")

The following segment was excerpted from this fund letter.

Lagardère: only a minor possibility the business is properly valued

We have held a position in Lagardère (OTCPK:LGDDF) for over eight months after the shares fell away whilst Vivendi (OTCPK:VVVNF, OTCPK:VIVHY) waited for approval for its takeover offer. Vivendi already owned 27.6% of Lagardère and agreed to acquire Amber Capital’s 17.5% stake on 16 December 2021 and lodged takeover documentation on 21 February 2022. The takeover offer could not be finalised until Vivendi met two regulatory conditions, being to divest its Editis book publishing business and “Gala” magazine; these conditions were finally fulfilled in November 2023. As a result of the length of the offer, Vivendi closed the offer and granted accepting shareholders “transfer rights” to transfer their shares to Vivendi at the bid price of €24.10XD once the requisite conditions were met. In December 2023, it was agreed that the transfer rights would be extended to 15 June 2025, being a date by when Lagardère will announce its first full year results under Vivendi’s control. There was a maximum of 28m transfer rights outstanding and we believe around 23.5 million still exist, mainly under the control of Arnaud Lagardère (the Chair) and Bernard Arnault (see below)

The present shareholder structure, with Vivendi having acquired ~63% of Lagardère, Arnaud Lagardère holding 8%, Financière Agache (Bernard Arnault) 8% and Qatar Holding 11.5%. When excluding an employee share plan, there is only a 7% free float of this €3.1 billion market capitalisation company.

Lagardère has two different but desirable main businesses where there are very few pure-play exposures globally:

- general (as opposed to technical/legal) book publishing where it is the second largest global participant; and

- travel retail where the business is the second largest convenience retail operator within travel and the fourth largest duty free participant.

General book publishing is high return on capital but relatively slow growing and with occasional volatility; conversely, convenience travel retail is a stronger long-term growth story, but is currently experiencing an aggressive upswing as travel returns to normality – and growth – post COVID. There is NOW no logical fit between the two businesses (there certainly once was), and they are likely to find different homes once Vivendi splits into four constituent parts. Lagardère also has some minor press, entertainment management and radio interests, the most desirable of which – the venerable magazine Paris Match – was sold to OTCPK:LVMHF for €120 million in May 2024.

Lagardère is now inexorably linked to Vivendi, not only via the majority ownership but Vivendi’s provision of an initial ~€1.5 billion debt line, required as a result of Vivendi’s takeover triggering early debt repayments. These loans have been refinanced to the tune of ~€1.3 billion with external banks, and Vivendi making a €650 million loan available, which has assisted in new revolving credit facilities being granted to Lagardère3.

Whilst nothing is ever obvious within the confines of the Bolloré empire, it does seem clear that the prevailing structure is highly sub-optimal. Parts of Lagardère would be best taken into 100% ownership to enable the creation of the envisaged publishing and distribution arm of Vivendi; however, we sense no long-term desire for Bolloré to own travel retail; it doesn’t fit neatly – other than as an investment – within the envisaged “new” Vivendi. But the travel retail business is a highly desirable asset which in our view has significantly greater value than that attributed by the accounting expert4 (€2.2 billion) opining on the Vivendi acquisition or the independent expert5 (€2.04 billion). Moreover, the Bolloré group’s desires appear to be to retain book publishing, since it fits within their own personal landscape, but also has financial attributes the group have historically found attractive.

This makes the investment case for Lagardère very attractive: there is effectively a Vivendi “put” – a value below which the shares are unlikely to fall, but in our view significant upside as the travel retail business will find a new home, either as part of a separate spin; at worst retained within a listed, rerated Lagardère which is very much the downside case or far more likely, sold to a third party. Private equity and Middle Eastern sovereign wealth (or a combination) would be obvious buyers given their other interests (past and present) in the sector.

Why is it unlikely that Lagardère is appropriately valued?

