")

")

Gilead Sciences (NASDAQ:GILD) reported its Q4 2023 results on last Tuesday, the 6th of February. The company reported flat year-on-year product sales, and slightly decreasing sales on a quarter-to-quarter basis. Coupled with more or less stagnant earnings and low expected growth in the 2024 outlook, these results do not look very positive on their own. Gilead’s shares did not react well to the publication of its earnings: they lost almost 10 percent of their value since then. But when looking under the hood, the details of Gilead’s individual business lines paint a more differentiated picture, with some drugs like Veklury performing bad but some, like the oncology business, much better.

In my previous article about Gilead, which I wrote about a year ago, I focused on the transformation that the company has gone through over the past decade. Gilead has successfully transformed its business to become much more diversified than it was in the past. In the financial results of Q4 2023, it becomes clear that although Gilead’s main source of income remains products against HIV, but oncology is an important future source of growth for the company.

Results and financial metrics

Gilead Sciences published its Q4 2023 results after market close on the 6th of February, and let us zoom in on the company’s financial results here. In the Gilead Sciences Q4 2023 supplementary information, the following financial figures can be found. (If the numbers appear too small on your screen, please zoom in or consult the original source to which I linked).

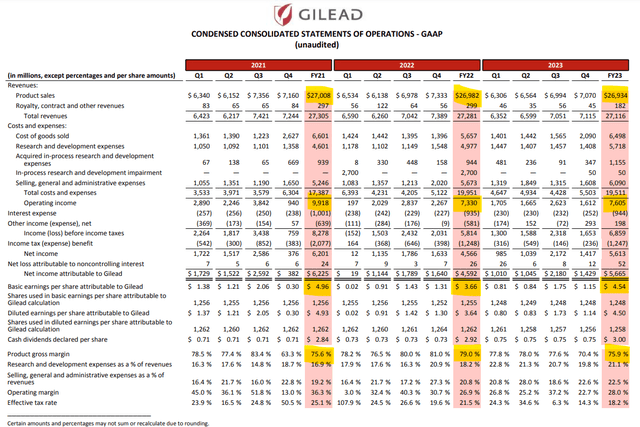

Gilead statement of operations (Gilead Q4 2023 supplementary info)

I highlighted the metrics that I want to focus on. First, as we can see, the total product sales of Gilead stayed more or less the same during the last three years, while the operating income of the company declined.

The product gross margin of Gilead in 2023 was 75.9%, down from 79 percent in 2022, but most notable here is that the most recent quarterly margin figure was the lowest of the last 2 years. As we can see when zooming in on these margin numbers, R&D and selling and administration costs increased as a percentage of revenue, while the effective tax rate decreased. As Gilead’s sales more or less stayed the same, an increasing cost burden of R&D and sales and administration could prove to become increasingly problematic for the company if costs continue to grow while revenues stay flat.

Gilead’s (basic and diluted) earnings per share (basic: $4.54) paint an unclear picture: a decrease compared to 2021 ($4.96), while they increased compared to last year ($3.66).

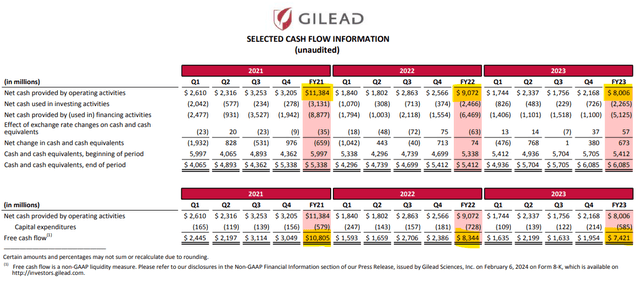

Gilead Q4 2023 supplementary info (Gilead Q4 2023 cash flow)

Now let us take a look at Gilead’s cash flow, which appears to go into the wrong direction. Net cash provided by operating activities and free cash flow have been decreasing since 2021: from $11.4B to $8B (cash by operating activities) and from $10.8B to $7.4B (free cash flow) are some quite large percentual drops.

