")

")

Introduction

Hims & Hers (NYSE:HIMS) — the viral telehealth platform that aims to help the world feel great through the power of better health — just reported Q2 earnings that obliterated all expectations.

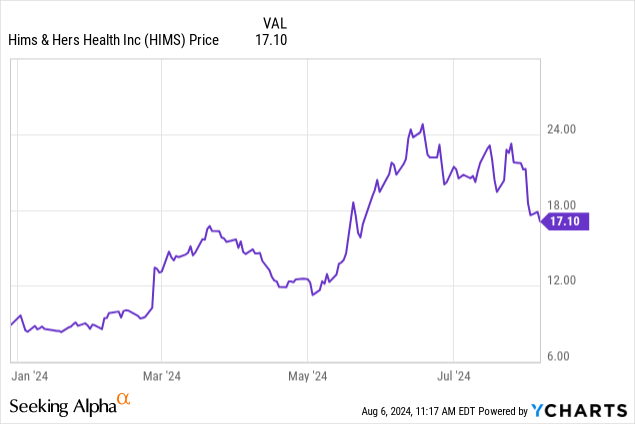

Throughout 2024, the stock has rallied as much as 200%, largely driven by the company’s tremendous growth and relentless execution. However, much of the rally was driven by the rising popularity and subsequent shortages of GLP-1 drugs — having recently launched its Weight Loss offering, Hims seemed poised to benefit immensely from this supply-demand imbalance. Unsurprisingly, the GLP-1 hype did provide some tailwinds for Hims, as reflected by the company’s blowout earnings.

That being said, Eli Lilly’s (LLY) CEO recently announced that the GLP-1 shortage is coming to an end, which was perceived as negative news for Hims… as if demand for Hims’ compounded GLP-1s might somehow disappear into thin air now that supply for branded GLP-1s is back online.

This news alone sent shares tumbling 12% in a single day. Along with a short report and a global market selloff, Hims stock is now down 30% from its recent highs.

To me, this flurry of negative news serves as a great dip-buying opportunity for investors.

Growth: Wild Reacceleration

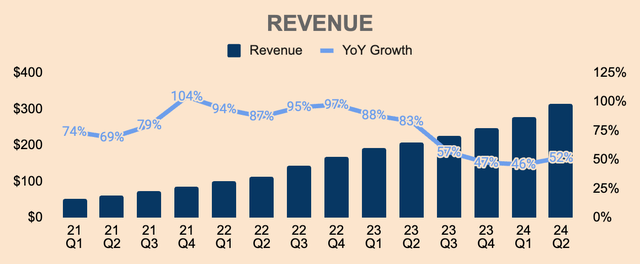

In Q2, Hims generated $316M of Revenue, up 52% YoY, which is an acceleration from Q1’s 46% growth. This also destroyed the high end of management’s guidance by $19M and analyst estimates by $13M. Such an outperformance reflects Hims’ strong value proposition and execution.

Author’s Analysis

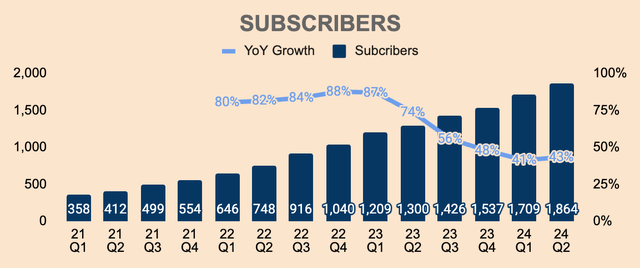

Revenue growth was mainly driven by a 43% YoY growth in the number of Subscribers, which came in at nearly 1.9M as of Q2. Hims added 155K Net New Subscribers in Q2, fueled by the growth of Personalised Subscribers, which was up 164% YoY to over 785K.

Author’s Analysis

Hims’ personalized offerings continue to drive the majority of growth as consumers seek medical care that caters to their unique individual needs, including multiple conditions, dosage levels, and form factors. Hims is seeing unprecedented demand and higher retention rates for personalized offerings, which is why the company is investing heavily in personalization.

For instance, Hims has increased Sexual Health personalized offerings by more than 70% over the past year, which contributed to Sexual Health Personalized Subscribers more than tripling YoY.

In the near future, Hims also plans to launch a multi-condition offering that targets both hair loss and erectile dysfunction — two of the company’s longest-tenured categories — for $49 a month, which should boost customer acquisition and retention.

