")

Icade (OTCPK:CDMGF) offers a very high-dividend yield and discounted valuation in the European real estate sector, but this seems to be justified by weak fundamentals and high exposure to the office segment in France, which faces cyclical and structural headwinds, thus Icade is a value trap in my opinion.

Company Overview

Icade is a French real estate company, operating as a commercial property investor and developer company. It’s a relatively small company in the European real estate sector, considering that its portfolio value was only about €6.6 billion at the end of last June, and its current market value is around $1.7 billion.

Its property portfolio is spread across 244 assets in France, and is highly concentrated in the office segment, which represented about 83% of its gross asset value (GAV) at the end of last June. Beyond office, Icade also has some exposure to light industrial assets (11% of total GAV), while other segments have smaller weights.

From a geographical perspective, its portfolio is quite concentrated in Paris, which accounts for some 89% of its portfolio, while other cities (including Lyon, Marseille, and others) only represent 11% of total GAV.

Investors should note that Icade had some significant exposure to healthcare, but has decided to gradually exit this segment. It has performed a significant sale in 2023, in which it received about €1.6 billion in cash, and still holds 22.5% of Praemia Healthcare and some assets in Italy, Germany, and Portugal, which it aims to sell over the next couple of years, expecting to raise about €1.3 billion in cash.

This means its property portfolio is expected to be mainly exposed to office in the future, which does not bode particularly well for its growth prospects, given that the office segment faces structural challenges. Indeed, following the pandemic, hybrid work solutions and work-from-home (WFH) have become increasingly popular, leading to much less demand for office space. While this trend is most visible in the U.S. and specifically in larger cities, this trend is also a reality in Europe even though office space in prime locations continues to show good demand levels.

More specifically in Paris, office demand in the Central Business District (CBD) remains quite healthy, but in other locations the supply-demand situation is quite different. As I’ve covered in a previous article on Icade’s competitor Gecina (OTCPK:GECFF), which is also quite concentrated in the Paris office market, being present in central locations and having quality assets is key to maintaining a resilient property portfolio.

While Gecina follows this strategy, being concentrated in Paris CBD and avoiding secondary locations, Icade follows a different strategy and is present across several office zones in the Paris region, being, therefore, more exposed than its competitor to structural issues in the office market.

As shown in the next graph, vacancy rates are quite different across Paris, with CBD enjoying a quite low vacancy rate (2.6% at the end of Q2 2024), while other areas have much higher vacancy rates that go up to more than 18% in the Inner Ring zone. Given that Icade is exposed to several areas in Paris, it’s not surprising that its vacancy rate was above 9% at the end of last June, a relatively high level compared to other European real estate companies and also compared to Gecina that has a vacancy rate of about 6%.

Office Vacancy (Icade)

While Icade says that more than 80% of its office portfolio is well located, its above-average vacancy rate shows that its portfolio quality is not great. Furthermore, even in well-located areas, the business prospects for office space aren’t particularly bullish over the long term, thus, in my opinion, Icade needs to reduce its exposure to the office and diversify its business profile more over the long haul.

The company seems to agree with this view given that its growth strategy is not based on the office segment, aiming to grow its exposure to light industrial properties, student housing, and data centers. This means its business profile is expected to gradually change over the long term, even though this is a slow process and office should remain its largest segment over the next few years.

In its property development segment, it has several projects underway which in total amount to some €1.3 billion of investments, being spread across offices, hotels, and data centers. At the end of last June, more than €900 million was already invested, thus its remaining capex needs are below €290 million.

Nevertheless, the majority of its developments are in the office segment due to historical reasons. Thus, new properties aren’t expected to change its business profile much in the short term. About 75% of its new developments are expected to be completed by the end of 2025 and most of them are already pre-let totally with a yield-on-cost of about 5%, boding well for rental income growth ahead.

In addition to its current investment pipeline, the company also owns some land, in which it intends to build hyperscale data centers which are expected to be completed over the next six to seven years and be operated by data center operators, such as Digital Realty Trust, Inc. (DLR) and Equinix, Inc. (EQIX) which are already Icade’s customers. Another way to further diversify its portfolio is through building transformations from office to residential, something that Icade is already doing in some assets in Lyon and Paris, which it expects to be completed by 2026 and can be retained in its property investment segment or sold to other investors.

Financial Overview

Regarding its financial performance, Icade has reported a mixed performance over the past few years given that its operating performance has remained relatively resilient, but its reported earnings were negatively impacted by property revaluations.

Like what happened to its peers, Icade’s property valuations were impacted quite significantly by rising interest rates over the past couple of years, plus higher vacancy rates in the office segment were also negative for its property portfolio value.

