")

")

")

")

")

In an ideal world, every investment call would look like a straight line up. You buy the stock low, and it would go up immediately and achieve your desired return. Unfortunately, we don’t live in such a reality. Calls sometimes don’t go as anticipated. And other times, they do go the way that we want, but they require time to get there. One company that I think fits in this latter category is MillerKnoll (NASDAQ:MLKN), a furniture and lifestyle retail business that I last wrote about in early March of this year.

In that article, I acknowledged that the company was seeing a decline in revenue because of economic factors. But I found myself impressed with bottom line performance that was robust. Add on top of this how shares were priced, and I ended up concluding that I was ‘cautiously optimistic’ about the business and its prospects. This led me to rate it a ‘buy’. Since then, things have not gone exactly according to plan. While the S&P 500 is up 10.1%, shares of MillerKnoll are up only 0.6%. Looking at the picture again though, I remain cautiously optimistic. But it is important to keep in mind that the picture can always change.

It just so happens that the next change, for better or worse, is going to be occurring later this month when, on September 19th after the market closes, management will be reporting financial results covering the first quarter of the company’s 2025 fiscal year. Analysts do expect a decline in revenue. However, they see profits and adjusted profits coming in higher than what they did last year. So long as the company does not post results that are worse than this, I think that keeping it rated a ‘buy’ is not a bad decision.

A fresh look

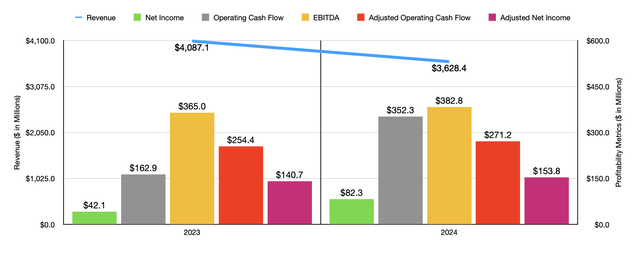

What I last analyzed MillerKnoll earlier this year, we only had data covering through the second quarter of the 2024 fiscal year. Results now extend through the final quarter of that year. Fundamentally speaking, 2024 ended up being a rather mixed time for the company. Take revenue as an example. During the year as a whole, sales came in at $3.63 billion. This is a decrease of 11.2% compared to the $4.09 billion the company generated one year earlier. Looking deeper into the data, management said that all of its operating segments reported lower volumes. But there were other contributors to this as well. For instance, the company closed its Fully business in 2023. It also ended up closing its HAY eCommerce channel in North America. Plus, in the 2023 fiscal year, the company had one extra operating week that added to sales. That extra week helped the company to the tune of $71.7 million. On an organic basis, the drop in revenue was a more modest 8.1%.

Author – SEC EDGAR Data

For most companies, particularly those that operate in hyper-competitive, low margin industries, you would expect a decline in revenue to bring with it a decline in profits as well. But the exact opposite occurred here. Management actually saw net profits nearly double from $42.1 million to $82.3 million. This was mostly the result of a surge in gross margin from 35% of sales to 39.1%. Management attributed this to higher prices, channel optimization strategies, reduced commodity prices, a reduction in storage and handling costs, lower freight and product expenses, and synergies associated with the firm’s acquisition of Knoll. In fact, on synergies, management said that they have achieved annualized run rate cost savings associated with Knoll in the amount of $160 million.

Other profitability metrics have followed suit. As an example, adjusted net income grew from $140.7 million to $153.8 million. This disparity is mostly because of a larger add-back in 2023 associated with impairment charges. Operating cash flow more than doubled from $162.9 million to $352.3 million. A more appropriate metric for this would be adjusted operating cash flow, which strips out changes in working capital. It rose a more modest 6.6% from $254.4 million to $271.2 million. Meanwhile, EBITDA for the business grew from $365 million to $382.8 million.

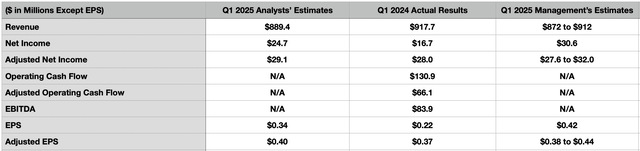

At the start of this article, I mentioned that management will be reporting financial results covering the first quarter of the 2025 fiscal year. The current expectation set by management is for the company to achieve revenue of between $872 million and $912 million. Even at the high end, this should be below the $917.7 million the company reported for the first quarter of 2024. Analysts also anticipate a decline in sales, with the current forecast calling for revenue of $889.4 million.

Author – SEC EDGAR Data

*Management’s ‘estimate’ for EPS and Net Income are based on midpoint extrapolations the author conducted that stemmed from detailed guidance provided by management.