Not to mention, robust Revenue and Subscriber growth was also driven by the recent launch of its Weight Loss offering:

- Its oral Weight Loss solution alone has reached an annual Revenue run-rate of $100M and is now the fastest-growing specialty to achieve that scale.

- Excluding its new GLP-1 injections, Hims’ existing offerings produced “Revenue north of $300M”, up more than 46% YoY. In other words, Hims’ GLP-1 compound generated around $15M of Revenue in Q2. Mind you, Hims launched its GLP-1 offering on the 20th of May, which means that this new product was able to generate roughly $15M of Revenue in less than half a quarter!

In short, Hims’ Weight Loss offerings are growing like wildfire and this should boost Revenue growth in the foreseeable future. In fact, management expects a further acceleration of growth moving forward:

- Q3 Revenue is estimated to grow 68% YoY to $380M at the high end.

- FY2024 Revenue has been revised upwards to $1.4B at the high end, up 61% YoY. This is more than $100M above analyst expectations.

- This also means that Q4 Revenue is expected to be about $426M, up 73% YoY.

Absolutely wild with how the numbers are stacking up.

Moreover, this is just the beginning of Hims’ Weight Loss journey. With more than 100M individuals with weight-related problems in the US, its Weight Loss product should be in high demand for the foreseeable future — with or without branded GLP-1 shortages — which should translate to robust Revenue growth for years to come.

Besides, buying Hims’ oral compound and GLP-1 injectables at just $79/month and $199/month, respectively, are much more compelling than spending $1,000+/month for an Ozempic or a Wegovy. And Hims’s Weight Loss products are delivering concrete results, so it’s reasonable to assume that Hims will continue to take market share from incumbents like Eli Lilly and Novo Nordisk.

Based upon self-reported data from approximately 12,000 customers subscribed a holistic Hims & Hers Weight Loss offering, customers report having lost on average 10.2 pounds while on compounded GLP-1 injections and 6.3 pounds, while on compounded oral medication kits between their initial weight loss consultation and their first check in approximately four weeks later.

(CEO Andrew Dudum — Hims & Hers FY2024 Q2 Earnings Call)

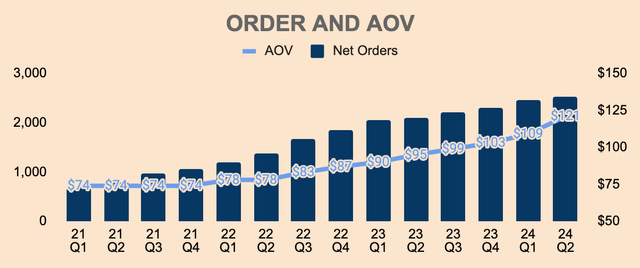

Over time, Net Orders and Average Order Values should climb up as well.

- Q2 Net Orders were 2.5M, up 20% YoY.

- Q2 AOV was $121, up 27% YoY and an all-time high for the company.

Author’s Analysis

Furthermore, Hims has many more categories to expand to, including insomnia, testosterone, menopause, and so on, so the growth potential for Hims is still massive.

And with a robust innovation pipeline in the field of personalization, multi-condition medication, and automation, I believe Hims has so much more room to grow from here.

HIMS FY2024 Q2 Shareholder Letter

Profitability: Durable Profitable Growth

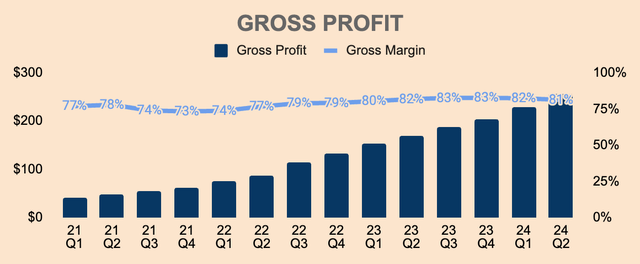

Turning to profitability, Gross Profit was $257M in Q2, representing an 81% Gross Margin, which declined 1pp YoY and QoQ, due to the launch of its Weight Loss offerings, which are still in the early stages of their life cycles. Moving forward, we should see further margin degradation in the near term but it should revert over time as the category scales.

Our Weight Loss specialty will continue to evolve throughout the year to leverage both our technology and personalized lines capabilities. As this happens, we expect rapid growth across the entire portfolio of offerings within the specialty. Utilization of third parties and other dynamics are expected to result in near-term Gross Margin erosion of 3 to 4 points that we expect to revert over the midterm.

