")

")

")

Introduction

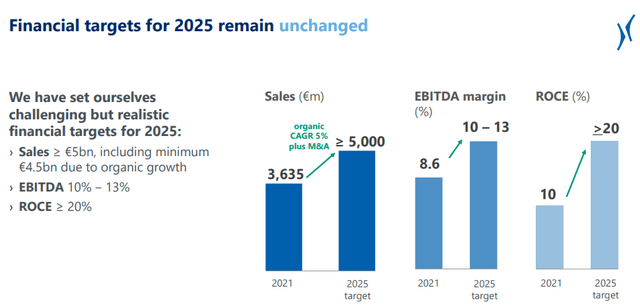

Krones (OTCPK:KRNNF) (OTCPK:KRNTY) is a German producer of machines used in the packaging and bottling sector. Its main specialty is to produce lines for filling aluminum beverage cans, glass bottles and plastic PET bottles. As you may know, I have been bullish on the packaging sector as a whole, and I think Krones stands to benefit from the slow but consistent demand increase in the packaging industry. The company’s mid-term plans include a higher revenue and a substantially higher EBITDA margin by 2025, and the company seems to be well on its way to achieve its targets.

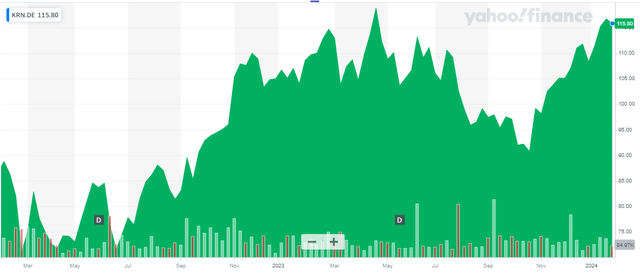

Yahoo Finance

The most liquid listing to trade in Krones’ stock is its primary listing on Deutsche Boerse where it is trading with KRN as its ticker symbol. The average daily volume in Germany is approximately 28,000 shares, for a monetary value of in excess of 3M EUR per day. There are currently 31.6M shares outstanding, resulting in a market capitalization of 3.67B EUR. As Krones had a net cash position of 285M EUR at the end of September, its enterprise value is just under 3.4B EUR.

Slowly moving toward its 2025 EBITDA margin goals

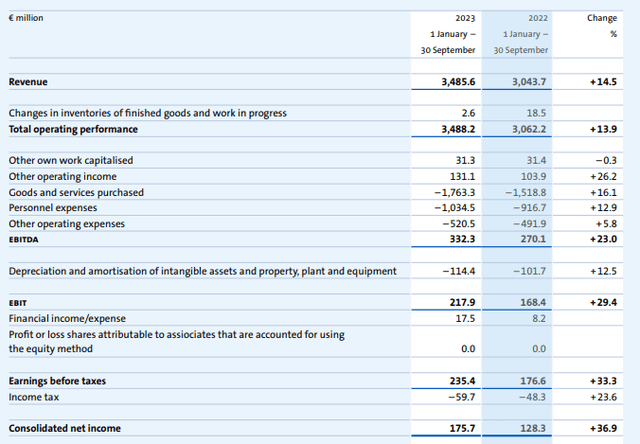

In the first nine months of 2023 (Krones still has to report its full-year results), the company generated a total revenue if 3.49B EUR, which is a 14.5% increase compared to the same period in 2022. Even more important than the revenue increase is the EBITDA increase, as Krones was able to boost its EBITDA by 23% to 332.3M EUR.

Krones Investor Relations

Meanwhile, the depreciation and amortization expenses increased by just 12.5% which indeed meant the EBIT expanded at a faster pace than the EBITDA, and with an EBIT result of 218M EUR in 9M 2023, Krones can be very happy. As the company has no debt, it’s actually reporting a positive interest income and this resulted in a pre-tax profit of 235M EUR and a net income of just under 176M EUR, representing an EPS of 5.56 EUR per share.

