")

")

Agnico Eagle Mines Ltd. (NYSE:AEM) remains a favorite of gold bugs and gold hedgers, holding a unique combination of bullish logic. The valuation is fair, while its underlying mining properties and resources are some of the best in the industry. A significant “margin of safety” for investors is supported by lower-cost operations from locations mostly in Canada. In addition, the balance sheet and management team are quite strong. My view is if you want exposure to rising gold prices, you had better own this company directly, or through sector ETFs and mutual funds.

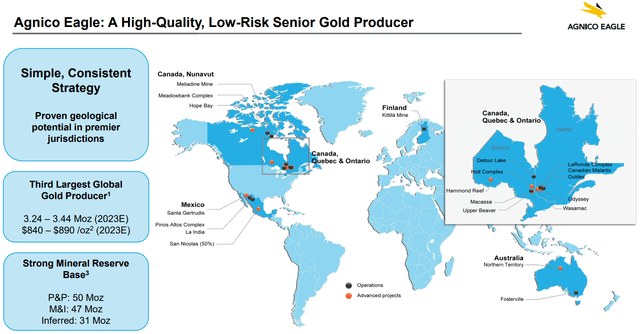

Agnico Eagle may run the smartest “map” of properties for investors. Canada, Australia, Mexico and Finland locations for gold in the ground may even represent a more effective setup than industry-leading production name Newmont (NEM), at least in terms of property safety considerations like ownership rights, taxes and regulations. I have taken the January 2024 Investor Presentation map slide to illustrate its constructive and diversified footprint of assets.

Agnico Eagle – January 2024 Investor Presentation

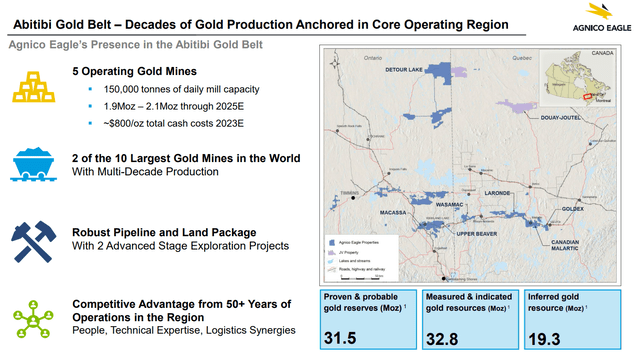

Canadian properties in the Abitibi Gold Belt are the company’s prized jewels for investors. Five operating mines, two of the largest gold mines in the world, and a number of exploration projects are included under the AEM umbrella.

Agnico Eagle – January 2024 Investor Presentation

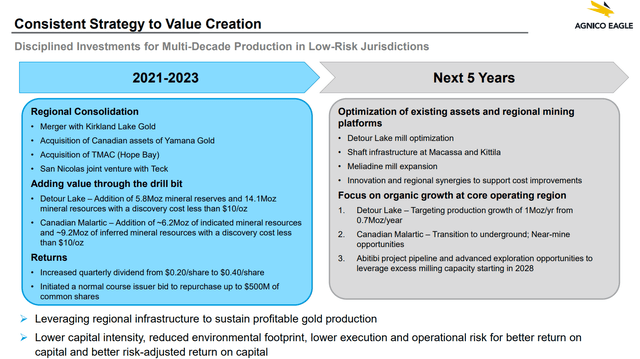

Resource Growth

Management is focused on growing sales without spending tons on capital to generate the increase. Below is a description of the recent merger with Kirkland Lake Gold, and mining conversion goals for the next five years. Moving from about 3.25 million ounces of gold produced in 2023, a target of 4 million is projected in coming years.