There are eight overriding reasons for Lagardère shares to be mispriced:

- there is only a 7% free float (worth €220 million) significantly restricting non-passive institutional investors from building a position; there is some offset by the fact that excluding past management and Bolloré, the two remaining significant external investors are astute judges of value, within strong global businesses, and have not made any type of overture to sell into the Bolloré offer;

- An uncertain strategic role for Lagardère within the Vivendi separation initiative – does it stay as a listed entity and on what basis? None of the Vivendi communications are clear about the role of travel retail, whilst regarding book publishing as a key asset;

- Vivendi’s offer to extend the transfer rights to 15 June 2025 creating confusion for longer;

- Career risk: the shares have long been regarded as a “dog” and currently trade 67% below the levels of early 2006 and nearly 30% below end 2009 – why bother?;

- The ongoing role of Arnaud Lagardère, the son of the founder (below) who was banned from holding executive roles on 30 April 2024 as a result of an indictment against him relating to events in 2018 and 20196; Arnaud Lagardère resumed his posts as Chair and CEO on 28 June 2024 after the partial lifting of the management activities ban M. Lagardère has recently sold ~4.2 million shares to Vivendi to assist in the repayment of personal loans to Credit Agricole7 (OTCPK:CRARF) but has a checkered reputation (see “background” below);

- As we discuss below, there are very few publicly listed cohort companies in either of Lagardère’s key businesses – the major general publishers are either privately owned, recently acquired by private equity or are part of a wider media conglomerate. There are publicly listed pure publishers such as John Wiley (WLY) or Scolastic (SCHL) but they thrive in specialist, technical areas. There are cohorts in travel retail, but as we discuss, the space covers everything from pure duty free to pure food service;

- IFRS16, being the accountants’ revenge on securities analysts, by turning the simple – paying rent in cash – into the complex – discounted value calculations with discount rate unwinds is bad enough in many companies. In the travel retail industry it is nightmarish, with amounts paid to airports by the retail concession holders being a mixture of fixed rent (subject to IFRS 16), minimum guaranteed rent (subject to IFRS 16) plus expensed turnover related costs, and percentage of turnover which is not subject to IFRS 16 and just charged as an operating expense. Hence, the use of EBITDA is nonsensical since it includes only the variable rental component as a cost. Bluntly, how many analysts are going to make the effort to do comparative analysis with only a 7% free float?? This encourages us to use operating cash flow adjusted for lease payments as a guide to profitability, with due regard to capital expenditure.

- Extensive use of joint ventures and equity accounted/partly owned companies within travel retail; Lagardère has four 50/50 joint ventures, notably with AWPL in Australia and the Pacific, SNCF (French Railways) and Lyon Airport which have revenue of ~€760 million (100% basis) but modest disclosed profits. Even more meaningful are the equity accounted associates with ADP (Aeroports de Paris) where Lagardère has 44% of the company which operates 140 stores at CDG and Orly plus 50% of the company operating the convenience retail. As a guide, turnover was ~€914 million in CY2023.

Lagardère’s storied background

We don’t have time to write a book; to do justice to Lagardère’s history virtually demands it, with interwoven links with Bolloré and Arnault, a mini-history of French manufacturing, Formula 1 cars, aerospace- the antecedent of Airbus (OTCPK:EADSF) – and the current businesses. It’s when you examine “storied” – not always for the right reasons – conglomerates like these that you understand why there are numerous hidden treasure troves for the astute acquiror to pick over.

The book publishing business Hachette was founded by Louis Hachette in 1826 after the purchase of a Parisian bookstore, moving rapidly into book publishing. As long ago as 1900, Hachette launched bookstores on the Paris Metro, an early evolution of “travel retail”. Over the next 80 years, Hachette expanded overseas, created new publications – notably “Elle” – and remained owned by the Hachette family.

