")

")

")

")

")

Getty Realty Corp. (NYSE:GTY), incorporated in 1955 and headquartered in New York, NY, is a net-lease REIT that primarily acquires, finances, and develops convenience and automotive single-tenant retail real estate assets.

Despite some risks faced by market concentration and changes in interest rates, GTY has potential. The REIT’s portfolio is mostly in markets with lower than average unemployment rates, its tenant base is well-diversified consisting of stable businesses, and its performance in the long run is reflective of its operational focus and lease structure. More importantly, however, the shares are undervalued, resulting in a high dividend yield, and there is not much to justify that.

Portfolio and Outlook

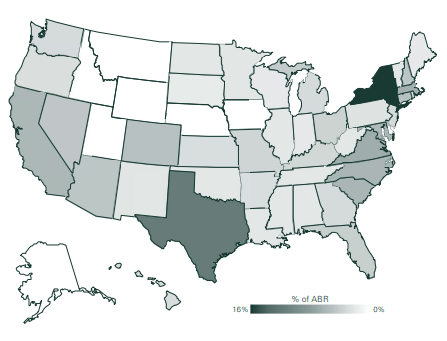

The REIT’s portfolio consists of 1,124 properties spread across 42 states. Its largest exposure is in New York (~16%), but it has a nationwide presence.

Investor Presentation

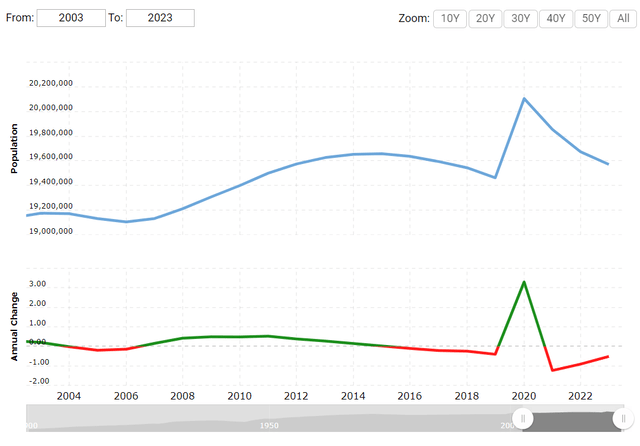

On one hand, the 20-year population growth trend in New York is not very promising:

MacroTrends

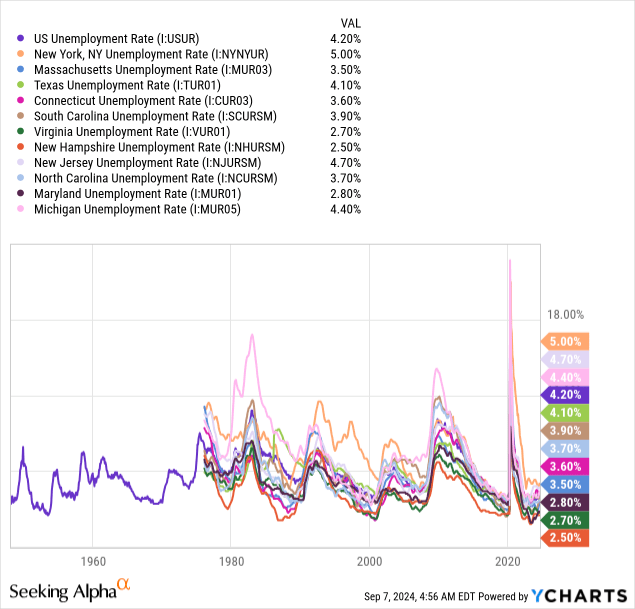

On the other, even though the unemployment rate in New York is one of the highest, most of the rest of the states in which it has the largest exposure have below-average rates, suggesting a positive outlook for the business:

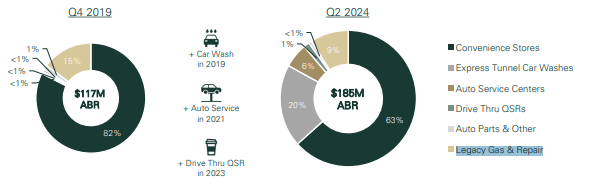

A robust portfolio is also supported by a solid tenant base. The tenants’ average rent coverage is 2.6x and the REIT enjoys a 100% rent collection rate (2023 and YTD). Additionally, in 2019, the REIT’s top tenants accounted for 82% of its ABR, and today they account for 68%. Another positive development was the decreasing reliance on convenience stores and gas/repair stations; in 2019, 82% of ABR came from convenience stores and 15% was generated by gas/repair stations but, today, both sources account for 63% and 9%, respectively, with the expansion of exposure to different businesses.

