")

")

")

Google (NASDAQ:GOOG) was able to deliver excellent earnings in the recent quarter by beating estimates in terms of EPS and revenue. However, Wall Street has punished the stock, likely because of faster capex growth projections made by the management. It is very important to put the AI hype in context when it comes to Google and other Big Tech stocks. During the calendar year 2023, we saw rapid price growth in Google, Meta (META), and other tech stocks. A large part of this bull run was due to the cost optimization initiatives of these companies. Google was able to massively reduce its headcount, which helped improve the EPS growth trajectory. The rapid growth in self-driving service provides another runway for growth, as mentioned in the previous article.

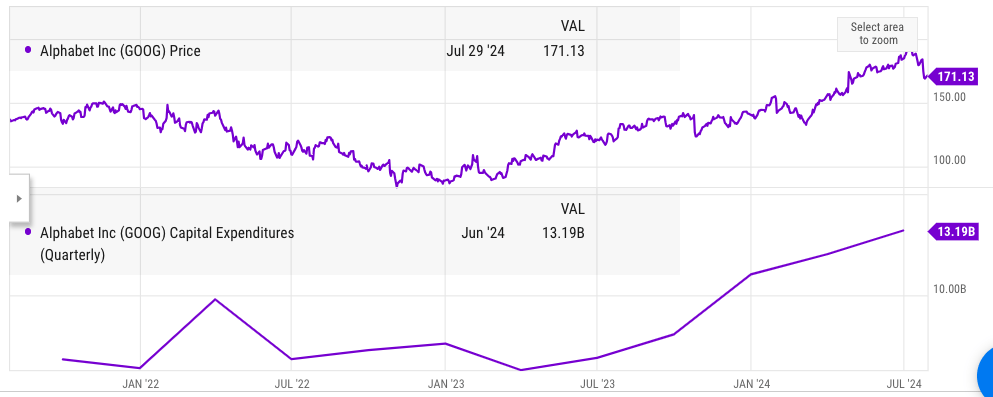

The AI hype likely did not play a big part in the bull run, as the valuation multiple of Google peaked at only 28 in 2023. In the recent quarter, capital expenditure came at $13.19 billion, compared to $12.01 billion in the first quarter of 2024 and a bottom of $6.3 billion in the first quarter of 2023. The forward guidance by the management mentioned that the company will maintain the current rate of $12-$13 billion in capex every quarter, which is close to $50 billion annually. This rate of capex is the highest investment level by Google, which has spooked Wall Street, as we could expect to see a negative impact on EPS trajectory over the next few quarters.

Google has a number of growth drivers like cloud, autonomous vehicles, subscriptions, and more. However, it will need to maintain discipline in spending if the management wants to show a good EPS growth trend. The monetization of many AI initiatives is still not clear. We could see some short-term headwinds due to higher capex, but the long-term growth momentum for the company is still quite strong. The forward PE ratio of Google is only 22 compared to 33 for Apple (AAPL) which has a significantly lower revenue growth trajectory. Google stock remains a Buy despite some short-term corrections.

Spending discipline is paramount

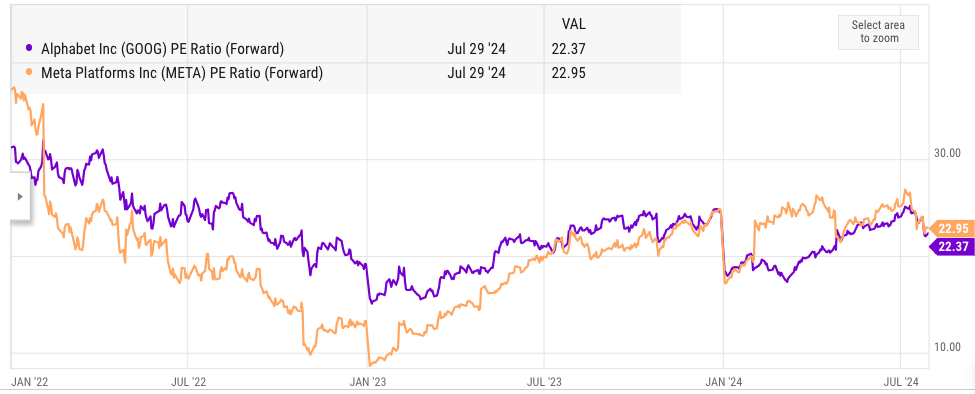

We have seen a strong bull run in most of the big tech stocks over the last few quarters. While AI hype has helped a few stocks, most of the other companies have seen bullish sentiment because of their cost optimization efforts. Google, Meta, and other tech companies announced massive layoffs in 2023 which helped in improving their EPS trajectory. This inevitably improved the sentiment towards the stocks and helped deliver one of the best bull runs for tech stocks in recent history for the last few quarters. The forward PE multiple did not expand significantly during this time despite the AI hype as shown in the following chart.

