")

")

")

Investment action

I recommended a buy rating for Infineon Technologies AG (OTCQX:IFNNY) when I wrote about it last December, as I believed the underlying demand was robust and that the valuation should be well-supported by these demand tailwinds. Based on my current outlook and analysis, I continue to recommend a buy rating. My key update to my thesis is that I believe the tough part of this down cycle is over, and IFNNY should see growth over the coming quarters, backed by strong underlying secular trends. At the current share price, even with my revised model assumptions, the upside is still quite attractive.

Review

IFNNY reported 3Q24 earnings last week, which saw total revenue of EUR3.7 billion, gross profit of ~EUR1.5 billion, EBIT of EUR519 million, EBITDA of EUR989 million, and recurring EPS of EUR0.37. On a growth basis, revenue fell by ~9.5% in 3Q24, a slight improvement from the ~12% decline seen in 2Q24. Gross margin also improved from 38.6% in 2Q24 to 40.2% in 3Q24, although it is still down ~420 bps vs. 3Q24. The same trend was seen in EBIT, where the EBIT margin expanded 30 bps sequentially to 14% but is still down from 24.4% in 3Q24.

Certainly, results have not been great since I last wrote about IFNNY. Year-to-date [YTD] revenue is down ~9% vs. my expectation for 7% growth in FY24. YTD EBITDA margin also did poorer than I modeled (28.2% vs. my model of 35.1%). As such, I get why the share price has seen heavy pressure since the start of the year. However, I am not ready to throw in the towel as it appears that IFNNY has moved past the bottom of this cycle as 3Q24 marked the first quarter of positive sequential growth since the start of FY24, and management guided for sequential growth in all segments in 4Q24. Importantly, it was noted that the worst of the inventory correction is now in the rear mirror (per management comments). I am cognizant of the fact that 1 quarter of sequential growth (3Q24) and 1 quarter of positive guidance (4Q24) are not sufficient to prove that a turnaround trend is happening. However, I am confident that over the next few quarters, IFNNY will see a growth turnaround for three reasons:

IFNNY

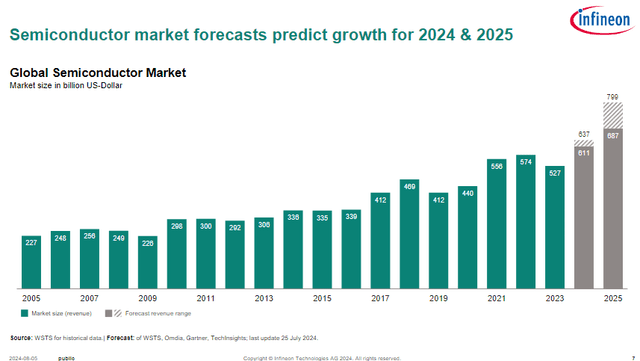

- The overall semiconductor market is expected to see growth in 2024 and 2025, which IFNNY will benefit from given its leading market position.

- OEMs are shifting from mature nodes (>28 nm) to more powerful nodes (<28 nm), an area where IFNNY is seeing very positive win rates (implying market share gains). This is a good quote from the 3Q24 earnings call to back this view: “I think we will see for the next years continuous market share gains because we are just now in the transition from the 65 to the 40-nanometer generation, which is now taking over in terms of volume and our design wind pipeline, confirmed design wins or rewarded design wins is even stronger in the 40-nanometer generation compared to 65. So, I think we are set up for more market share gains going on. And I also see a good design win trajectory already at this point in time playing out in the 28-nanometer node. So we are pretty confident on that business.”