In 1981 Hachette was acquired by Daniel Filipacchi and Jean-Luc Lagardère; Lagardère was the CEO of Matra8, an aerospace, transportation and vehicle business which diversified into weapons systems and electrical equipment. Lagardère pursued a conglomerate strategy under the Matra name, despite being heavily focused around vehicles. The company entered Formula 1 in 1968 – for only one season – but provided the cars for Tyrell’s 1969 championship winning season driven by (Sir) Jackie Stewart9.

In 1992, the shareholdings in Hachette and Matra were pieced together under the banner of Matra Hachette, with “Lagardère”, the current entity, being the largest shareholder; Lagardère moved to full control in 1996. In 1999, the technology business was merged with Aérospatiale, then in July 2000 with CASA (Spanish aircraft) and Germany’s DASA aerospace to become EADS – the direct predecessor of the current Airbus.

The Lagardère “entity” had been created as an SCA10 en commandite par actions – French version of a partnership, with general (managing) partners (Lagardère himself) and limited partners (effectively shareholders); this gave Lagardère complete control with less than a 10% stake. The entity issue became more important when Jean-Luc Lagardère passed away in 2003; his only son, Arnaud Lagardère, became the Managing Partner of Lagardère SCA. Arnaud reversed the strategy of his father and sold off the manufacturing and aerospace interests and embarked on a strategy of investing in wider media (including a 20% stake in Canal+ at one stage) as well as sports and sports management.

In 2013, Lagardère sold its final stake in EADS (Airbus) – realising ~€2.3 billion for the sale of 61.5 million shares; these shares are now worth ~€7.9 billion11 suggesting the decision left nearly 180% of the current market value of the whole of Lagardère on the table from this single transaction.

Source: TIKR | Best Site for Stock Market Research & Investor Analysis

These decisions plus money losing investments in sports set the scene for an ongoing decade plus of share price stagnation. In 2016, event driven European investor, Amber Capital, became a shareholder, building to above a 16% stake by March 2020, establishing a website “strongerLagardère.com” and putting forward a slate of 8 new directors12 and 16 resolutions, at a time when the share price was below €10. Six months prior, Lagardère had filed suit for significant damages alleging its shares had fallen significantly due to Amber’s campaign.

By mid 2021, M. Lagardère had been backed into a tight corner by Amber Capital’s 20% stake but Vivendi’s building of a 29% stake in the group throughout 2020 and 2021; despite a capital injection from Bernard Arnault to his personal holding company, the attempt to effectively pit Vincent Bolloré against Bernard Arnault in pursuit of Lagardère could not eventuate13. The SCA structure was removed in June 2021 by shareholder agreement at a cost of ~€200 million (10 million shares to the general partner), and eventually Vivendi buying out Amber Capital (subject to takeover).

With the sale of “Paris Match” to LVMH, M. Arnault has achieved something tangible from the exercise. We now move to the final stage of development with the likely break-up of Lagardère to fit the Bolloré/Vivendi agenda. We content that is not priced into the shares.

What could Lagardère be worth?

We view the best approach to valuing Lagardère as a sum of the parts, with the knowledge that in a Vivendi-driven dismemberment, the book publishing business will be spun off, to be preserved by Bolloré’s amazing sense of history in a new company named Louis Hachette Group14. This may require Vivendi to sell off the travel retail business within Lagardère, perhaps deal with the radio assets and bid for the 37% minorities. That is an easier proposition if the minority shareholders can SEE the fungible value of travel retail – which they presently can’t – as well as reducing the size (after a capital return?) of the required bid by Vivendi to acquire the minority position. Whilst Financière Agache and M. Lagardère both own transfer rights, the knowledge that travel retail could be worth far more than previously, aside from M. Lagardère’s emotional attachments to the business suggest negotiations with each of the key parties are likely. Qatar Holdings haven’t shown their hand other than not to accept the €25.50 (cum dividend) or €24.10 (ex-dividend) offers.