Ycharts

Figure: Forward PE ratio of Google and Meta. Source: Ycharts

The forward PE ratio of Google and Meta peaked at less than 25 in the recent bull run, and most of the stock price growth was due to strong EPS growth.

Ycharts

Figure: Recent spike in Capex by Google. Source: Ycharts

The reduction in headcount helped Google improve the profit margins over the last few quarters. Despite the recent 14% revenue growth, the headcount in the recent quarter came at close to 179,000 employees compared to over 181,000 in the year-ago quarter. The headcount reduction has certainly helped expand the profit margin and EPS growth. However, the management has announced that it will again start increasing the headcount.

Higher capex and employee count will inevitably hurt the EPS growth in the next few quarters. Hence, it is important to closely watch the future spending programs of Google in order to gauge the returns potential in the stock.

Future growth drivers are quite strong

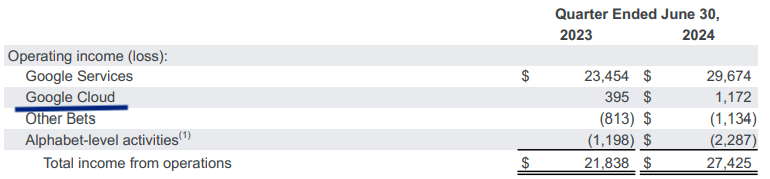

Google reported $10.3 billion in quarterly revenue for the Cloud segment, which is an increase of 25% from the $8 billion revenue reported in the year-ago quarter. The bigger news in this segment has been the strong margin expansion. The operating income in Cloud segment increased from $395 million to $1.17 billion. This increases the operating margin to 11% in the Cloud segment.

Google Filings

Figure: Operating income growth in Google Cloud. Source: Google Filings

There is a big gap between the operating margin of Google Cloud and the market leader Amazon’s (AMZN) AWS. Over the last few quarters, AWS has reported ttm operating margin in the range of 25%-30%. It is highly likely that Google Cloud would be able to close the gap in operating margin with AWS over the next few quarters as it gains better economies of scale. Combined with strong revenue growth in the Cloud business, we could see a rapid improvement in operating income, which will boost the overall margins for the company.

Amazon Filings

Figure: Recent operating margin of AWS. Source: Amazon Filing

If Google Cloud is able to show an average revenue CAGR of 25%, it could reach $150 billion annualized revenue rate by 2030. At 25% operating margin, this segment alone will add $40 billion to Google’s operating income by 2030. The recent ttm operating income of Google is $97 billion. If Google Cloud shows the above-mentioned revenue growth and margin trend, it could deliver a CAGR 6.5% growth in operating margin for the company on a standalone basis till the end of the decade. Google could invest this profit in other growth options and increase the buyback pace, which should help the EPS trajectory.

Another major growth segment in the self-driving business of Waymo. Google announced another $5 billion “multiyear” investment in this segment. The autonomous driving segment has required massive investment and lots of time. This would make a high barrier to entry for other businesses. We have already seen the poor performance of GM’s (GM) Cruise. Even Apple with its deep pocket has cancelled the self-driving Project Titan. I believe we will eventually see only three big players in this space: Google’s Waymo, Tesla (TSLA), and Amazon’s Zoox.

The robotaxis are just the tip of the iceberg in terms of the addressable market. They are also likely to be one of the most complex problems as it includes transporting people, which comes with its own regulatory headaches. It is inevitable that we will see this segment expand to robotrucks. According to the Bureau of Labor Statistics, there are many more times the number of truck drivers as there are taxi drivers. We could also see an expansion of this segment into package delivery.