(CFO Yemi Okupe — Hims & Hers FY2024 Q2 Earnings Call)

Author’s Analysis

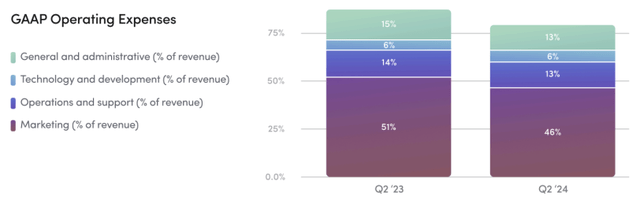

Hims continues to gain operating leverage. As you can see, all expense lines as a % of Revenue are either flat or down YoY, but the most important area of optimization came in the marketing department, with Marketing Expenses as a % of Revenue down 5pp YoY to 46%.

This shows that the Hims brand is getting stronger and gaining more awareness, which helps to drive “continued robust growth across our longest tenured specialties” and “meaningful acceleration in our ability to scale newer specialties”.

HIMS FY2024 Q2 Shareholder Letter

As a result of strong operating leverage, Hims’ bottom lines improved meaningfully:

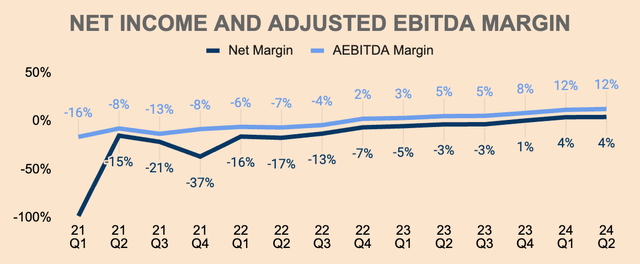

- Q2 Net Income was $13M at a 4% Margin, which improved 7pp YoY.

- Q2 Adjusted EBITDA was $39M at a 12% Margin, which improved 7pp YoY.

Author’s Analysis

The only plausible reason why bottom line margins did not improve QoQ is due to the higher costs associated with its Weight Loss offering, which should revert as it scales further.

That said, management expects Q3 and FY2024 Adjusted EBITDA of $40M and $155M, respectively, at the high end, representing an 11% Margin for both periods. This means that Adjusted EBITDA Margins are unlikely to improve during the remainder of the year, probably due to continued investments into the business as well as higher marketing spend in the back half of the year as Hims capitalizes on the Weight Loss opportunity.

Nevertheless, Hims is larger and more profitable than ever before and is on track to reach its long-term Adjusted EBITDA Margin target of at least 20% before 2030. Considering its current momentum, I think Hims will achieve this goal by the end of 2025.

Whatever it is, Hims is well-positioned to deliver durable profitable growth for years to come.

Health: Reinvesting For The Future

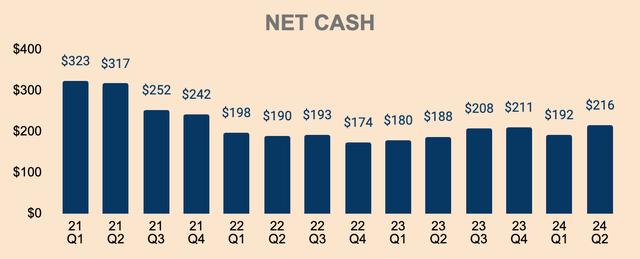

As of Q2, Hims has $216M of Net Cash with zero debt on its balance sheet — Net Cash should build up over time as the company is already Free Cash Flow positive.

Author’s Analysis

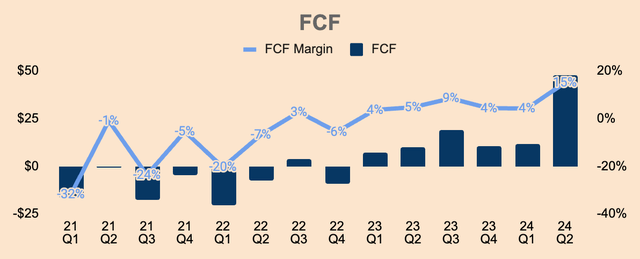

As a matter of fact, Hims just generated the highest level of FCF in its history, at $48M in Q2, representing a FCF Margin of 15%. And this is despite cost pressures from its Weight Loss division — imagine what the company’s FCF profile will look like once this division scales.

Author’s Analysis

With such a strong FCF generation, Hims took the opportunity to buy back shares. In Q2, the company repurchased $20M of its stock and has completely exhausted its $50M buyback program it initiated back in November last year. As a result, management authorized an additional $100M for buybacks, which should boost EPS growth as well as minimize dilution from stock-based compensation.

