")

")

By Maria Sanchez

When it comes to integrating environmental, social and governance (ESG) factors into investment strategies, market participants may be interested in deviations from the benchmark. Tracking error is a widely used metric that helps measure the size of these deviations. Improving the ESG profile of a composition often means accepting a higher tracking error due to screening or selection processes. Investors typically seek ESG indices that offer similar risk/performance profiles to traditional benchmarks.

It is important to note that for the S&P 500® ESG Index, there is no guarantee of a specific level of tracking error, as that is not a target in the optimization process. This is a consequence of the index construction, which maintains similar sector and industry weights as the benchmark without drastically altering the composition’s risk profile. As a result, it has historically maintained relatively low tracking error, with the index consistently mirroring the benchmark.

The S&P 500 ESG Index reduces deviations from the S&P 500 through its methodology.1

- Objective: The S&P 500 ESG Index measures the performance of securities from the S&P 500 that meet sustainability criteria and maintains similar overall industry group weights as the underlying index.

- Construction: It applies sustainability eligibility criteria, then uses S&P Global ESG Scores to select constituents. It targets 75% of the market cap within each industry group and chooses the top ESG performers, seeking sector neutrality.2

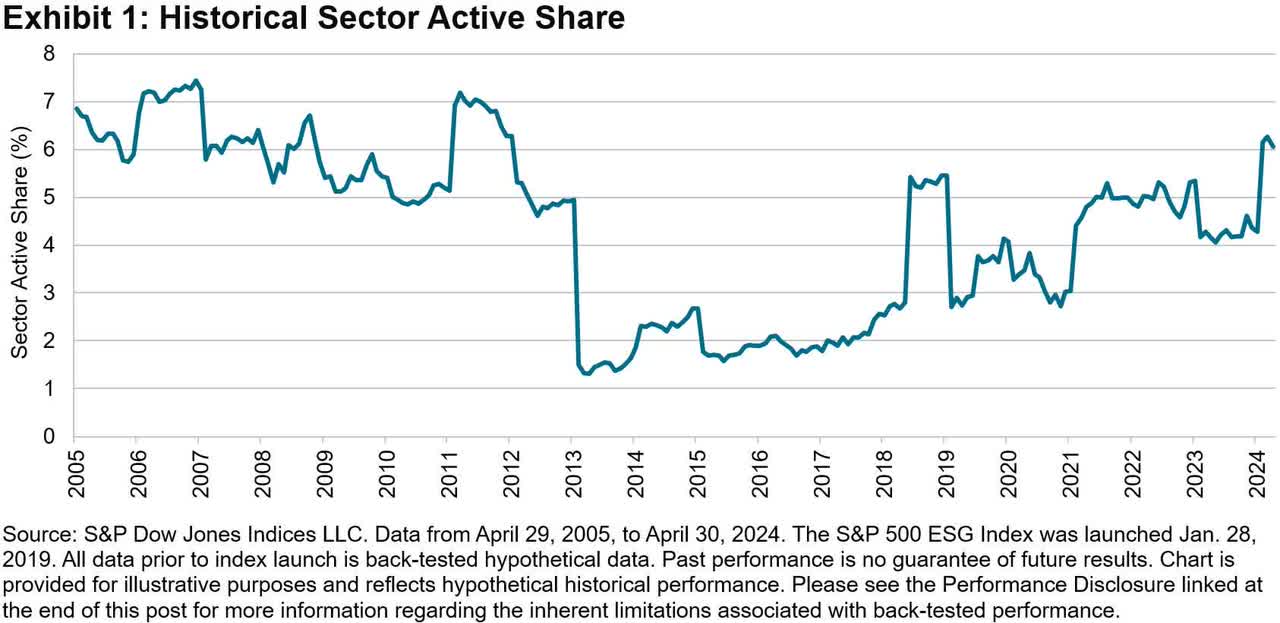

While there may be some deviations from the underlying index due to screening and selection based on criteria such as certain business involvement with specific thresholds, violations to global standards such as the United Nations Global Compact (UNGC), and low ESG scores, the S&P 500 ESG Index demonstrated a low sector active share3 of 4.2% on average from its launch on Jan. 28, 2019, to April 30, 2024. This implementation of the methodology helps ensure consistent tracking of the benchmark (see Exhibit 1).