Agnico Eagle – January 2024 Investor Presentation

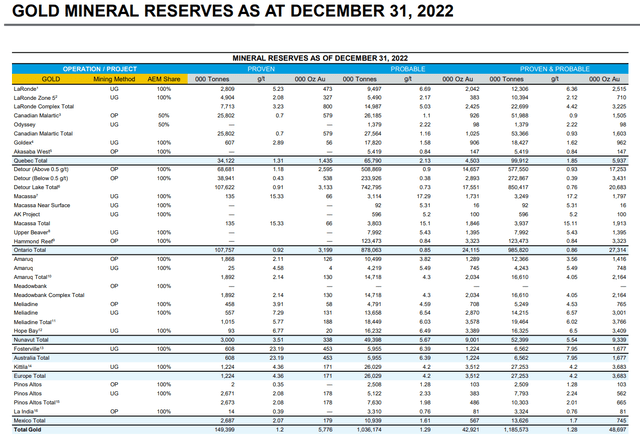

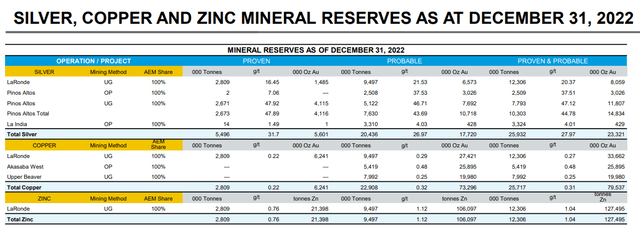

Looking at current and estimated production rates vs. proven & probable gold reserves of 48.7 million ounces (at yearend 2022) plus another 70.5 million in measured, indicated & inferred gold resources, I estimate the company should be able to produce at similar rates for another 15-20 years. This longevity number is likely only surpassed by Newmont and Barrick Gold (GOLD) in the major miner category (diversified with U.S. or Canadian properties).

Agnico Eagle – January 2024 Investor Presentation Agnico Eagle – January 2024 Investor Presentation

Production Costs

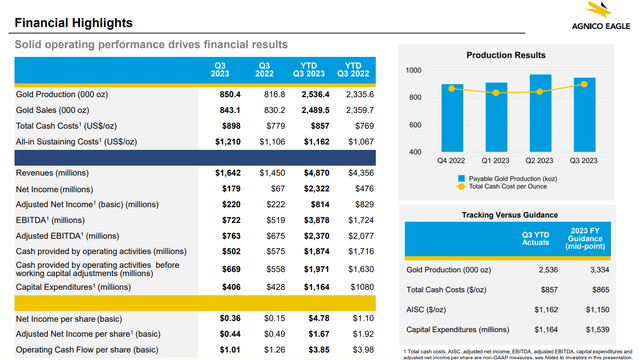

Another point to evaluate is the overall cost of metals production. Every mine and miner has a different cost setup, depending on locations, grades and recovery techniques, transportation to processing mills, on top of labor, energy, and debt service expenses. Fortunately for AEM shareholders, the $1,150 per ounce All-In-Sustaining-Cost number is very low vs. industry averages closer to $1,400 today. What this means is earnings and free cash flow rates per ounce are very desirable to own.

Agnico Eagle – January 2024 Investor Presentation

Clean Balance Sheet

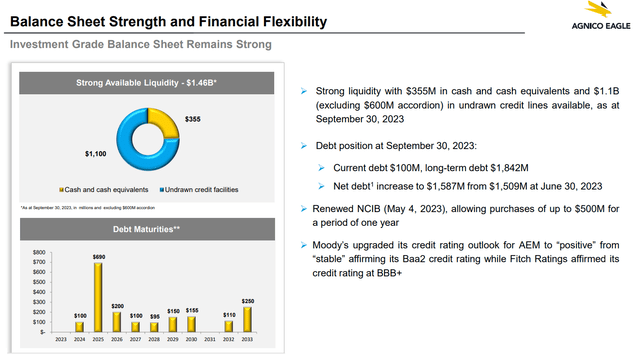

Agnico Eagle also runs a conservative balance sheet with little debt, which helps smooth out operating performance and keep costs of production as low as possible.