Travel retail: likely worth more than “independent valuation report”; significant rebound in progress

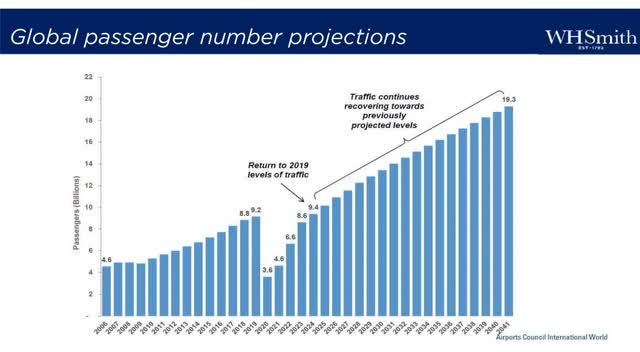

In our view, travel retail is an exciting business opportunity, which lends itself to sophisticated statistical analysis against a very simple equation: revenue = passengers x per pax spend. The more folks travelling, by ferry, cruise ship, train and plane, the greater the revenue opportunity. The key is to continue to unlock each passenger’s wallet which is where the analysis comes in. Most of our analysis is focused on airports since around 9.4 billion people use planes each year, with a positive demographic of younger people travelling more freely to more places using lower cost carriers and the various on-line methodologies to book and travel. Not forgetting demographically advantaged boomers…

Source: WH Smith plc Final Results presentation 9 November 2023

The sophisticated statistical analysis is all about trends, and how to maximise the selling potential of very expensive monopoly real estate within airports. Three of the listed companies – Avolta (OTCPK:DUFRY), WH Smith (OTCPK:WHTPF) and SSP Group (OTCPK:SSPPF) are (rightly) fanatical about formats, entry to new locations and the data analysis that underpins this. Somewhat stunningly, when we analyse Lagardère’s cohort and despite the complexity of the accounting, there is little differentiation between the pricing of the publicly listed companies or the underlying margins that they obtain.

In the two reports accompanying the bid documentation, we noted that travel retail was valued at a midpoint ~€2100 million by Sextant Expertise and 8 Advisory. We think things have moved on from there given the merger of Dufry with Autogrill to form the Swiss-based Avolta and the strong growth reported by the four major listed players in revenues in the immediate past.

We believe travel retail is a highly attractive business where consolidation of the industry on a global basis is leading to enhanced returns as passenger numbers grow rapidly as a rebound from COVID restrictions. Somewhat surprisingly, there are few publicly listed plays within an industry which investors would immediately recognise as being part of individually inherent monopolies, with significant pricing power – how often have you complained about the price of food, beverage or even a chocolate bar at an airport, anywhere on the planet?

We noted earlier that there are significant accounting issues in evaluating the cohort companies due to IFRS16; our focus is to look at segmental operating cash flow after lease payments which strips away most of the accounting issues, and to also be cognisant of capital expenditure which is a recurring contractual and expansionary item.

There are significant segmental differences within travel retail, with the business broadly dissecting into essentials (where Lagardère are the global leader in airports only), duty free and foodservice. Surprisingly, given that duty-free alone is a US$40bn+ global industry, there are few publicly listed peers within the industry. There is realistically only one direct comparative to Lagardère being Avolta (AVOL.SW) which has exposures to all the three main groupings, but there is merit in assessing three other listed entities:

Comparative sizes as at 30 June 2024

|

€billion† turnover |

shares |

Price (LOC) |

Eq. Cap (€mn) |

Debt (€mn) |

Ent value |

Outlets (#) |

Duty free |

Food |

Essentials |

|

Avolta |

150.4 |

€34.90 |

5,250 |

2,705 |

7,955 |

5100 |

4.90 |

4.64 |

4.09 |

|

Lagardère‡ |

Part of larger diverse group (analysis bellow) |

5120 |

2.19 |

1.56 |

2.02 |

||||

|

W H Smith† |

129.9 |

£11.32 |

1750 |

520 |

2,270 |

1270 |

1.74 |

||

|

SSP† |

796.0 |

£1.48 |

949 |

736 |

1,685 |

2900 |

4.10 |

||

|

China Tourism Duty Free† |

2068.9 |

K$47.9 |

11,619 |

(3,600) |

8,009 |

>200 |

5.56 + 2.81P |

||

|

DFS Group |

LVMH & Robert Miller; not separately disclosed |

420 |

4.00 |

||||||

|

Heinemann |

Privately owned – Heinemann family (Germany) |

500 |

3.60 |

||||||

|

Duty Free Americas |

Privately owned – Falic family (USA) |

200 |

1.94 |

||||||

| † £1=€1.19; €1=RMB7.95 €1=US$1.09 ‡ excludes joint ventures and associates |

Cohort valuations coalesce at historic EV/OCF of ~9x

The following tabulation assesses the four cohorts to Lagadere travel retail by examination of operating cash flow minus lease payments and comparison with capex over recent periods – trailing twelve months or estimates in the case of Avolta; it should be noted that the European companies are heavily seasonal with profits in the “summer” April – September period:

|

LOCmn |

Avolta (€mn) |

CTS Duty Free (RMB mn) |

SSP Group (£mn) |

W H Smith (£mn) |

|||||

|

CY2022 |

CY2023 |

CY2022 |

CY2023 |

year 9/23 |

TTM 3/24 |

year 9/22 |

year 9/23 |

TTM 2/24 |

|

|

Revenue |

6,878 |

12,790 |

54,296 |

67,075 |

3,009 |

3,209 |

1,400 |

1,793 |

1,862 |

|

OCF |

1,590 |

2,531 |

7,675 |

9,936 |

498 |

507 |

219 |

302 |

316 |

|

Leases |

(1,035) |

(1,883) |

(670) |

(711) |

(251) |

(258) |

(107) |

(137) |

(141) |

|

Net OCF† |

555 |

848 |

7,005 |

9,225 |

247 |

249 |

112 |

165 |

175 |

|

NET margin |

8.0% |

6.6% |

12.5% |

12.6% |

8.2% |

7.8% |

8.0% |

9.2% |

9.4% |

|

Capex |

(95) |

(396) |

(213) |

(746) |

(220) |

(251) |

(70) |

(106) |

(112) |

|

Free cash flow |

460 |

452 |

6,792 |

8,479 |

27 |

(2) |

42 |

59 |

63 |

|

Ent Value |

7,954 |

68,905 |

1,796 |

1,907 |

|||||

|

EV/Net OCF |

9.4x |

8.1x |

7.2x |

10.9x |

|||||

|

† before working capital changes |

There are various distortions to margins and multiples in the table above, notably:

- Avolta’s full acquisition of Autogrill did not close until July 2023, which results in significant revenue growth into CY24 and will see higher CY24 margins;

- SSP Group is in the midst of aggressive expansion of its food service outlets, which is constraining margin and adding to capex; the company has however, flagged midpoint revenue of £3.45bn for the year to September 2024;

- WH Smith still retains 514 “High Street” shops with £470m revenue & equivalent margin

Applying the cohort to value Lagardère Travel Retail at €3.35 billion

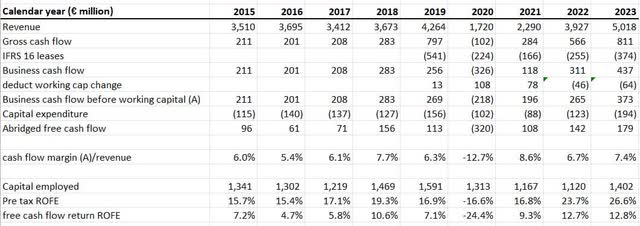

Relevant financials for Lagardère travel retail over a nine-year period are tabulated below:

We note, the significant recent growth in revenue which has attracted a stable, now slightly increasing margin and high return on funds employed despite >€100 million in capital expenditure each year. Margin out-turn is consistent with Avolta but marginally below WH Smith.

