")

Q4 2024 Earnings Call Transcript")

")

In my search for high yield income holdings to add to my Income Compounder portfolio, I sometimes use a fund screener to look for CEFs (closed end funds) that offer a steady monthly distribution. One such fund screener is available from AICA and uses data from CEFdata.com to support the screening criteria. While browsing for CEFs that offer annual distribution yields exceeding 10% that trade at a discount to NAV, I stumbled across a CEF that I had not heard of previously, and which has very little coverage on SA.

The Highland Global Allocation Fund (NYSE:HGLB) is a global equity and fixed income alternative asset fund that offers a monthly dividend of $0.081 per share, resulting in an annual yield of 12.5% at the current market price of $7.80 (as of 8/1/24). The fund advisor is NexPoint and the fact sheet from the fund’s website describes the fund strategy and investment objectives.

The Fund is a closed-end fund that seeks above-average risk-adjusted total returns by investing in U.S. and foreign equities and fixed income securities, along with select alternative investments in the pursuit of long-term capital growth and future income.

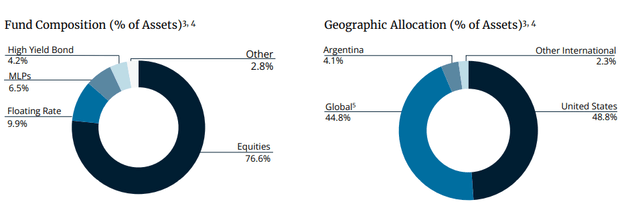

HGLB is a global fund that as of 3/31/24 held about 76% equities, about 10% floating rate fixed income, some MLPs, high yield bonds, and other alternative assets as shown on the fund fact sheet.

HGLB fact sheet

The fund’s investment objective is further described on the website:

The Global Allocation Fund, managed by James Dondero, invests primarily in U.S. and foreign equity and debt securities that the portfolio manager considers to be undervalued by the market but have solid growth prospects. Undervalued securities are those securities that are undervalued relative to the market, their peers, their historical valuation or their growth rate.

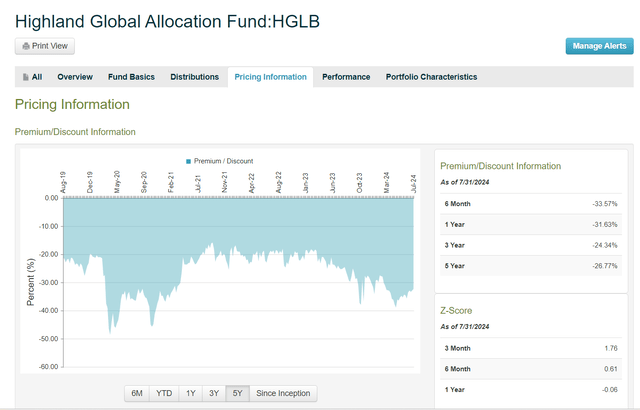

If the name, James Dondero, is familiar, you may recognize that he is also the fund portfolio manager for a sibling fund from NexPoint, the Highland Opportunities and Income Fund (HFRO). Like HFRO, the HGLB fund also trades at a substantial discount to NAV and has traded at a very wide discount for most of the past five years, as shown on this pricing chart from CEFConnect.

CEFConnect

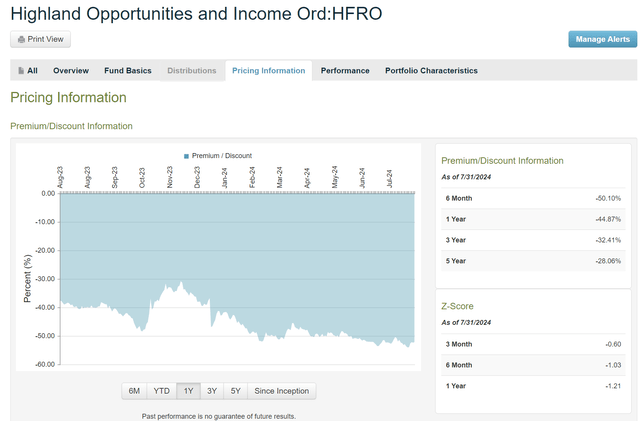

The current discount of -31% is slightly better than the 6-month average but even wider than the average 5-year discount of -26%. If the HFRO fund is any indication of what to expect from HGLB, it would not surprise me to see the discount continue to widen unless something changes due to activist pressure from someone like Saba Capital. The HFRO fund currently trades at a discount of more than -52%, which widened considerably after that fund slashed its distribution by half in January of this year.

CEFConnect

Although both funds are offered by NexPoint and James Dondero is portfolio manager for both HGLB and HFRO, and both trade at substantial discounts to NAV, that is about the end of the similarities.

