")

")

")

The S&P 500 rebounded for a second day in a row, as investors looked for more bargains in the technology sector, but the financial sector suffered losses after bank executives cautioned about the outlook for lending and net interest margins. At the same time, financial regulators announced that the expected increase in capital requirements for banks would be 9% next year instead of 19%. That is a huge tailwind for the sector, as it frees up more capital for banks to use for lending and trading. The caution from executives in the sector is understandable given the concerns about a slowing rate of economic growth, but I still see more tailwinds than headwinds as we move into the new year.

Finviz

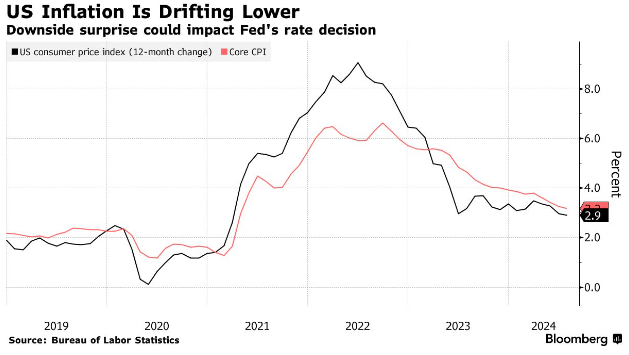

The Consumer Price Index (CPI) rose just 0.2% in August, while the core rate excluding food and energy rose 0.3%. That lowered the headline number from a peak of 9.1% to 2.5%, while the core rate held at 3.2%, as expected. Rental inflation remained elevated at 0.5% for the month, due to the lagging calculation used by the Bureau of Labor Statistics, and accounted for most of the headline number increase. As I have maintained for months, if the BLS used real-time data, the rate of inflation would already be at the Fed’s target of 2%. As the lagged calculation catches up with real-time price increases, the headline, and core will rapidly approach the Fed’s 2% target, if not fall below it.

Bloomberg

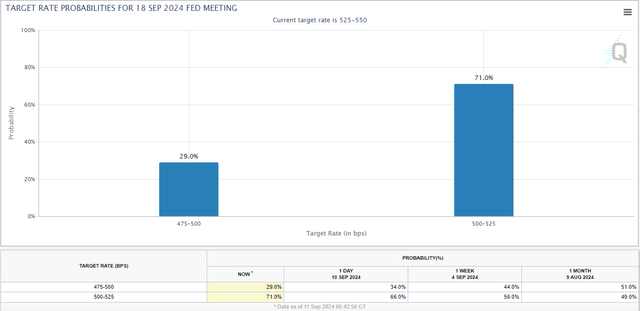

I think this report affirms we will see a 25-basis-point rate cut next week from the Fed. There is no reason to panic, which is what a 50-basis-point move would imply. Chairman Powell recognizes that the prior two occasions when the Fed was forced to make a larger initial cut (2001 and 2007) occurred in advance of an imminent economic downturn. Powell and the Fed will move rates at a measured pace on the way down, in the same manner they increased them. Such messaging from him during his press conference should calm investors.

CME

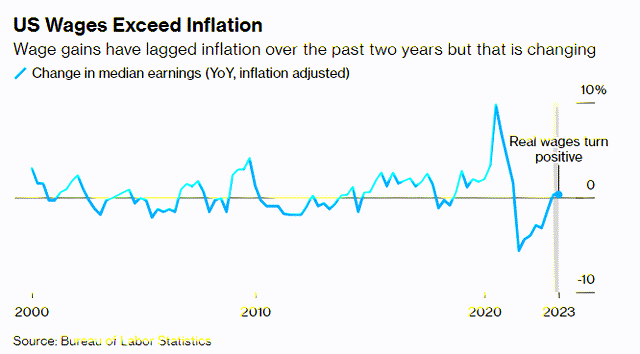

In April 2023, one of the pillars of my soft landing playbook was the return to real wage growth, which is the primary fuel for our economic growth. The disinflationary trend was well entrenched at that time, and once the rate of inflation fell below the rate wages were increasing, consumers started to gain purchasing power. Yesterday, the Census Bureau reported that median income increased an inflation-adjusted 4% in 2023 to $80,610. That is one of the most important reasons why the economy avoided an economic downturn, despite elevated borrowing costs.

Bloomberg

Real incomes continue to grow, as last week’s jobs report revealed average hourly earnings increased 3.8% in August on an annualized basis. In the Personal Income and Spending report for July, which includes all forms of income, wages grew 4.4% over the previous 12 months. In both cases, income growth exceeds both the CPI at 2.5% and the Personal Consumption Expenditures (PCE) price index at 2.5%. Additionally, the plunge in oil prices below $70/barrel for the first time since 2021 has huge ramifications for consumer spending power. Not only does it free up more discretionary dollars for purchases, but it allows central banks in the US and abroad to ease monetary policy more rapidly, lowering borrowing costs.

Barron’s

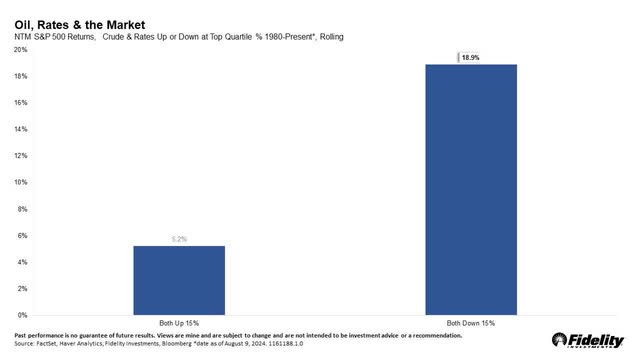

I shared the charts above and below last week, but they have renewed importance. The decline in both oil prices and interest rates over the past several months by more than 15% has a bullish precedent. Since 1980, a decline in both oil prices and interest rates of more than 15% over the prior 12 months has led to outsized gains for the S&P 500, as it is tremendously stimulative to economic growth.

Barron’s

Read the full article here

")

")

")

")