The outlook for 2024 appears very bright at this junction, although there are some mixed signals in respect of the upcoming Olympic Games which will cause clear distortions. Based on growth in H1 2024, with revenue in travel retail some 13.5% above Q1CY2023 like for like, but 18.0% on a reported basis including acquisitions, we expect full year divisional revenues to hit €5.8 billion, with increased cash flow margin around 7.8% – results consistent with WH Smith earlier this year. This suggests full year business cash flow around €450 million, just over 20% above that of 2023.

Lagardère’s main peer, Avolta will also record significant growth because of a full year of Autogrill; based on consensus analysists estimates, we expect revenues of €13.6 billion in CY2024, which at a 7% margin would yield business cash flow of €954 million for 2024.

On this basis, with a 30 June 2024 enterprise value of €7,954 million, Avolta trade at 8.3x forward business cash flow, not dissimilar to CTS Duty Free. Applying a similar multiple to Lagardère Travel Retail would provide a gross valuation of €3.7 billion – close to 70% above the highest of the independent valuations in the Vivendi takeover documentation. Even apply the cohort’s 9x business cash flow valuation to CY2023 numbers would yield a value around €3.35 billion for this unit.

Book publishing

Lagardère Publishing is, in our estimation, the world’s second largest general book publisher, with revenues of around €2.8 billion per annum, about 60% of the size of Penguin-Random House, owned by the German Bertelsmann Group. Book publishing is a relatively slow growth business – Lagardère revenues have grown 4.5% pa CAGR over the past five full years – but is a high cash flow, high return on capital business. In CY2023, the Lagardère business generated pre-tax, pre-interest cash flow of €229 million on revenue of €2.8 billion, and then invested €64 million for free cash generation of €165 million. With the intellectual property of publishing knowledge, past libraries and access to distribution – of all types – these assets are prized for their long term “investment” properties; corporate transactions in the sector (when they occur) tend to be at relatively high prices.

A brief comparison of the “Big 5” general book publishers is given below:

|

€million |

Owners |

2023 revs |

|

Penguin Random House |

Bertelsmann (family) |

4,532 |

|

Hachette & other units |

Lagardère |

2,809 |

|

Harper Collins |

News Corp |

1,830 |

|

MacMillan |

Holtzbrinck (family) |

est. 1,060 |

|

Simon & Schuster |

KKR |

est. 1,057 |

The US$12 billion in revenue carved up by the five majors has caused issues in respect of corporate transactions. The US Justice department successfully won a lawsuit (filed November 2021, deal terminated November 2022) to prevent Bertelsmann acquiring Simon and Shuster, when put up for sale by its previous owner, Paramount in November 2020. Bertelsmann had offered US$2.175 billion versus the 2021 EBITDA earnings base of $216 million, but Paramount was forced to accept an offer of (effectively) $1.62 billion by KKR, pitched at around 8.2x EV/EBITDA .

The regulatory intervention shows the potential future difficulty in dealing at the higher end of the publishing market; the stumbling block for the merger related to the alleged two-thirds market control of acquisition of publishing rights in the US, post a merger. Given Lagardère’s French (and non English) language publishing and its #4 size in the USA, there may be more flexibility regarding an eventual merger with another top 5 player.

In February 2022, US listed Houghton Mifflin Harcourt (HMHC) agreed to be acquired by Veritas Capital Fund VII at $21 per share being an equity capitalisation of $2,682. The company, a major supplier of school books under contract, held net cash of $146 million at end December 2021; the enterprise value of $2,535 million equated to 9.4x 2021 adjusted EBITDA of $270 million, being a 16.8% margin on revenue.