Agnico Eagle – January 2024 Investor Presentation

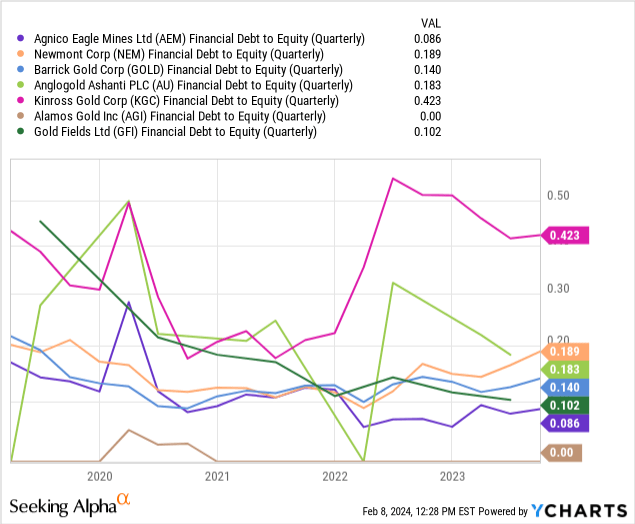

Measured against the largest gold mining peers traded in the U.S., Agnico Eagle runs one of the least leveraged balance sheets looking at total debt to equity. Compared to Newmont, Barrick, AngloGold Ashanti (AU), Kinross Gold (KGC), Alamos Gold (AGI), and Gold Fields (GFI), Agnico has excellent financial flexibility and very low overhead costs.

YCharts – Agnico Eagle vs. Largest Gold Miners, Debt to Equity, 5 Years

Valuation Ideas

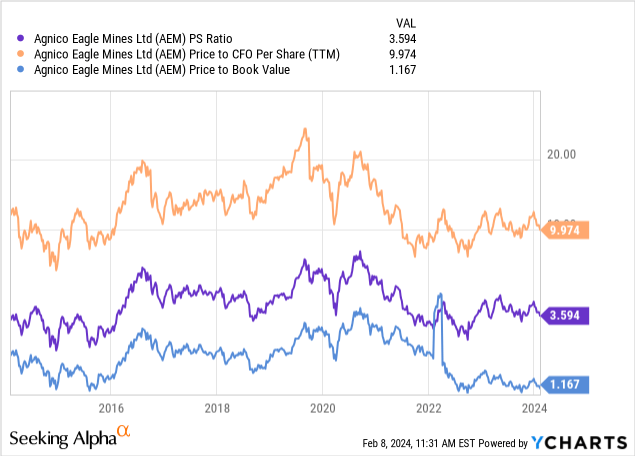

With a stock quote stuck in neutral the last few years, its valuation has been improving. Reviewing price to trailing sales, cash flow, and book value, AEM is approaching its cheapest valuation in years following a decade of company growth.

YCharts – Agnico Eagle, Price to Basic Trailing Fundamentals, 10 Years

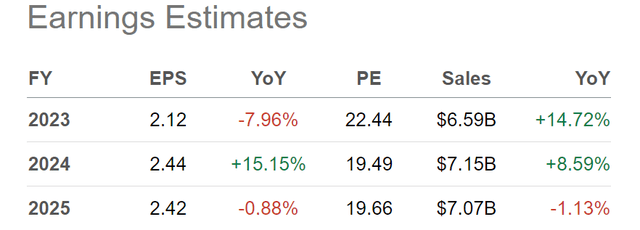

Earnings and sales are projected by analyst consensus to rise slightly in 2024, with flat results expected for 2025 vs. this upcoming year. The good news is Wall Street is forecasting flat to only minor price increases in the world’s main monetary metal. If gold prices surprise to the upside, EPS and sales have nowhere to go but up.

