(NTPIF)")

")

")

")

Q3 2024 Earnings Call Transcript")

")

Investment Thesis

The Interpublic Group (NYSE:IPG) reported Q4 results on the 8th, February and beat on revenue and EPS. The share price hasn’t moved much and trades on the 200-day moving average. I believe the company holds a narrow moat due to a suite of valuable intangible assets and the strong reputations of their advertising agencies. So I am initiating a Buy on the company with a share price target of $38.

Background

New York based IPG provides advertising and marketing services worldwide. They specialize in consumer advertising, digital marketing, public relations and other related disciplines. They are one of the Big Five alongside Dentsu, Omnicom, Publicis, and WPP. Like the rest of the Big Five their business model focuses on inorganic growth, whereby they acquire smaller advertising agencies and add them as subsidiaries. The company operates three segments, Media, Data & Engagement (46% of revenues), Integrated Advertising & Creativity Solutions (39% of revenues), and Specialized Communications (15%).

The company has transformed from a traditional marketing company to one that offers a full suite of solutions. In 2018 they acquired Acxiom for $2.3 billion and it remains a standalone unit of IPG. The acquisition brought together IPG’s marketing services, and analytical capabilities with Axciom’s expertise in data. The combination of both companies has been a success, with operating margins expanding 320 basis points since 2018 and 5-year CAGR of 6.28%.

Financials

IPG holds the fourth largest market share in the industry but sports some of the highest historic growth of the Big Five. Below is a table showing growth rates from the top four by market share in the industry:

| Name | 5-year CAGR | Fwd growth |

| (IPG) | 6.28% | 1.22% |

|

(WPP) |

2.62% | 2.43% |

| (OMC) | -0.79% | 4.30% |

| (OTCQX:PUBGY) | 8.27% | 4.15% |

The majority of the top four largest Advertising companies, excluding Omnicom are experiencing headwinds with forward growth rates that are below their historic rates of growth. IPG particularly lags the others, however, they posted organic growth recently and I believe this will continue. That leaves room for revision upgrades in future quarters and therefore more upside to its share price.

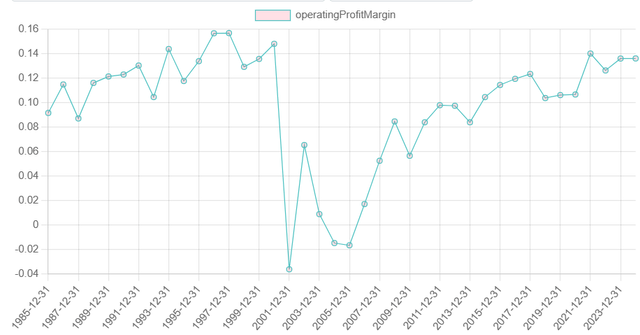

Operating Margins have climbed 520 basis points over the past decade and have accelerated further due to the “2020 Plan” and restructurings.

Source: Author’s Calculations

The company’s capital allocation strategy involves paying a robust dividend yield of 3.8%, making acquisitions and repurchasing shares. As of the 7th, February management announced the repurchase of $320 million shares. However, the main distribution is through dividends, as IPG on average repurchases about 2 cents of their shares back for every dollar of sales, which is less than Omnicom and WPP.

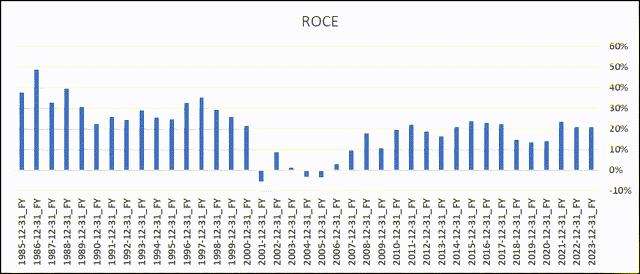

The company sports EBIT margins of 13.6% and is a business with low capital intensity, so its return on capital employed (including Goodwill) is greater than its cost of capital.

Source: Author’s Calculations

In Q4, net revenues climbed 1.6% to $2.6 billion, driven by organic growth, offset by the impact of dispositions. This was the first organic growth after three consecutive quarters of decline and was driven by growth across all segments of the business. Media, data and engagement grew 1.1%, Integrated advertising increased 2% driven by IPG Health, and finally, Specialized Comms grew revenue 2.9%. Operating Margins increased to 24.3% from 17.4% a year ago and after excluding restructuring charges, adjusted margins climbed 200 basis points.

Revisions

The 6-month trend in revisions is negative, however, over the last month analysts have moved up estimates across the board to 2028, due to the reported organic growth. EPS revisions show a similar trend, declining over the last 6-months but have been increased in the last month. The increase in revenue revision is a very positive sign and one of the main indicators for my Buy recommendation especially relative to the valuation.

Seeking Alpha

Valuation

Source: Author’s Calculation

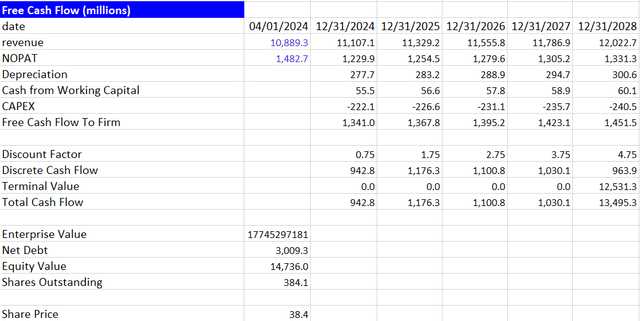

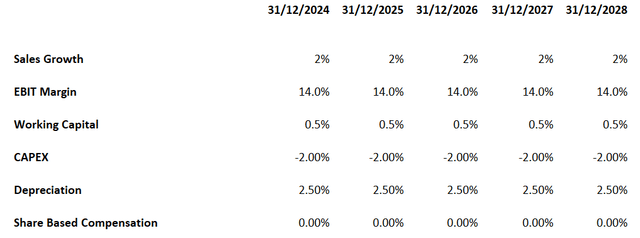

The average 5-year forward growth rate is 2% and the company pays a dividend of yield of 3.8%. So I have chosen to use a P/FCF multiple of 13x with a WACC of 9%, producing a share price target of $38 and an upside of 16%. In my valuation I have EBIT Margins constant at 14% but there might be room for further expansion as the “2020 Plan” continues. I have working capital incrementing cash flows at a rate of 0.5% of sales to account for the larger balance of accrued liabilities relative to accounts receivable. And for CAPEX I have this running into perpetuity at the 20-year median of 2%.

Source: Author’s Calculations

Risks

Advertising and Media spending is often closely related to the business cycle, and with more than 80% of IPG revenues generated in developed markets any downturn in those regions will drastically affect the top and bottom lines. Furthermore, despite the diverse range of clients, their client base remains concentrated, with a fifth of net revenues being accounted for by their top ten clients. So they must maintain good relationships and continue acquiring innovative firms or risk losing important clients.

On the flipside, in times of strong economic growth the firm can overpay to acquire firms leading to excessive goodwill and lower ROI.

Conclusion

IPG is a company with key competitive advantages, as evidenced by their return on capital and 5-year CAGR. It is currently trading on the 200-day moving average and I believe the fundamentals point to more upside. Especially as organic growth has returned and the trend in operating margins is up. So, as previously mentioned, I’m initiating a Buy on the company with a price target of $38.

Read the full article here

(NTPIF)")

")

")

")

Q3 2024 Earnings Call Transcript")