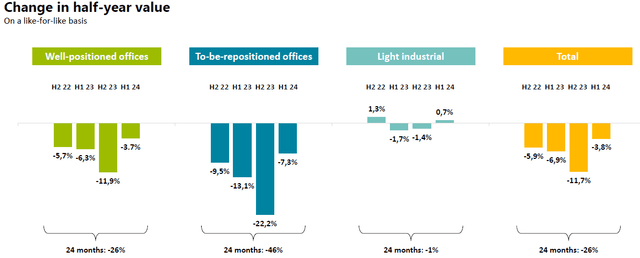

Indeed, its portfolio valuation has declined by 26% since the second half of 2022 until last June, with a higher impact on low-quality office properties, while industrial assets were more resilient and reported much more stable valuations during this period.

Portfolio decline (Icade)

As shown in the previous graph, its better-located offices declined in value by 26% over the past couple of years, while for lower quality offices the decline was 46%. This clearly shows that location and property quality are key for resilient valuations and relatively strong demand for office space, something that Icade seems to fail at to some extent, considering that it has reported an above-average portfolio valuation decline since mid-2022.

Despite that, recent valuations showed a trend deceleration for offices, as interest rates started to decline in Europe, which is support for property valuations in the short term. Indeed, the European Central Bank made its first rate cut back in June and is expected to perform several cuts over the next few months, which is expected to be a tailwind for property valuations ahead. According to Bloomberg data, the ECB’s key rate is expected to decline from its current level of 4.25% to 2.65% by the end of 2025, being a positive driver for higher property valuations in the coming quarters.

This is also positive for its balance sheet, as higher property valuations should lead to lower leverage in the near future. An important metric is the loan-to-value (LTV) ratio, which was 35.9% at the end of last June, representing an increase of about 240 basis points (bps) in the semester. This is justified by lower valuations and the lack of disposals over the past few months, but Icade’s LTV ratio is quite good and below the average of the European real estate sector. Thus, the company doesn’t need to perform further asset disposals in the coming quarters to protect its balance sheet, as lower rates should be enough for Icade to report a relatively stable LTV ratio going forward.

Regarding its operating trends, Icade’s gross rental income amounted to €188 million in the first half of 2024, an increase of 4.1% YoY on a like-for-like basis, driven mainly by rental indexation to inflation. However, regarding leases expired in the past six months, Icade has lost about €30 million of annual rental income through tenant exit and lower renewals, which does not bode well for rental income growth in the near future.

Its net current cash flow from strategic operations was €111 million in H1 2024, a stable value compared to the same period of last year, and its EPRA Net Asset Value (NAV) was €62.6 per share, representing an annual decline of 6.8% YoY due to lower property valuations and dividend outflows, which were not offset by its organic cash flow generation.

For the full year, Icade expects some business stabilization in H2 2024, but its net current cash flow is expected to decline by 5-10% YoY, showing that its operations continue to face several challenges, including higher vacancy, falling rents, and lower inflation uplift compared to previous quarters.

Despite that, Icade wants to maintain an attractive shareholder remuneration policy over the next few years, which is supported by its good financial position and cash proceeds from its healthcare disposal. Its last annual dividend was €4.84 per share, representing an annual increase of 11%, which was not supported by its earnings as the company reported losses in 2023.

However, this is largely explained by lower property valuations, which is a non-cash charge, thus the best way to analyze its dividend sustainability is based on cash flows. Its dividend outflow was €328 million in 2023, while its net current cash flow (including strategic activities and property development) was about €240 million. This means its dividend was not covered by organic cash flow generation and is, in some part, financed through asset disposals.

Considering that Icade has a good leverage position and a sizable asset disposal program related to its healthcare assets, I think its dividend is somewhat safe for now, even though its sustainability over the long term may be questionable.

The market seems to agree with this view given that at its current share price, Icade offers a dividend yield of about 24%. This high-dividend yield is clearly a sign that Icade’s dividend is not sustainable and a dividend cut is likely ahead. Indeed, according to analysts’ estimates, its dividend is expected to gradually decline over the next three years, to €3.17 per share by 2027. Thus, investors shouldn’t be too excited about Icade’s high-dividend yield given that is clearly not sustainable in the medium to long term.

Regarding its valuation, Icade is trading at a significant discount to its NAV, given that it’s currently trading at about 0.32x NAV. This multiple is below its own historical average over the past five years and also compared to its peers, including its closest peer Gecina that is trading at about 0.68x NAV, which in my opinion is more a reflection of Icade’s fundamental issues rather than being a signal of undervaluation

Conclusion

Icade offers a very high dividend yield and a cheap valuation, but I think this is more a trap than an opportunity for investors, as the company is highly exposed to offices and its business outlook is not great. While the company acknowledges this and wants to grow in other areas, this will certainly take time and Icade doesn’t seem to be an interesting play in the European real estate sector currently.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")