HGLB is a much smaller fund with about $260M in net assets, the fund uses virtually no leverage (roughly 3% according to CEFConnect), and it attempts to offer an alternative investment option with low correlation to domestic equities. Although HGLB has an inception date of January 1998, it has gone through several major structural changes in the past ten years. This note from the fund website describes one of those changes that took place in 2013:

Note: Effective April 9, 2013, Highland Core America Equity Fund was renamed Highland Global Allocation Fund. At the same time, Highland Capital Management Fund Advisors, L.P. became the sole Adviser to the Fund and the Fund no longer utilizes a sub-adviser. In addition to these changes, the Fund’s investment strategies were revised and the Fund will no longer invest at least 80% of its assets in domestic equity securities.

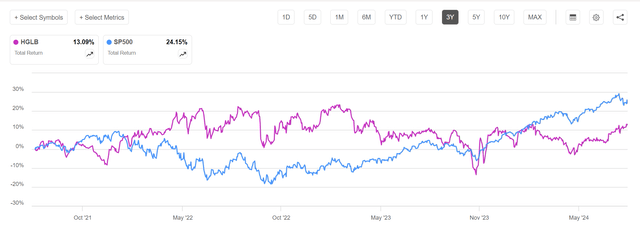

The Global Allocation fund was formerly an open-end mutual fund that converted to a CEF in February 2019. As a CEF, the fund has traded at a substantial discount to NAV since its inception as a closed end fund, and total return performance has suffered as a result. As we can see from the 3-year chart of total return performance, there is little correlation between fund performance compared to the S&P 500, thereby confirming that the strategy is working in that sense.

Seeking Alpha

Managed Distribution Offers Steady Income

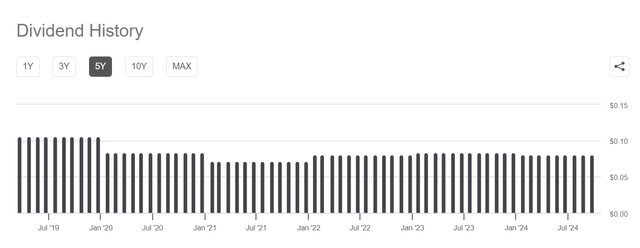

HGLB continues to pay a steady monthly distribution using a managed distribution policy, resetting the monthly dividend amount every January. In that respect, this CEF offers a reliable, high yield monthly distribution which is very attractive to income investors. The five-year dividend history as shown on the SA Dividend History page indicates the 12-month pattern with a cut from $0.1060 per month in 2019 to $0.0840 in 2020, reduced to $.0710 in 2021, then increased to $.0810 in 2022, followed by another increase back to $.0840 in 2023 and now set again at $.0810 in 2024.

Seeking Alpha

The fund website offers very little information regarding dividend coverage, with a link to the section 19a notice from December 2023 showing that about 68% of that month’s distribution was from NII and 31% from ROC. According to CEFConnect, the most recent distributions for 2024 have consisted of about one third income and nearly two thirds ROC.

HGLB Fund Holdings

The fund holdings are somewhat concentrated as well, with nearly one third of the total portfolio value tied to debt (9%) and equity (21%) holdings in a private company now called MidWave Wireless, formerly TerreStar Corporation.

Seeking Alpha

According to the fund’s Annual report issued in September 2023, the investment in MidWave Wireless was one of the positive contributors to performance in 2023.

MidWave Wireless, previously known as TerreStar, the Fund’s largest position, was a positive contributor to performance during the year. MidWave Wireless is a privately held, nationwide licensee of wireless spectrum, an asset that most people use every day. Spectrum is the radio frequency that carries all wireless communication signals. The Federal Communications Commission (the “FCC”), which has regulatory oversight in the space, administers spectrum for non-federal use. The FCC typically sells or assigns initial wireless spectrum licenses to market participants using an auction process. Access to spectrum may also be attained through the secondary market, which allows licensees like MidWave Wireless to transfer, sell, or lease spectrum, in whole or in part.

The substantial reliance on a single private company in a closed end fund makes me cautious about recommending it to anyone without doing further due diligence. Additional top holdings also pose a high level of risk in my opinion, including the Argentine debt and Whitestone REIT (WSR) positions. WSR just reported Q2 2024 earnings and missed on both the top and bottom lines, although they did update guidance for 2024. NexPoint Real Estate Finance (NREF) is also a risky selection based on past performance and their latest earnings report for Q2 2024 was just announced with a miss on earnings.

Overall, this looks like a tempting fund based on the managed distribution with a steady monthly high yield dividend, but I am unsure how well covered that dividend really is. Based on the substantial discount that has only grown wider this year, other investors do not seem to have a warm and fuzzy feeling about it either. And if the HFRO fund is any indication, there could be trouble ahead for HGLB, especially if the US economy starts to deteriorate.

I rate HGLB a Hold and would look for a reason to buy if there is a catalyst for the discount to close, such as activist pressure from Saba similar to what they have done with the Blackrock funds and other CEFs that they have impacted. Until or unless that happens, I intend to remain on the sidelines.

Read the full article here

")

Q4 2024 Earnings Call Transcript")