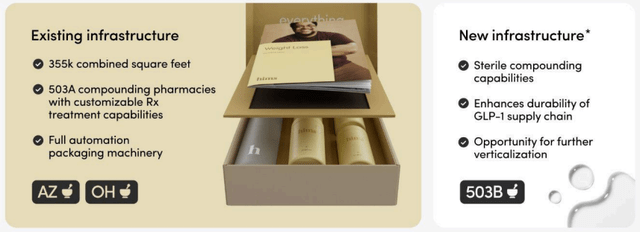

More importantly, Hims is reallocating a portion of its FCF for infrastructure upgrades. This includes investing in automation in existing facilities as well as acquiring an FDA-registered 503(b) facility, which is expected to close sometime later this year.

Over the long term, this acquisition will present additional opportunities across specialties such as hormonal therapy and other treatments that require sterile compounded medications. In the near term, this further enhances the durability of our supply chain for compounded GLP-1s and positions us to improve accessibility as we verticalize these operations.

(CEO Andrew Dudum — Hims & Hers FY2024 Q2 Earnings Call)

HIMS FY2024 Q2 Shareholder Letter

All in all, I like that management is focused on reinvesting into the business, which not only fortifies the company’s existing moats but also positions the company well to capitalize on the ongoing telehealth wave.

Valuation: Still Dirt Cheap

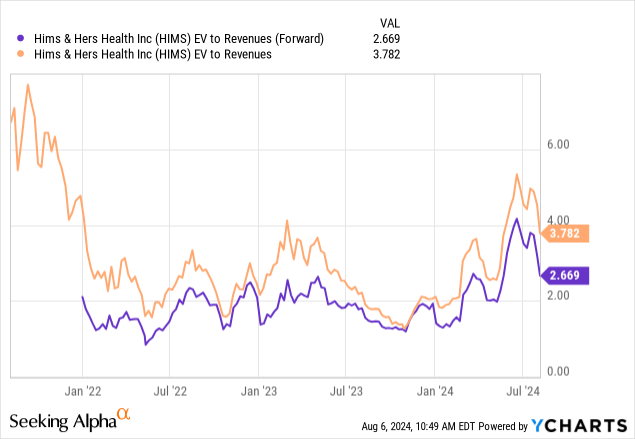

Despite being up 70%+ YTD, Hims stock is still significantly undervalued and underappreciated. The company now trades at an EV to Revenue multiple of just 3.8x. On a forward, basis that multiple drops to 2.7x, which is just ridiculously cheap for a company with software-like Revenue, 50%+ growth, high Gross Margins, robust FCF, zero debt, and near-flawless execution.

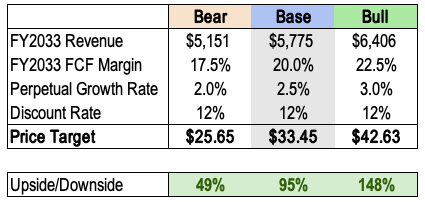

Considering its raised guidance and strong business momentum, I’m raising my price target from $28 a share in my previous article, to $33 a share. This represents an upside potential of about 95%.

As I write this, Hims stock is trading down on the back of a triple-beat quarter with the company set to accelerate growth for the remainder of the year. Perhaps, this is a great dip-buying opportunity.

Author’s Analysis

Risks

- Politics: CEO Andrew Dudum has made some rash political comments lately — he might do so again in the future. If he does, the markets might react negatively.

- Lawsuits: Healthcare is a sensitive industry. Any side effects, any negative developments, or any unforced errors, could lead to lawsuits against Hims. For instance, according to Hims, its “Compounded semaglutide has not been approved nor evaluated for safety and effectiveness by FDA”.

- GLP-1 Fad: Much of the recent runup in the stock price was due to the company’s new Weight Loss offering amidst shortages in GLP-1 drugs. As pointed out earlier, the shortages seemed to be over, which may call into question the durability of Hims’ Weight Loss offerings. Is it just a one-off event that temporarily and artificially boosted demand for Hims products? Though I have little doubt about Hims’ best-in-class offering, it’s still a risk worth considering.

Thesis

Hims just pulled off one of, if not, the best quarter ever since the company went public, demolishing analyst Revenue, EPS, and guidance estimates.

Considering strong business momentum, strong fundamentals, strong execution, strong product pipeline, and strong outlook, I believe Hims stock warrants a Strong Buy rating.

Despite the outperformance, the stock is in the red, now down more than 30% from its recent highs.

To me, this screams nothing but “Buy the dip!”

Read the full article here

")

")