Valuations of book publishers and estimated value of Lagardère publishing

The passive trading multiples are below those applied in the last two corporate transactions in the sector, involving acquisitions of businesses with roughly $US$1 billion revenue bases. There are three listed “pure” book publishers of any significance; however, the two US based and listed entities have significant specialisms in technical and learning (J. Wiley and Sons) and €2.8 billion childrens’ books (Scholastic); the smaller UK listed Bloomsbury Publishing, famous for being publishers of the “Harry Potter” series:

|

Scholastic |

J. Wiley & Sons |

Bloomsbury Publishing |

|

|

SCHL (US$ million) |

WLY (US$ million) |

BMY (£ million) |

|

|

Contract education & children |

Technical, education & research |

General |

|

|

Shares issued |

28.21 |

54.4 |

81.44 |

|

Price (30/6/2024) |

$35.47 |

$40.70 |

6.26 |

|

Market capitalisation |

1,000 |

2214 |

510 |

|

Net debt/(cash) (ex-leases) |

(79) |

684 |

(66) |

|

Enterprise value |

921 |

2,898 |

444 |

|

Forward year revenue |

1,440 |

1,670 |

343 |

|

Forward year EBITDA |

170 |

395 |

50 |

|

Margin |

11.8% |

23.6% |

16.2% |

|

EV/EBITDA |

5.4x |

7.3x |

8.0x |

We view Lagardère Publishing as a significantly appealing business, with potential merger possibilities within the Big 5, most likely Simon and Schuster, once it is liberated under the Vivendi separation program. Comparisions of Lagardère’s performance to that of Bertelsmann and Harper Collins, suggest a higher end multiple could be attained on an IPO.

The Independent Accountant and Independent Expert in the Vivendi takeover documentation15 attributed (mid-point) values of €3.25 billion and €2.87 billion respectively, averaging out at €3.06 billion. Lagardère has performed better than Harper Collins over the past six years, but not quite as well as Penguin Random House (Bertelsmann) with the “Big 3” posting ~5%pa revenue CAGR over the period at average EBITDA margins of over 14.5%:

Source: Lagardère, News Corp & Bertelsmann annual reports

We are aware that an 8.2x EV/EBITDA multiple for the sale of Simon & Schuster was a distressed or pressured sale by the vendor. However, the use of the hefty premium Bertelsmann were prepared to pay is not appropriate. We believe in a passive valuation as part of the Vivendi separation, a multiple of 9x EV/EBITDA is reasonable, being above Bloomsbury but below the takeover of HMHC. On that basis, we view Lagardère Publishing as being worth €3.35 billion. It is noteworthy that return on invested capital in the division is over 23% pre-tax leaving open the opportunity for a private equity buyer to participate and leverage the business, in a similar fashion to KKR in Simon & Schuster should a full sale be contemplated. This isn’t a situation that we believe the Bolloré family would contemplate.

Other assets

The radio and entertainment assets, licences for “Elle”, “Journal du Dimanche” are largely incidental, especially after the sale of “Paris Match”. Most of these assets are in a SCA structure with M. Lagardère as the general partner, which gives a hint, in our opinion, that they will go with him once other sales from Lagardère are made.

We are happy to take the Independent Accountant (€308 million) and Independent Expert (€290 million) views of value and deduct the €120 million sale price of “Paris Match”, which was well above the estimates of either. That suggests the traditional media and entertainment assets to be worth ~€180 million.