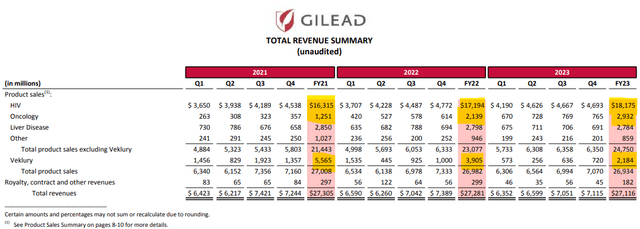

Gilead Q4 2023 revenue summary (Gilead Q4 2023 supplementary info)

If we look at Gilead’s revenue summary, split among different categories of product sales, we can see that the company’s flat revenue is not so flat among these categories. While the HIV business showed modest growth in revenue during the last two years, the biggest differences can be detected in oncology and Veklury. Veklury, which is used to treat covid cases, showed a strong decrease in sales and sales levels are very volatile over different quarters. Oncology on the other hand, shows strong growth, but started from a much smaller base in 2021, while it surpassed Veklury’s sales in 2023. If oncology (Yescarta and Trodelvy, among others) can continue its growth, it might well become a much more significant contributor to Gilead’s revenue over the coming years.

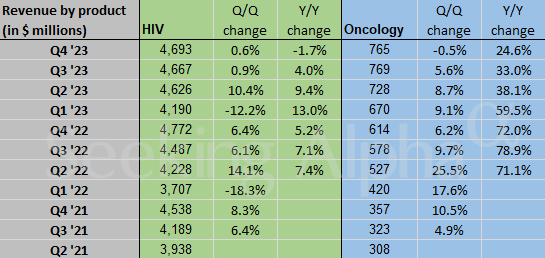

These revenue numbers are also made easy to digest by the Seeking Alpha graph about HIV and Oncology revenue over the last quarters:

HIV and Oncology quarterly sales (Seeking Alpha Graphs)

It might be a little bit worrying that oncology sales, which are supposed to be the big grower for the future of Gilead, have completely flattened out during the last quarter. Growth already decelerated from a quarter-over-quarter growth of more than 25 percent to single digit numbers in 2023, but during Q4 growth was even (slightly) negative.

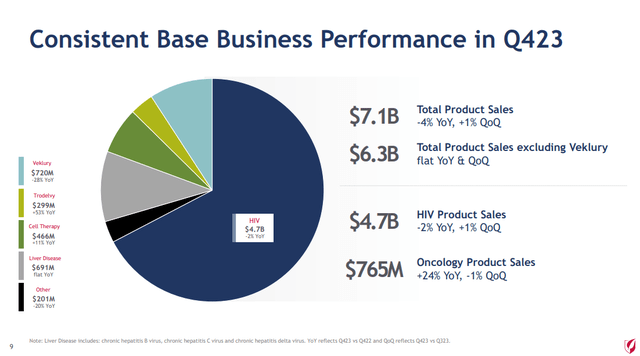

About Veklury: As Veklury sales have been decreasing quite quickly during the last two years and are very dependent on the number of covid patients being treated in hospitals, it is not surprising that Gilead included numbers ‘excluding Veklury’ in its Q4 presentation, as you can see below:

Gilead Base Business Performance in Q4 2023 (Gilead earnings presentation)

Here the company confirms that the most important differences among the drug categories are that oncology showed strong growth with +24% year-on-year, HIV more or less stayed flat and Veklury showed a strong decrease.

Outlook and valuation

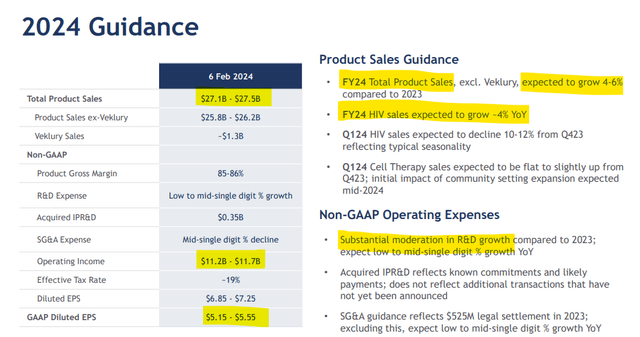

Gilead also provided a guidance for 2024 in its Q4 financial results. Let us go through the most significant aspects of it:

2024 Guidance (Gilead earnings presentation)

First, Gilead expects total product sales of $27.1-27.5B, which is slightly higher than current year. HIV sales are expected to grow by about 4 percent, while cell therapy is expected to not continue its previous growth in 2024. Also notable in this light is the recent failure of Trodelvy to pass phase 4 lung cancer trial, which decreases the scope for revenue increase for this drug.