Seeking Alpha Table – Agnico Eagle, Analyst Consensus Estimates for 2023-25, Made February 7th, 2024

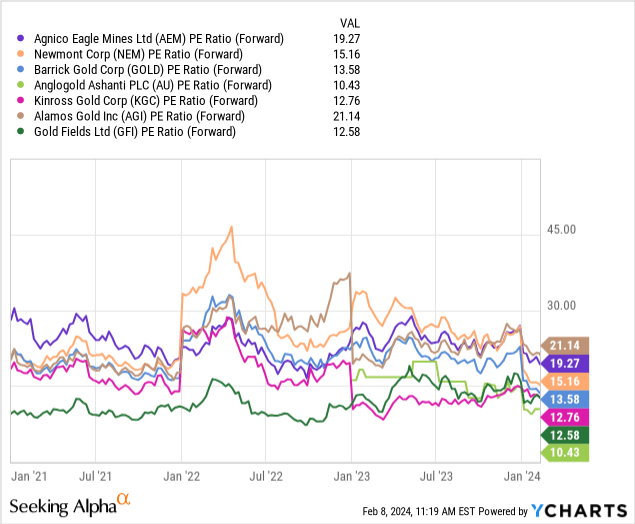

When we review price to forward EPS estimates since January 2021, we can see AEM has dropped from the most overpriced of the major miner group at 30x for a ratio, all the way down to 19x lately. While this multiple is still higher than the peer group, its “premium” has definitely shrunk.

YCharts – Agnico Eagle vs. Largest Gold Miners, Price to Forward Earnings Estimates, Since January 2021

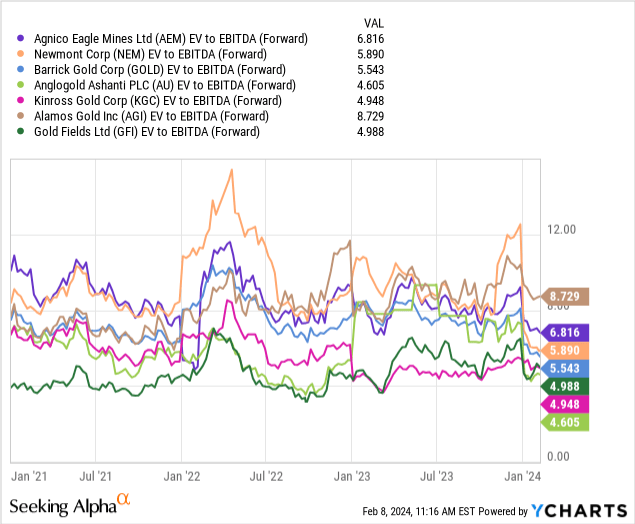

When we include debts due over time and subtract cash holdings at the bank from total equity market capitalization, the whole enterprise valuation [EV] picture has also been moving in the right direction for buyers. EV to forward EBITDA estimate ratios have dropped from 11x to 6.8x over the last two years.

YCharts – Agnico Eagle vs. Largest Gold Miners, EV to Forward EBITDA Estimates, Since January 2021

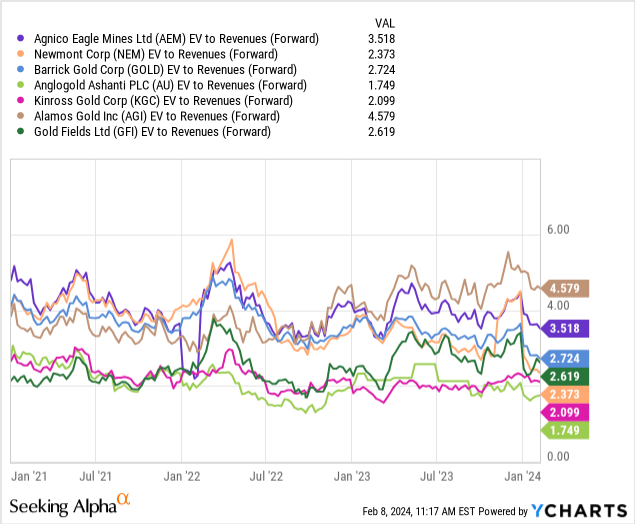

The EV to revenue ratio is now getting close to a decade-low reading. 24 months ago the ratio was 5x, today it is 3.5x.