On the bottom line, management said that adjusted earnings per share should be between $0.38 and $0.44. This implies adjusted net profits of between $27.6 million and $32 million. By comparison, in the first quarter of 2024, MillerKnoll reported adjusted earnings per share of $0.37, which translated to adjusted profits of $28 million. Analysts expect a reading of about $0.40 per share, or $29.1 million. As for GAAP earnings, management is calling for a midpoint reading of about $30.6 million. That would imply a per share profit of $0.42, which would be comfortably above the $0.22 per share, or $16.7 million, the company reported one year earlier. Analysts, for their part, are calling for earnings per share of $0.34, which would imply net profit of about $24.7 million. We don’t know what else analysts are anticipating or what management thinks will occur. But in the table above, you can see other important metrics and what they came in at during the first quarter of 2024.

Author – SEC EDGAR Data

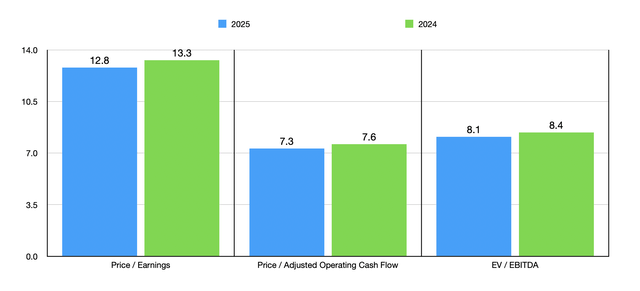

For the year as a whole, management is forecasting adjusted earnings per share of between $2.10 and $2.30. At the midpoint, that would be net profits of about $159.8 million. If we assume that other profitability metrics will rise at a similar rate, then we would anticipate adjusted operating cash flow of $281.8 million and EBITDA of $397.7 million. Using these estimates, as well as historical results for the 2024 fiscal year, we can see how shares of the company are valued in the chart above. On its own, particularly compared to cash flows, MillerKnoll appears to be attractively priced. In the table below, I then compared it to five similar businesses. On a price to earnings basis, only one of the five companies was cheaper than our target. The same holds true on an EV to EBITDA basis, though one other company was tied with it. But on a price to operating cash flow basis, three of the five companies ended up cheaper than our candidate.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| MillerKnoll | 13.3 | 7.6 | 8.4 |

| HNI Corporation (HNI) | 22.4 | 9.4 | 10.8 |

| Steelcase (SCS) | 18.6 | 6.9 | 8.1 |

| Interface (TILE) | 16.8 | 8.6 | 8.4 |

| Pitney Bowes (PBI) | 70.4 | 6.3 | 41.5 |

| ACCO Brands (ACCO) | 10.5 | 3.1 | 10.9 |

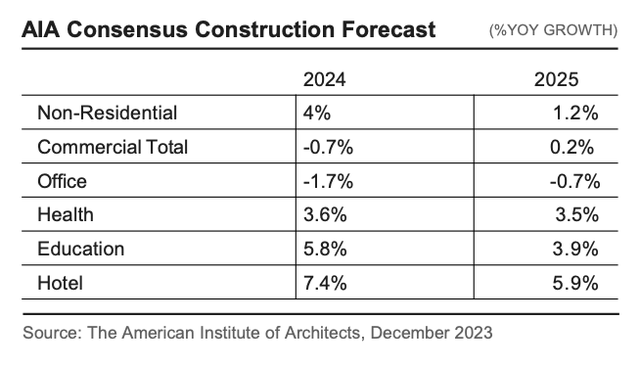

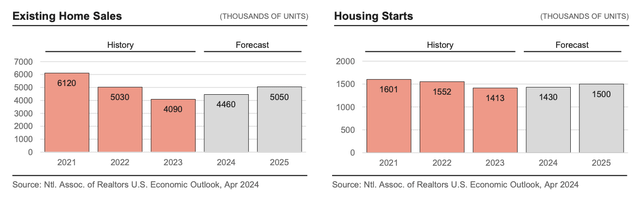

All things considered, this makes MillerKnoll appear to be attractively priced on an absolute basis and slightly appealing on a comparable basis. In the long run, I fully expect the company to do reasonably well. Already, it is doing fine in a difficult environment. However, the company should benefit from certain economic factors as time goes on as well. In the first image below, you can see projected construction related activity for this year and next year. If everything goes according to plan, the company should benefit from growth in most markets. Really, everything other than office construction should fare well. And in the subsequent images below, you can see existing home sales data and housing starts. The fact of the matter is that, as a furniture and lifestyle company, the company benefits from robust housing activity. When people move into a new home or construct a home, they often need to furnish it. Existing home sales have been projected to rise this year and next. And housing starts, after bottoming out last year, should also do the same.

MillerKnoll MillerKnoll

Takeaway

Based on the data currently available, I find MillerKnoll to be an interesting prospect. Because of the market it’s in and the decline in sales that the company has experienced, I wouldn’t exactly call it a top-tier prospect. But for those interested in this space, it’s clear that management knows what it’s doing. Shares are reasonably attractive, and market data suggests that the future for the company should be at least modestly bright. Given this combination of factors, I think that keeping the company rated a soft ‘buy’ is appropriate right now.

Read the full article here

")

")

")

")

")