")

")

")

Last year, I wrote about Kroger (NYSE:KR) and argued that it had an attractive valuation. I also liked its dividend growth record. Today, I’d only really support the latter argument. I hold the stock, and I plan to continue doing so. However, I’m not in a huge hurry to add more shares.

Kroger is a great company with a long history. It has stores throughout the United States, and it sells many products under its own label. It put out a bid to buy Albertsons (ACI) for $24.6 billion in October 2022. That move has been put into regulatory limbo, with the FTC expressing concern that the merger would stifle competition. Kroger and Albertsons have promised to sell some stores to C&S Wholesale Grocers to appease the regulators, but the merger has still not won approval.

Just today (August 20, 2024), Kroger announced it was filing suit to stop a Federal Trade Commission internal review of the merger. A recent Supreme Court decision that has called into question the powers of the regulative apparatus of the federal government. A pending case on August 26 might help the grocer’s merger go through in a more speedy fashion.

Recent Financials

Kroger has seen some strong revenue growth over the past decade. In the annual report released in 2015, KR had $108.5 billion in sales. That number was slightly north of $150 billion in the last annual report. The biggest growth took place between 2020 and 2023. This is not surprising, as inflation spiked in 2022. Revenue growth should be lower (without accounting for a future merger) because of the decline in the rate of inflation on a year-over-year basis. The future merger would lead to a higher top-line number because of a much higher number of stores, but same-store sales for the individual companies would need to be analyzed to see whether there was actual revenue growth if the merger goes through.

The most recent quarterly report saw revenue grow by only 0.5% over the same quarter last year, excluding fuel sales. The company expects full-year growth of between 0.25% and 1.75%. An adjusted EPS for the year is expected to come in between $4.30 and $4.50, which is higher than the $3.95 reported in the most recent fiscal year.

Net income over the past decade has generally fluctuated between the $1.7 billion and $2.2 billion range. There were a couple of outlier years in which income was slightly higher, with 2019’s $3.1 billion the high mark for net income. This shows that margins are relatively low, which is common for grocery companies, despite recent political complaints against price gouging on the part of companies that sell food. Kroger is a profitable company for a company that’s primarily tied to groceries, but its margins are not excessive by any objective standard.

Kroger’s net debt has increased over the past decade, from about $11.4 billion to $19.3 billion. This does not indicate huge leverage at this point. However, the larger Kroger would take on more debt that might be held by Albertsons should the merger go through, currently a little more than $13.8 billion. There is also likely to be quite a bit more debt tied to buying out the Albertsons shareholders.

The merger would theoretically produce some synergies and provide a stronger ability to negotiate lower wholesale prices. This could improve profitability.

Income

Kroger continues to provide an increasing income stream for investors. Just a decade ago, the company paid out only $0.35 per share each year. That has more than tripled to $1.32. Despite the uncertainty over the merger, the most recent dividend increase came in at 11%. Over the past five year, KR has increased its dividend by more than 15% per year on average. This is a healthy level of dividend growth. The current yield is not huge at 2.43%, but it beats the S&P 500’s (VOO) current yield that’s less than 1.3%.

One of the reasons the dividend has grown so rapidly is the very low payout ratio the company started with. This number was less than 20% back in 2015. It’s now nearly doubled to just north of 38%. This is still pretty low, and theoretically relatively safe, but it is a development to pay attention to. The fact that the dividend increased by 11% this year likely shows that the management believes that there are no major concerns that require keeping the growth number lower for a year or two.

Should Kroger continue increasing the dividend at an 11% clip, investors should see their income double in a little more than six years. This is higher than the rate of inflation, even at its recent peak of around 9%.

Current Valuation

When I wrote my previous article, the cost of a share of Kroger was around $44. Now, it sits at $52 per share, although it approached $58 earlier this year. I’m not angry at the price increase, as it has positively affected my net worth. However, I don’t look at the company as a screaming deal at present.

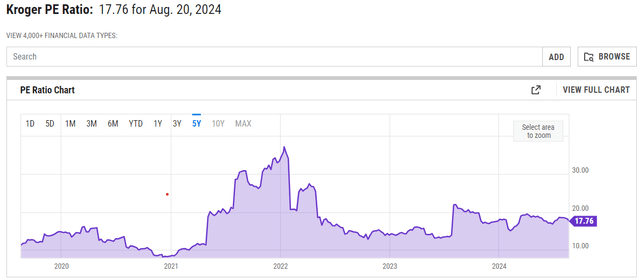

The current P/E ratio is 17.76, which is a little bit higher than its median number over the past five years of 15.42. Also, the uncertainty over the merger and calls for preventing price gouging in the grocery industry (which is actually relatively nonexistent) could pose threats to Kroger in the short run.

Kroger P/E Ratio Chart (YCharts)

Conclusion

Kroger is a great company. The company has had a strong run in recent years, and the grocery industry is relatively resistant to recessions. People have to eat, after all. KR has a higher price than it had a year ago, while there has not been a massive increase in revenue or income. There are likely to be better entry points in the future. I bought several years ago (around 2017, if memory serves correctly) after a revised earnings estimate. A massive drop in the short run provided a good entry point for the long run. Since I hold the stock, I’ll continue to hold for the solid dividend growth. The yield is not great, but the strong increases in the payout should provide more income over time. The merger with Albertsons and the current political environment are risk factors that investors should take into consideration in the short run, but overall, Kroger is a strong company with a strong history to draw from.

Read the full article here

")

")

")