Sum of the parts valuation: €32.40

Our sum of the parts valuation of €32.40 per Lagardère share is tabulated below:

|

€ million |

Comments |

|

|

Travel retail |

3,350 |

9x business cash flow as defined |

|

Book publishing |

3,350 |

9x EV/EBITDA per analysis above |

|

Other assets |

180 |

Independent experts less “Paris Match” sale |

|

Capitalised costs |

(126) |

9x central costs of €14 million |

|

Net debt |

(2,100) |

June 2024 = €2,255 but seasonal peak |

|

TOTAL |

4,564 |

|

|

Per share |

€32.40 |

30 June share price €20.70 represents 36% discount |

We have NOT applied a holding company discount since we view Lagardère as likely being dissected as part of the Vivendi separation which makes the significant passive valuation very appealing.

|

Copyright and Disclaimer © Other than material being the property of its respective owners, this presentation is copyright 2024 East 72 Management Pty Ltd. All Rights Reserved. You may not reproduce parts of this work without permission, which can be sought by email, but you are free to distribute the work on each security (Lagardère and Catapult International Limited) in its entirety with full attribution. This communication has been prepared by Andrew Brown and East 72 Management Pty Limited ( E72M) (ACN 663980541); E72M is Corporate Authorised Representative 001300340 of Westferry Operations Pty Limited (AFSL 302802) of which Andrew Brown is a Responsible Manager. While E72M believes the information contained in this communication is based on reliable information, no warranty is given as to its accuracy and persons relying on this information do so at their own risk. E72M and its related companies, their officers, employees, representatives and agents expressly advise that they shall not be liable in any way whatsoever for loss or damage, whether direct, indirect, consequential or otherwise arising out of or in connection with the contents of an/or any omissions from this report except where a liability is made non-excludable by legislation. Any projections contained in this communication are estimates only. Such projections are subject to market influences and contingent upon matters outside the control of E72M and therefore may not be realised in the future. This update is for general information purposes; it does not purport to provide recommendations or advice or opinions in relation to specific investments or securities. It has been prepared without taking account of any person’s objectives, financial situation or needs and because of that, any person should take relevant advice before acting on the commentary. The update is being supplied for information purposes only and not for any other purpose. The update and information contained in it do not constitute a prospectus and do not form part of any offer of, or invitation to apply for securities in any jurisdiction. The information contained in this update is current as at 30 June 2024 or such other dates which are stipulated herein. All statements are based on E72’s best information as at 30 June 2024. [ Please note that there have been significant share price moves of several “cohort” companies mentioned in this report during the month of July 2024]. This presentation may include officers and reflect their current views with respect to future events. These views are subject to various risks, uncertainties and assumptions which may or may not eventuate. E72M makes no representation nor gives any assurance that these statements will prove to be accurate as future circumstances or events may differ from those which have been anticipated by the Company. Footnotes 1Vivendi Press Releases: “Vivendi will study a project to split its activities into several entities” 13 December 2023, “Update on the study of the split project” 30 January 2024, “Update on the study of the split project” 22 July 2024 2Enterprise value being market capitalisation + net debt minus market value of securities (mainly Spotify) 3“Lagardère SA successfully completes its refinancing operation” Company announcement 7 June 2024 4“Note en response etablie par Lagardère” (French only) 12 April 2022 report by Sextant Expertise 5“Rapport de l’Expert Independent” (French only) 12 April 2022 report by 8 Advisory 6Further details in “Financial Times” 3 May 2024 “Lagardère: Anatomy of a French heir’s fall” 7“Financially suffocated, Arnaud Lagardère sells a quarter of his shares to Vincent Bolloré” “Le Figaro” 6 June 2024 8Stands for Mécanique Aviation Traction 9Fan’s of Netflix’s “Drive to Survive” should watch Roman Polanski’s brilliant documentary “Weekend of a Champion” made in 1972 about Jackie Stewart’s Monaco Grand Prix victory of 1971. 10Societe en commandite par actions 11As at 30 June 2024 price of €128 12Including ex-French President Nicolas Sarkozy 13A well written rundown of events contained in “Financial Times” 26 April 2021 “Arnaud Lagardère closes in on agreement to revamp governance” 14Vivendi “Update on the Group’s split project” 22 July 2024 15“Note en response etablie par Lagardère” (French only) 12 April 2022 report by Sextant Expertise and 8 Advisory |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here