")

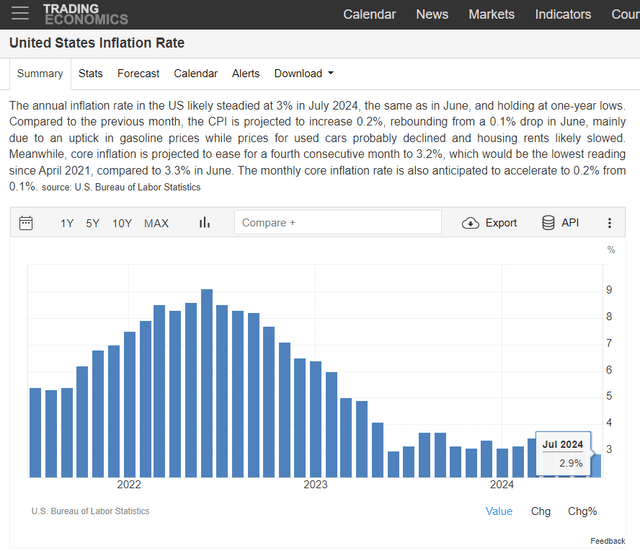

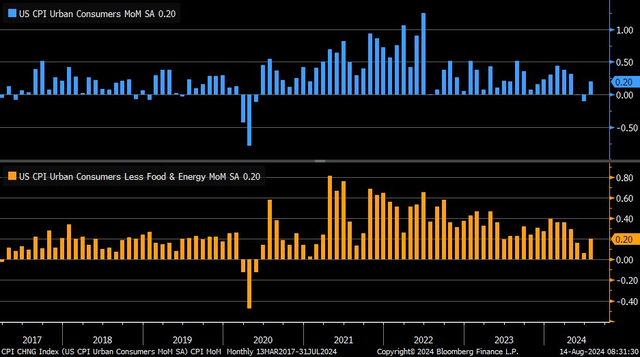

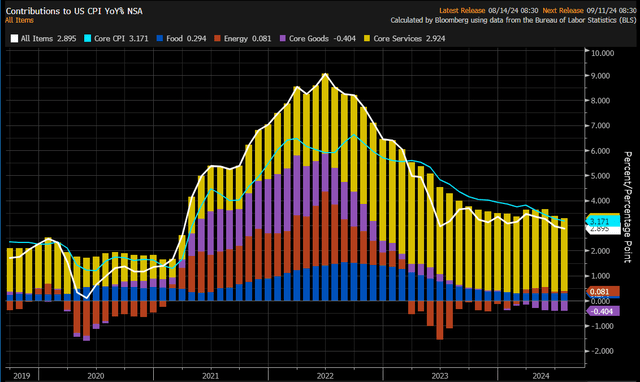

July CPI came in as expected at +0.2% on Headline following an unrevised up 0.1% in June. The Core rate also verified up 0.2%, in line with expectations. The year-on-year inflation rates are now +2.9% on Headline and +3.2% for the Core rate. It was the first drop under +3% since March 2021, indicating solid progress in the fight against high inflation. The Y/Y Core rate was the lowest since April 2021, matching what economists were forecasting.