YCharts – Agnico Eagle vs. Largest Gold Miners, EV to Forward Sales Estimates, Since January 2021

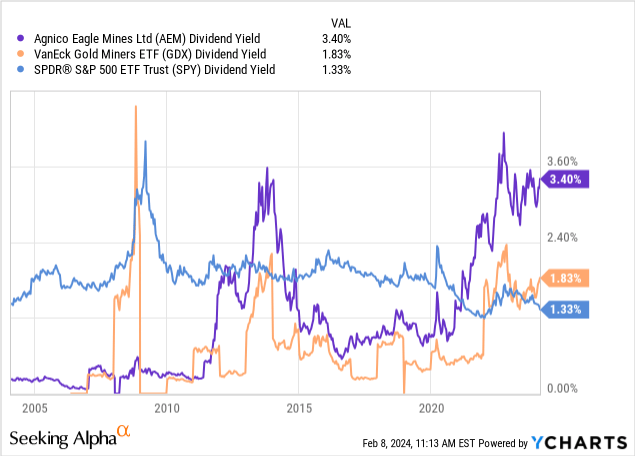

Dividend Yield Buy Argument

Perhaps the strongest argument to own Agnico Eagle at $47 is the trailing dividend yield of 3.4%. If gold, silver, zinc prices climb during 2024, earnings will jump and the annual cash distribution will almost surely bump higher into 2025. Already, the 3.4% rate is the best “relative” setup to both the VanEck Gold Miners ETF (GDX) average and S&P 500 level, pictured below. If you are a dividend/income investor searching for a long-term geopolitical and money printing hedge, AEM really should be near the top of your research list today.

YCharts – Agnico Eagle vs. GDX & SPY, Dividend Yields, 20 Years

Final Thoughts

Just remember, you get what you pay for in every miner, just like anything else in life. Agnico Eagle’s slightly elevated valuation vs. peers is well justified. The premium is a response to safer jurisdiction assets, an A+ management team, little net debt, low production costs, and a decent growth future.

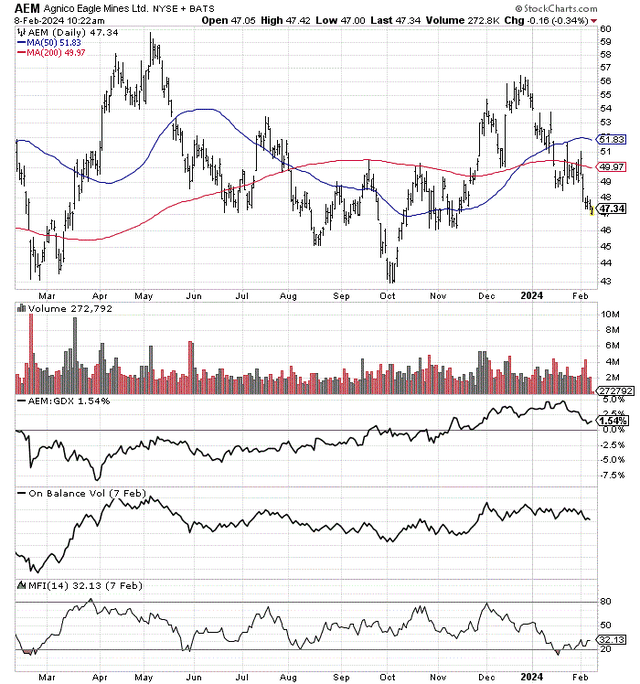

Despite going nowhere in price the last 12 months, AEM has been able to “outperform” the main gold mining industry VanEck Gold Miners ETF by a slim margin, with increasing relative strength since last March. You can view this statistic on the yearly chart of daily price and volume changes below.