Operating income is expected to come in between $11.2 and $11.7B, which is not bad compared to last year. Also, earnings per share expectations show some growth, but nothing spectacular. I also find it notable that the company mentions that there will be substantial moderation in R&D growth compared to 2023. As I mentioned, if R&D expenses would continue to grow while the company’s sales remain more or less flat, this could provide problems for profitability eventually. So it is good to see that this is not expected to be the case in 2024.

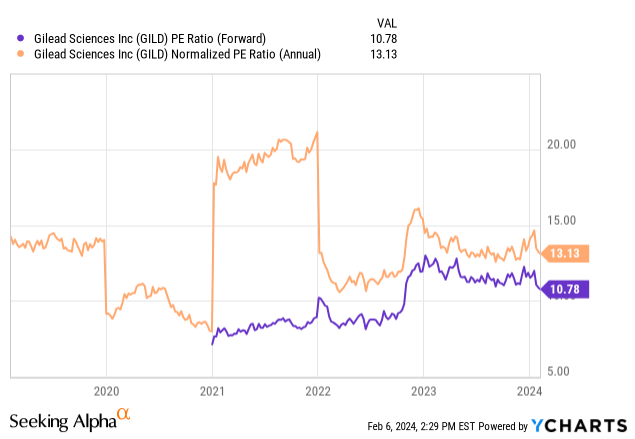

Now let us pay some attention to the valuation of Gilead in order to determine whether the company could be a decent investment at current share price levels. If we take a look at Gilead’s PE ratio, the company looks relatively cheap, with a forward PE ratio of below 11 and a normalized PE ratio of 13:

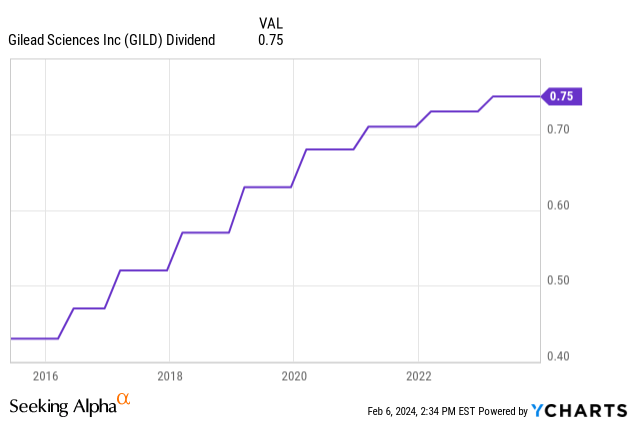

Also, Gilead pays an increasing dividend, which the company recently increased from a quarterly $0.75 to $0.77. This is not a substantial raise, but to be honest I believe the company’s current financial results also do not justify a large dividend increase. Also, the dividend yield is already relatively generous with 4%, but this is only the case because the shares are relatively cheap compared to peers. As we can see, Gilead has increased its dividend quite consistently over the last couple of years:

Conclusion

Looking at its main financial metrics, Gilead Sciences seems to be a company in stagnant waters: slightly decreasing sales, relatively flat earnings and a 2024 guidance with very modest growth expectations.

I believe the company has a decent pipeline (which I did not discuss in this article but you can find more details about it in Gilead Sciences’ earnings presentation), and Gilead is simply a profitable pharma company. But there appears to be no quick path to strong future earnings growth.

Gilead looks quite cheap at the moment with a forward PE ratio of below 11 and a (normalized) current PE ratio of just above 13, but the company is cheap for a reason: no growth and limited scope for quick future growth. Also, an important part of Gilead’s pipeline and high potential drugs have been acquired by taking over other companies, and although Gilead has been moderately successful with this, this is not enough to warrant a much higher share price multiple.

Most plausibly, I believe that Gilead Sciences will prove to be dead money on the short term. On the longer term, the company might be a good investment, and you get paid a decent dividend of more than 4 percent for waiting. I own a small position in Gilead myself, but I am not considering adding to this position any time soon.

Read the full article here

")

")

")

")