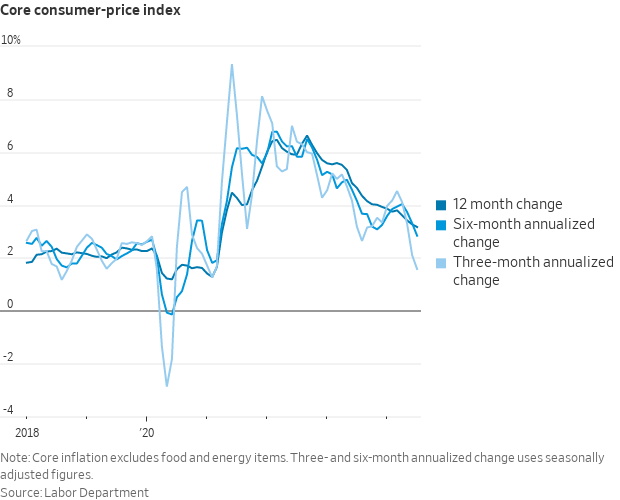

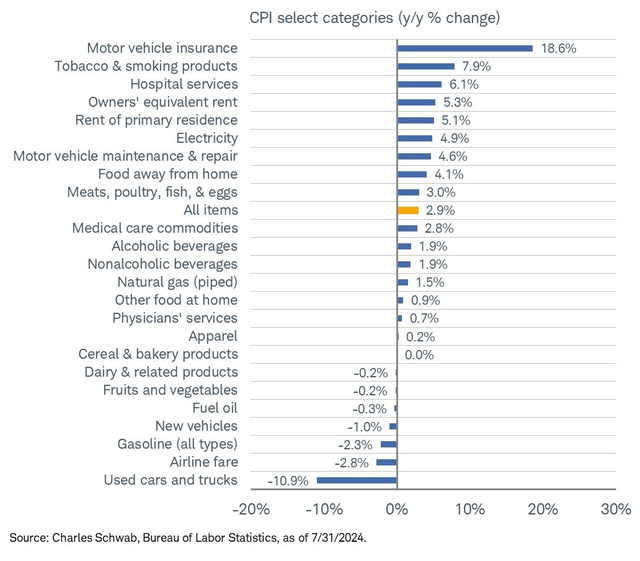

Unrounded, the numbers were even more dovish, with Headline CPI up 0.1549% and the Core change up 0.1652%. The 3-month annualized change in Core CPI fell to just +1.58% — the lowest since February 2021. As for other key metrics, US CPI Supercore M/M was up just 0.21%, a soft reading after the previous month’s negative change, and is now at the highest percentage in the past three months. Contributing to softer consumer prices is a steep 19.4% fall in used cars and trucks, though higher borrowing costs today make autos still expensive for many Americans.

US Real Average Hourly Earnings, as a result of the July inflation update, were up 0.7% and higher by just 0.4% on the Y/Y view. The Core CPI ex-Shelter index printed negative for the third straight month. Core Goods CPI, meanwhile, indicates ongoing deflation in that slice of the domestic economy, declining by 1.9% last month.

July CPI Verifies Near Estimates

Christian Fromhertz

CPI Y/Y Drops Under 3%

Trading Economics

CPI Headline & Core Post 0.2% Rises

Liz Ann Sonders

CPI 3-Month Annualized Change Falls Under 2%

WSJ

CPI Components

Michael McDonough

CPI Categories Y/Y

Liz Ann Sonders

Stock market futures dipped slightly immediately after the 8:30 a.m. ET release, but then crept higher, building on Tuesday’s big gain. Interest rates rose, though, with the yield on the US 10-year Treasury note (US10Y) increasing to 3.87% from 3.82%. The US Dollar Index was near a seven-month low this morning, with the EUR/USD pair trading at year-to-date highs near $1.10.

S&P 500 (SPY) Was Little Changed Post-CPI, Holding Tuesday’s Rally

Stockcharts.com

US 10-Year Treasury Yield Rose After the CPI Report

TradingView

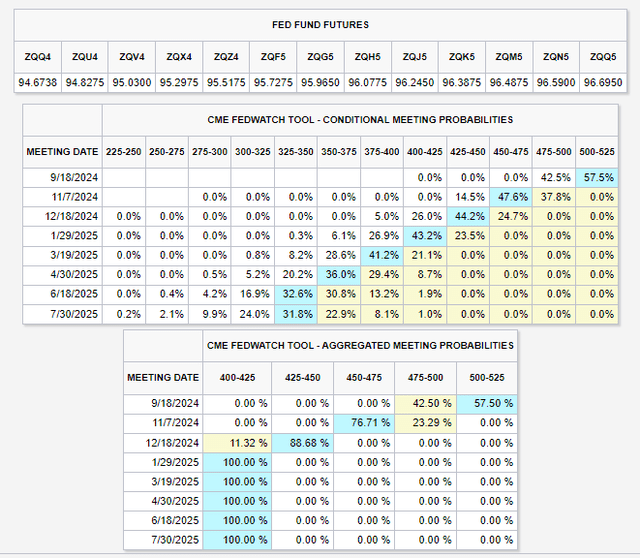

Bond traders trimmed their bets on a large 50-basis-point cut to come at the September Fed meeting. As it stands, there’s about a 58% chance of a normal quarter-point ease, as fears of an immediate economic slowdown have eased in the last several days. Recall last week that a sanguine ISM Services PMI report followed by an unexpected significant decline in weekly jobless claims helped assuage recession fears for the moment.