In addition, On Balance Volume indicator trends have been above average vs. the mining sector, while the 14-day Money Flow Index has been flashing on oversold condition since the middle of January.

StockCharts.com – Agnico Eagle, 12 Months of Daily Price & Volume Changes

Share price targets depend on the future price of gold, alongside the rising costs of production, as the primary variables to consider. Of course, general Wall Street equity direction and the level of interest rates (creating acceptable returns for gold mining investments) are other ideas to ponder/follow.

The best-cash scenario for Agnico Eagle shareholders is inflation rates stabilize (cost of production inputs) and interest rates decline (allowing valuation multiples to expand), while the selling prices for gold, silver, zinc rise dramatically. In this case, operating profits and free cash flows would soar, as would the stock quote, on rerated acceptable returns on investment.

The flip side of the equation (bearish outcomes) would be high and rising levels of inflation and interest rates, with flat to lower metals pricing appear. In the end, you have to make a binary choice for your precious metals outlook.

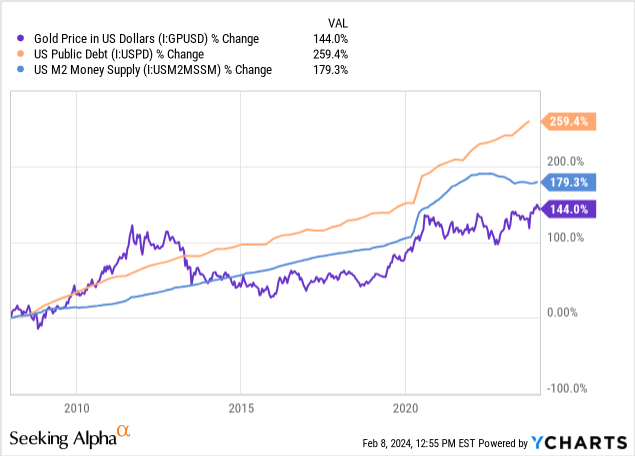

I have explained in many previous articles about the constructive lease rate picture for gold bullion, the higher than usual odds in 2024 of geopolitical trouble in the world causing flight-to-safety asset buying in gold assets, and the overall long-term valuation of gold being quite low today vs. other asset-classes and money printing levels in the U.S. over the decades.

For example, measured from the “beginning” of the last severe recession in 2008 (about the same spot in the economic cycle as today in my opinion), gold’s price increase has failed to keep up with out-of-control money printing rates in America.

YCharts – Gold Rate of Gain vs. Treasury Debt Outstanding & M2 Money Supply, Since 2008

My specific forecast is Agnico Eagle will trade above $100 a share over the next couple of years on a gold price rise above US$2500 to as high as $3000 an ounce in 2024 or 2025 (which would push EPS into the $5 to $7 annual range). So, adding a position now makes plenty of sense.

In a worst-case scenario of gold retracing back to $1800 an ounce this year, AEM could decline to new multi-year lows under $37. But I rate this outcome as a low-probability event (probably tied to a stock market crash generally on Wall Street).

For a balanced risk/reward review, a double in Agnico Eagle’s quote over three years would generate a total return around +30% annualized on new purchases (including the dividend). And, if gold gets moving to the upside soon, much better performance is possible for calendar 2024. On the downside, a worst-case decline to $35 a share represents about -20% for total return loss potential over the next 12 months.

When you eliminate all the noise in the financial media and investor negativity on precious metals in early 2024 (in favor of Big Tech names), AEM is sitting in a really good spot at $47 a share for a long-term valuation, with a solid/rising dividend yield rolling into your account while you wait for higher stock pricing. Based on its improved valuation over the last year, I am maintaining my Strong Buy rating. You can read my previous article on AEM posted in September 2022 here.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")

")