Waymo has successfully completed 2 million paid trips and is rapidly expanding in new cities and increasing its customer base. Waymo has completed these trips in less than 10 months of operation. We could see a strong inflection point as it expands the service in other cities. A successful growth trajectory in Waymo should improve the bullish case for Google and also help improve the valuation multiple for the stock.

Another major growth segment is the subscription business. Google’s YouTube subscription has increased the customer base from 50 million in late 2021 to 100 million by early 2024.

Google Filings

Figure: Increase in subscription revenue. Source: Google Filings

The subscription business is becoming a key anchor service for Google, on which other services can be monetized.

Impact on stock price

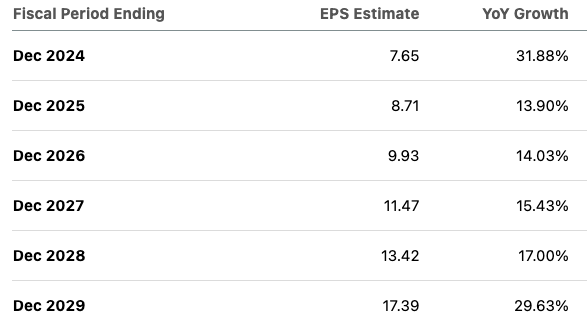

The management does not work in a vacuum, and it is likely that they will take the recent stock correction as a strong signal by Wall Street to rein in huge spending. The forward EPS estimates for Google are very good, and we could see an upward revision in them if the company is able to deliver good growth in Cloud, autonomy, and other segments.

Seeking Alpha

Figure: EPS estimates for Google over the next few years. Source: Seeking Alpha

The stock is trading at less than 20 times EPS estimate for the fiscal year ending 2025 and close to 17 times the EPS estimate for the fiscal year ending 2026. The PEG of Google stock is very good compared to many other big tech stocks.

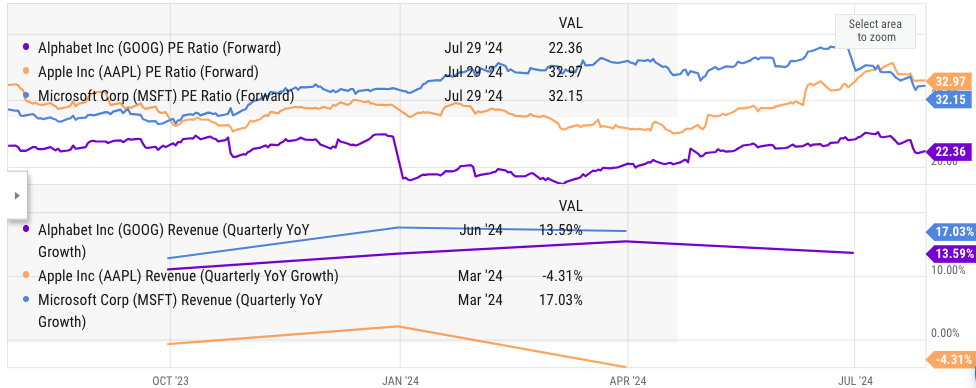

Ycharts

Figure: Key metrics for Google, Apple, and Microsoft. Source: Ycharts

Google is trading at a forward PE ratio of only 22 compared to 33 for Apple. On the other hand, the revenue growth of Google is significantly better than Apple. The long-term growth drivers for Google are also better than Apple due to Cloud and other high growth businesses.

If Google’s management is able to keep spending in check and deliver good EPS growth, we could see an improvement in valuation multiple by the end of 2024.

Investor Takeaway

Google stock saw a correction as Wall Street is worried about the high levels of capex for building AI capacity. The monetization of these initiatives is still not clear. Google will have to rein in spending if it wants to improve the EPS trajectory. The strong revenue growth and increase in margin in Cloud segment is a good tailwind for Google stock. There is still a big gap between the margins of Google Cloud and AWS. This should allow greater margin expansion in this segment over the next few quarters.

Alphabet’s Waymo has also been successful in commercialization of its self-driving service. We should see strong growth as the service is expanded in other cities, increasing the addressable market. Google stock has a forward PE ratio of only 22 compared to 33 for Apple. This shows that the stock is quite cheap, and long-term investors could use the recent correction to add to their position. I maintain a Buy rating for the stock.

Read the full article here

")

")

")