CME FedWatch: 58% Chance of a Quarter-Point September Ease

CME FedWatch Tool

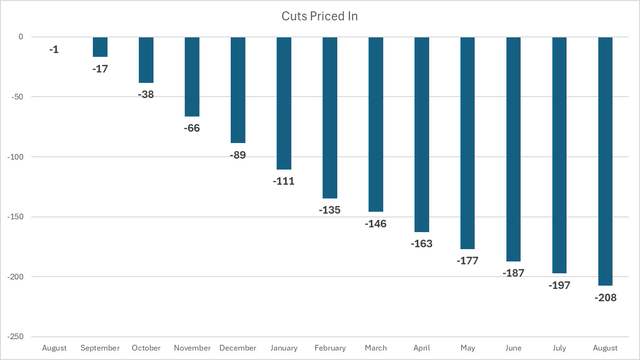

Expected Fed Rate Cuts

CME FedWatch Tool

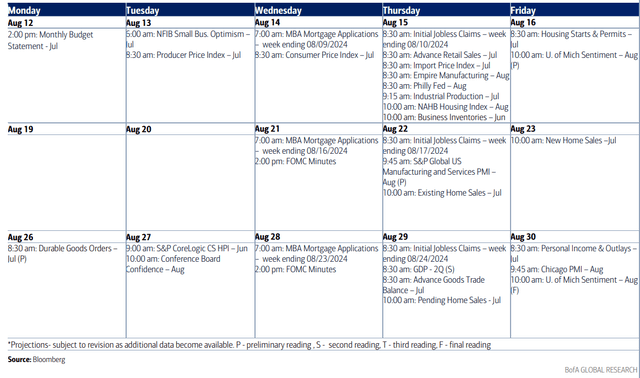

Looking ahead, Retail Sales and Industrial Production are the macro headliners on Thursday, while the University of Michigan Surveys of Consumers wraps up a busy data week. Tomorrow’s slate will provide clues about the growth segment of the US economy and will likely impact whether we get a 25 or 50 basis point Fed rate cut at its next meeting in September. And following an encouraging NY Fed Consumer Inflation Expectations report on Monday, the bar may be high for an improved set of household sentiment numbers in the UMich survey.

Next week is light, but we will get FOMC Minutes from the July Fed gathering and preliminary S&P Global PMI data, along with New Home Sales for July. Retail earnings continue to roll in, too.

Upcoming Macro Data

BofA Global Research

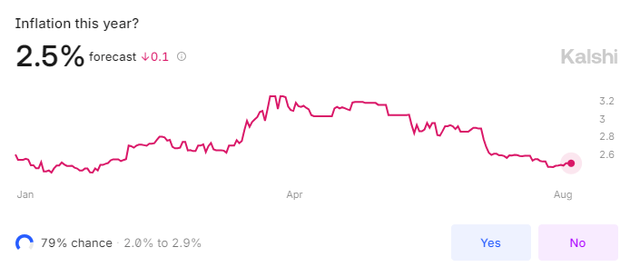

Inflation Seen Near 2.5% for 2024

Kalshi

The Bottom Line

The July CPI report was relatively soft when taking out the monthly consumer price changes out an extra decimal point. The year-on-year Headline CPI rate is now under 3%, which should come as welcome news to households and voting members on the FOMC. Equities weren’t much changed after the report, while Treasury yields ticked up. All eyes will now shift to tomorrow’s Retail Sales report and Friday’s University of Michigan survey.

Read the full article here

")