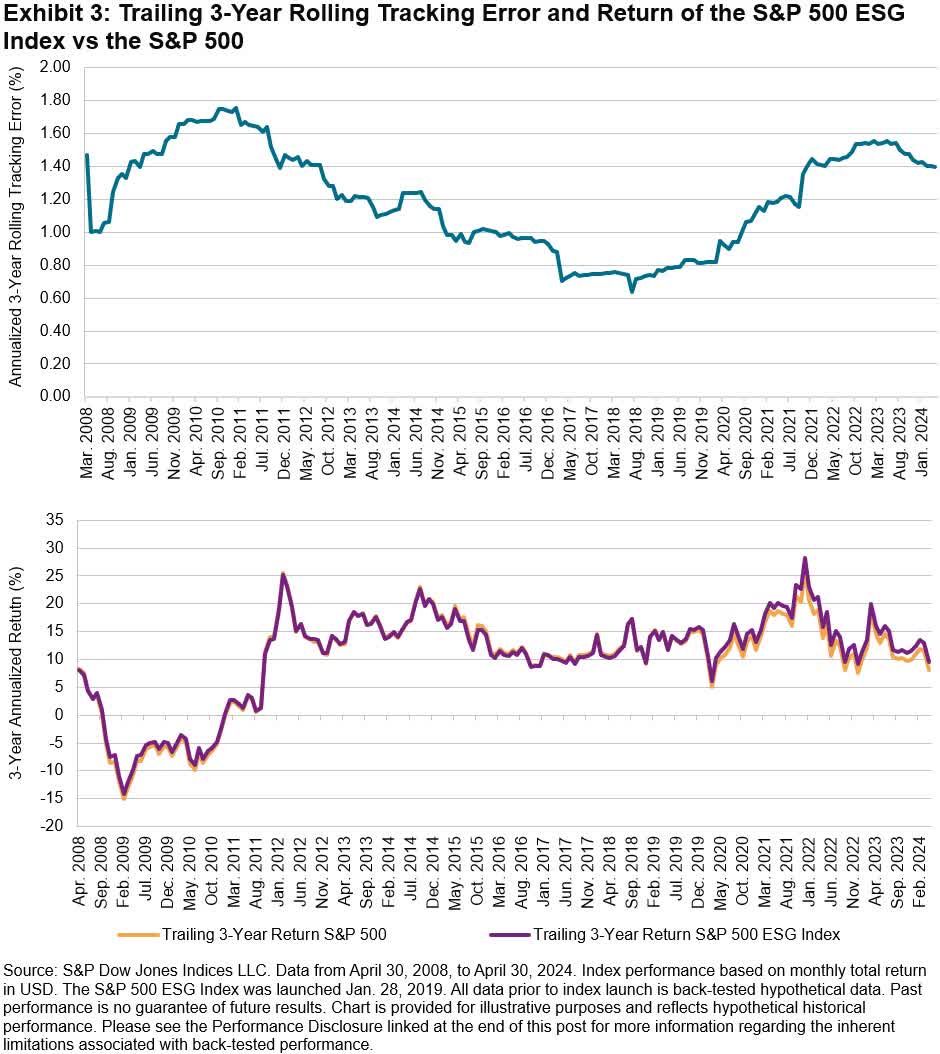

Tracking error measures the size of the index performance differential over a certain period. In other words, it is the annualized standard deviation of the difference between the performance of the S&P 500 ESG Index and the S&P 500 over a period. Tracking error is an important metric for market participants, as it can indicate whether they are obtaining the desired market exposure.

The S&P 500 ESG Index has historically achieved comparable performance to the S&P 500, thanks to its similar industry group weights. As of April 30, 2024, the annualized tracking error for the 3-year period was 1.399% (see Exhibit 2), demonstrating a relatively low deviation.

![]()

To review how this metric has evolved over time, Exhibit 3 shows that the 3-year tracking error of the S&P 500 ESG Index compared to the S&P 500 has consistently remained below 2%, indicating relatively low deviation.4

S&P Dow Jones Indices offers a range of indices that consider different levels of integration of ESG factors to reflect a wide range of investment needs. These include the S&P 500 ESG Leaders Index and the S&P 500 ESG Elite Index. Typically, the stricter the sustainability criteria are, the higher the expected tracking error.

![]()

Conclusion

The S&P 500 ESG Index’s construction maintains similar sector and industry weights as the benchmark, allowing the integration of ESG scores while maintaining similar sector exposures, which has resulted in a relatively low tracking error, even without using an optimizer.

1 For more information, please see the S&P ESG Index Series Methodology.

2 For more information, please see Rowton, Stephanie, “Sector Neutrality: An Essential Mechanism within the S&P 500 ESG Index,” S&P Dow Jones Indices LLC, Sept. 9, 2024.

3 Sector active share is a specific application of the broader concept of active share, which measures the degree to which a portfolio’s sector allocations differ from those of its benchmark. It is calculated by taking the sum of the absolute differences between the portfolio and the benchmark’s sector weights, then dividing by two.

4 Low tracking error is typically less than 1%. This indicates that the composition closely follows the benchmark with minimal deviation. Medium tracking error is typically between 1% and 5%. High tracking error is typically greater than 5%. These ranges can vary depending on the specific context and investment strategy.

Disclosure: Copyright © 2024 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. This material is reproduced with the prior written consent of S&P DJI. For more information on S&P DJI, please visit S&P Dow Jones Indices. For full terms of use and disclosures, please visit www.spdji.com/terms-of-use.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here

")

")

")