetings and providing expertise on WisdomTree’s existing and future bond ETFs. In addition, Kevin works closely with the fixed income team. Prior to joining WisdomTree, Kevin spent 30 years at Morgan Stanley, where he was Managing Director and Chief Fixed Income Strategist for Wealth Management. He was responsible for tactical and strategic recommendations and created asset allocation models for fixed income securities. He was a contributor to the Morgan Stanley Wealth Management Global Investment Committee, primary author of Morgan Stanley Wealth Management’s monthly and weekly fixed income publications, and collaborated with the firm’s Research and Consulting Group Divisions to build ETF and fund manager asset allocation models. Kevin has an MBA from Pace University’s Lubin Graduate School of Business, and a B.S in Finance from Fairfield University.

Original Post

Read the full article here

")