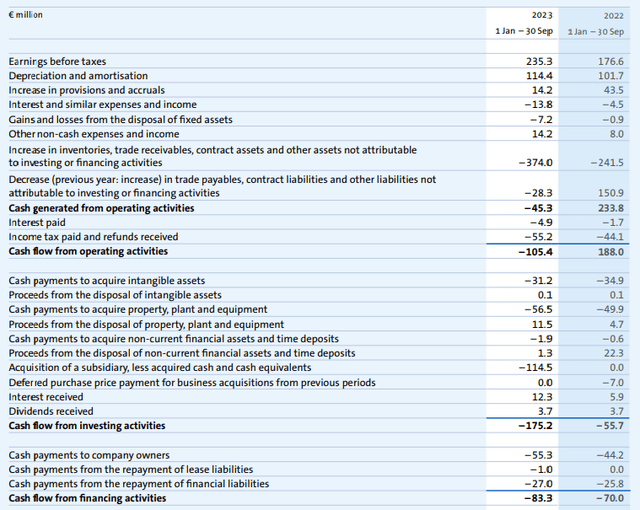

The EBITDA growth in the third quarter was a little bit more subdued, but it still handsomely exceeded the revenue increase. It’s also important to realize the strong net profit is also converted into real cash. Looking at the 9M 2023 cash flow statement, the operating cash flow was a negative 105M EUR, but this included a 402M EUR investment in the working capital position. Excluding working capital changes, the reported operating cash flow was approximately 297M EUR, and 293M EUR after deducting the correct amount of taxes.

Krones Investor Relations

We also should still deduct the 1M EUR in lease payments, but it’s only fair to add the 16M EUR in dividend and interest income back to the equation, resulting in an adjusted operating cash flow of 308M EUR In the first nine months of 2023.

With a total capex of 88M EUR, the underlying free cash flow in the first nine months of 2023 was roughly 220M EUR, or almost 7 EUR per share.

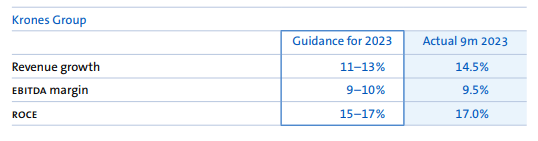

The company remains on track to post a 11-13% revenue growth versus 2022 while the EBITDA margin should come in between 9% and 10%.

Krones Investor Relations

That’s nice to see, but I’m more pleased to see the company remains on track to achieve the 2025 mid-term targets it outlined during its 2022 capital markets day. The company had initially set a revenue target of “in excess of 5B EUR” and I think that target will already be reached in 2024. As such, I will anticipate a revenue of 5.25B EUR by 2025.

Krones Investor Relations

The company plans to generate an EBITDA margin of 10%-13% on that revenue. If I would use the midpoint of that guidance and apply an EBITDA margin of 11.5%, the attributable EBITDA in 2025 should be approximately 604M EUR.

We know the depreciation and amortization expenses will be approximately 160M EUR, and I will assume a net finance income of 15M EUR per year (the net cash position will have increased by 2025, so I don’t think I’m too optimistic here). This will result in a pre-tax income of 460M EUR and a net profit of 340M EUR, assuming an average tax rate of 26%. This would indicate an EPS of around 11 EUR per share and I expect the free cash flow result to be pretty similar given the relatively low capex and growth capex plans. This also means that – barren of any sudden additional increases in working capital requirements – the net cash position will likely increase towards 700M EUR by the end of 2025.

Investment thesis

Based on the guidance for 2023, the stock is currently trading at an EV/EBITDA ratio of approximately 8, which is not spectacularly cheap. However, if I start running the models using the mid-term guidance, Krones is starting to look pretty cheap. The enterprise value will be just 2.9B EUR while the EBITDA is anticipated to increase to just over 600M EUR, indicating the stock is trading at a forward EV/EBITDA ratio of less than 5 based on the projections for 2025.

This, in combination with an anticipated P/E ratio of 10 and a free cash flow yield of approximately 10%, makes Krones pretty attractive at the current share price. I currently have no position in Krones, but I may initiate a long position in the near future.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")