Clough Global Equity Fund (NYSE:GLQ) is an equity closed end fund we have not visited since 2022. In our last article on the name, we highlighted how the fund had a very high unsupported distribution rate and a significant amount of leverage, making it a high beta play.

In light of the equity market rally in 2024, we are going to revisit this name, its structure and composition, and highlight where the CEF fits within an investor’s portfolio.

A much deleveraged fund

When we last analyzed this name, the CEF had a high leverage ratio of 40%, which made the fund a very volatile proposal. GLQ in 2024 looks very different, with the name having lowered its gearing ratio significantly:

leverage (Fund Website)

The fund is barely leveraged at 12% now, making it a much less volatile CEF and in the process a more suitable fund for today’s environment which is filled with macro uncertainties.

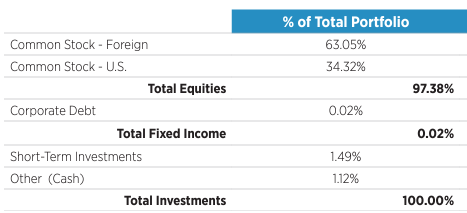

The CEF has also eliminated its bond holdings, essentially becoming an equity only closed end fund:

Allocation (Fund Fact Sheet)

The foreign stock sleeve clocks in at 63%, while the U.S. equity sleeve comes in at 34%. The Corporate Debt sector is a negligible 0.02% of the fund, and we expect this figure to move to zero as the remaining bonds mature. Short-Term Investments and Cash are utilized to manage the fund’s liquidity, so expect those allocations to persist.

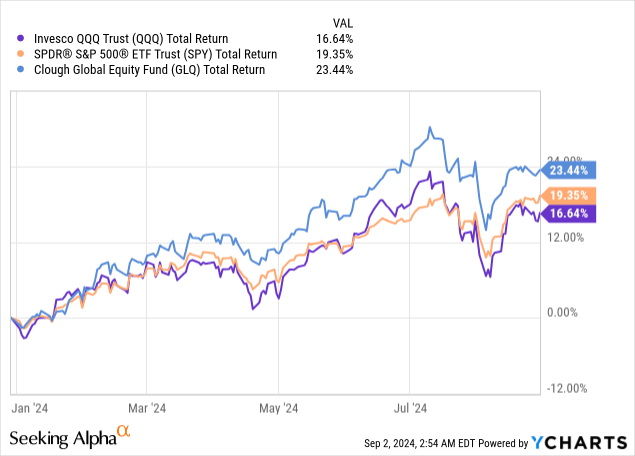

Beating the SPY in 2024

GLQ has managed to select outstanding individual names for its portfolio, beating both the S&P 500 and the Nasdaq in 2024:

Data by YCharts

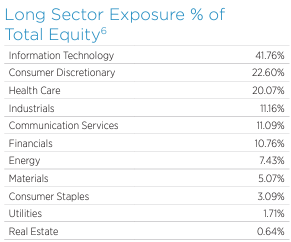

While the small fund leverage has helped, most of the outperformance in the name comes from its security selection, which is tech-heavy and contains a significant amount of semiconductor stocks:

Sectors (Fund Fact Sheet)

Information Technology represents 41% of the fund, followed by Consumer Discretionary at 22% and Health Care at 20%. Its top names include Apple (AAPL) at 8% of the fund, Microsoft (MSFT) at 7.5% and SK hynix (OTCPK:HXSCF) at 6.7%. SK Hynix is emblematic for the CEF’s outperformance, the name being a South Korean semiconductor vendor. This fund has the mandate to invest globally, and has been able to take advantage of global tech trends.

Doing a longer-term total return analysis is not useful at this stage, since the name has significantly deleveraged and narrowed its focus. The best way to think about this name going forward is as a global equity CEF with a small leverage ratio and a tech focus. We like this new format much better than the old one since the fund is a more honest and straightforward take on tech equities. Highly leveraged CEFs tend to take a significant beating in a down market, prompting managers to reduce leverage and impair NAVs permanently. While exciting in bull markets, high leverage constructs tend to ultimately cause NAV decreases. To note, GLQ was down -42% in 2022.