- I believe everyone can agree that demand for AI-related solutions/applications is going to continue growing from here, and this is a very positive trend for IFNNY. This increases demand for advanced power solutions, where IFNNY is already seeing strong traction so far. In the call, management noted: “we are accelerating our AI power business with significant ramp-ups for several customers, some of which already deploy our innovative vertical power delivery solutions”

IFNNY

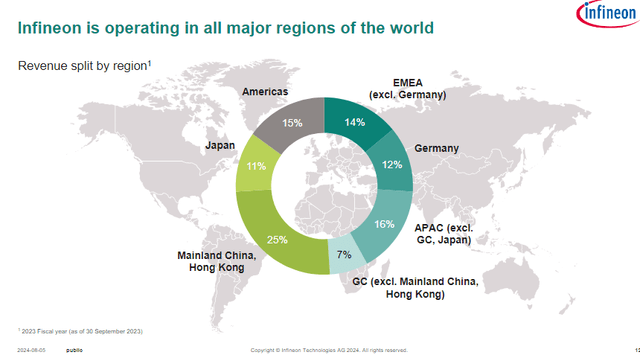

Given that automotive is IFNNY’s largest segment, I can understand why some investors may be worried about the weak EV demand environment in the US. This is a fair concern, but remember that China continues to see strong EV demand, and IFNNY has more revenue exposure to China than the US. Importantly, IFNNY is the leading player in China, which provides investors with exposure to the fastest-growing EV market in the world.

Looking at the global adoption of electric vehicles, regional divergence remains pronounced. China sees healthy consumer demand, which helps us, particularly given our number one automotive market position there. 2Q24 call

Hence, if you were to ask me, will IFNNY see growth recover in the next quarter? I think it’s going to be hard to answer. But will IFNNY see overall growth over the next few quarters? I believe the answer is yes. Assuming this assumption is right, I expect IFNNY to see very strong EBITDA growth as the topline recovers and the cost structure gets lowered. I have already discussed my views on revenue above, so I will focus on cost structure here. There are two aspects to take note of here. Firstly, IFNNY will see EUR800 million of lowered costs at the gross margin line as these underutilization charges go away in FY25 (when utilization recovers). Secondly, IFNNY will start to benefit from its current cost-cutting program in FY26. For those that are unaware, IFNNY launched its “Step Up” program in 2Q24 to target a leaner cost structure, and so far, things have progressed well with the business already winding down two backend facilities in Asia, writing down equipment in a facility in Regensburg, and now expecting to reduce headcount over the next few quarters.

Valuation

Author’s work

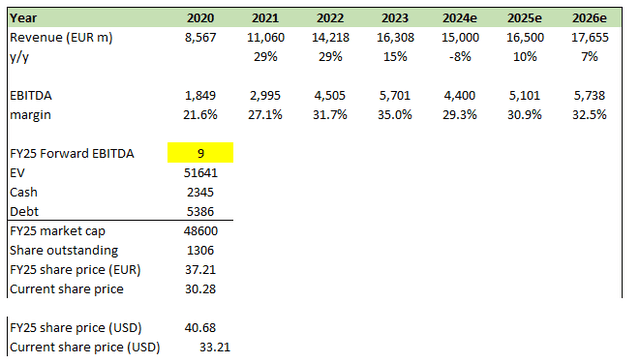

After the share price decline so far, I think the upside case remains attractive even after adjusting my growth estimates downward (reflecting the poor YTD performance and any lingering weakness for the rest of FY24). FY24 performance is likely to come as per guidance (-8%) given the visibility that management has and the YTD performance so far. In FY25, the business should see a strong growth recovery. As per historical performance, after a year of negative y/y growth, the following year’s growth tends to be >10%. Assuming 10% for FY25, I got to a revenue figure of $16.5 billion. As for FY26, I assumed 7% growth (pre-covid growth levels). I have also tapered down my EBITDA margin expectation as revenue size is smaller (but should still improve from FY24 given the larger revenue base vs. FY24 and cost savings).

Risk

IFNNY now needs to show the market that the trough is over and growth will turn positive over the coming quarters. This is basically a “show me” story now, which means if IFNNY fails to meet expectations or misses its own guidance again (it missed in 1Q24 and 3Q24), the stock will likely get punished again. In other words, pinpointing the exact timing of growth recovery is a risk that investors have to bear when going long the stock today.

Final thoughts

My recommendation is a buy for IFNNY. YTD, the business performance has been poor, with revenue declines and margin compression, but I believe IFNNY will see growth over the next few quarters. Firstly, the worst of the inventory correction appears to be behind us, and the company is demonstrating early signs of recovery. Furthermore, IFNNY has strong market positions in key growth areas that bode well for growth.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")