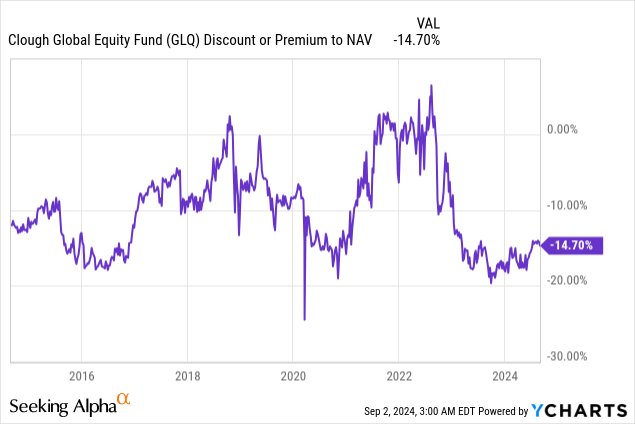

Premium/Discount to NAV

The CEF is now seeing its discount to NAV narrow slowly as it has normalized its structure:

Data by YCharts

After its significant loss in 2022, the CEF saw its premium of 3% move to a large -20% discount. This type of move is not unusual for high beta names, with significant losses also bringing along a widening in the discount to NAV.

The CEF has rebounded slightly, with the discount now at -14%, for a 6-point narrowing.

Distributions – Synthetic ROC utilization

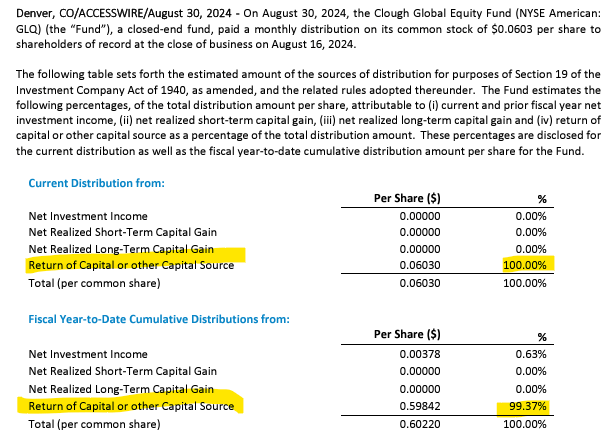

GLQ is an interesting CEF example because its Section 19a notice looks puzzling:

ROC (Section 19a)

While we saw the fund having an outstanding performance in 2024, its Section 19 notice displays a high ROC utilization. How is it possible? ROC is usually utilized by fund managers when they cannot crystalize capital gains in equities, and are thus forced to cover distributions with their own capital.

GLQ is a very rare breed where the fund chooses to use ROC in order to take a more aggressive stance without using more leverage. The fund has NAV performance to sustain its distribution, but has chosen to use its cash/liquidity for the distribution in order to increase its equity allocation. Rather than sell a portion of its holdings, the manager is betting less of a cash balance will be needed, and thus will use some of that for its distribution.

A high ROC figure here is therefore very different than the same one for an underperforming fund. The manager has chosen to optimize its cash and liquidity allocation, rather than use ROC to fund an unsupported distribution. The distribution rate is 10% currently; therefore the NAV performance shows us there is plenty of underlying dynamic total return to support that. We expect the figure to switch 100% to capital gains once the full liquidity calibration takes place.

GLQ risk factors and forward

The fund’s main risk factor is composed of tech and semiconductor stocks performance. A downturn in the respective sectors would see a significant move lower in the fund’s price, which would be slightly accelerated by the CEF’s leverage ratio. While the fund has significantly reduced leverage, a gearing ratio is still there, meaning the CEF benefits from it in up markets but also experiences faster moves lower in down-markets.

We are of the belief GLQ has made a smart move in lowering its leverage and adopting a distribution rate more in-line with historic total returns for equities. Long term, the fund should outperform if the portfolio management team continues to select the correct names, thus making the fund an appealing actively managed tech tilted portfolio.

Conclusion

GLQ is an equity closed end fund. The CEF has transformed itself in a low leverage, equity only vehicle in the past two years. The name is still trading at a large -14% discount to NAV due to its significant -42% loss in 2022. The CEF is overweight global tech names and semiconductors, which represent 41% of the holdings. We like the fund’s transformation from a high beta vehicle into today’s format, and we believe a lower leverage ratio will help the name long-term. The CEF has had an outstanding 2024 with a 23% total return, and given the stretched equity markets it falls in the hold category currently.

")

")

")

")

")

")

")

")

")

")

")

CEO Dave Ricks presents at 43rd Annual J.P. Morgan Healthcare Conference (Transcript)")