Investor Presentation

Another aspect of the quality of its portfolio is the way it expands it through sale-leaseback transactions, as it buys the properties from prospective tenants and then leases them back to them. That provides immediate financing to businesses and allows the REIT to decrease both the risk and the work that comes with first buying or constructing real estate with the intent to find tenants to lease it to and, as a result, occupancy is higher for such a retail REIT (99.7% as of the end of the last quarter). Moreover, Getty Realty underwrites net leases which result in lower maintenance CapEx and, therefore, a higher and more predictable cash flow.

With a well-diversified portfolio and tenant base, as well as an advantageous underwriting process and favorable economic drivers in its key markets, Getty Realty’s business should continue to grow at an attractive pace and provide value to shareholders. Speaking of which…

Performance

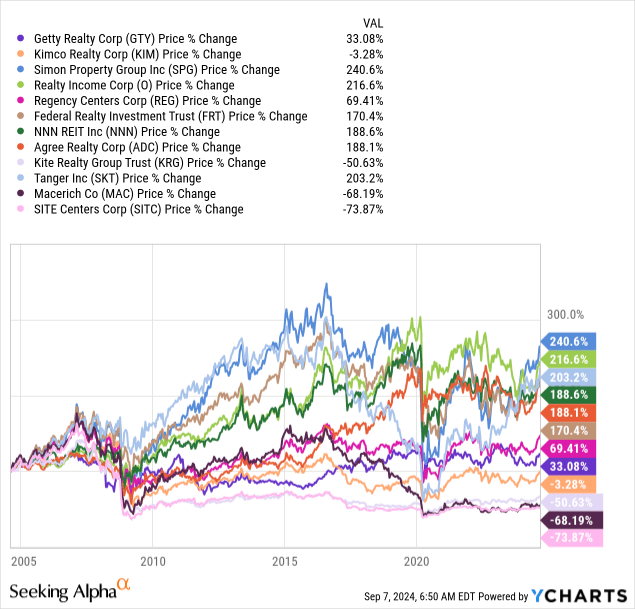

Merely judging from its price performance as a proxy for expansion, on a peer-relative basis it’s clear that there were plenty of retail REITs that grew much faster in the last two decades:

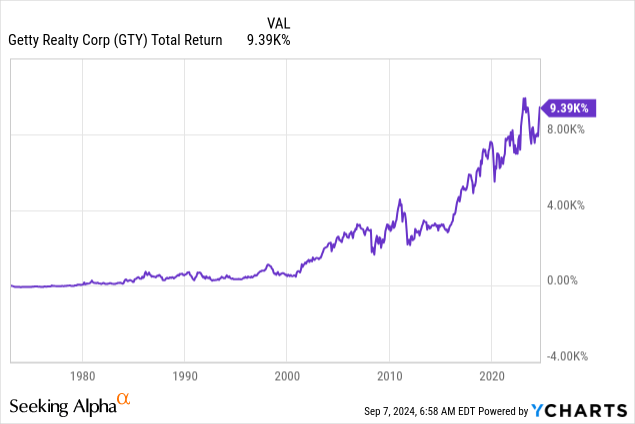

On a total return basis, however, it’s also evident that Getty has delivered great value to shareholders over the long term, with accelerating growth in the last decade:

Last year, the company made $172.8 million in annualized base rent, up 12.1% YoY. Occupancy was at 99.8% last year, the same level as the year before. Additionally, NOI increased by 9.13% and AFFO per share reached $2.25, a 5.14% YoY increase. The most recent results suggest a meaningful momentum in general, as ABR increased by 15% YoY and occupancy experienced only a minor decrease of 10 bps to 99.7%. Also, net operating income increased by 21.55% and AFFO by 3.57%.

2024 might be a slower year, however, judging from management’s guidance. Based on the mid-point AFFO of $2.31 per share, the implied YoY growth is 2.67%.

Leverage & Liquidity

The REIT’s BBB- rating by Fitch Ratings is justified given that only 44.37% of its assets are funded by long-term debt, which as of the end of the last quarter consisted of senior unsecured notes, a term loan, and a revolving credit facility. Its debt is also 100% unsecured which provides a lot of flexibility and the weighted average interest rate it pays on it is only 4.35%.

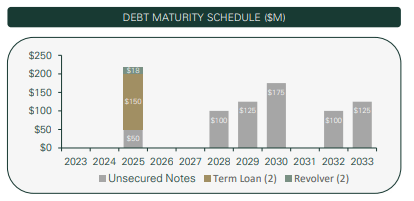

Also, with a Debt/EBITDAre ratio of 5.32x and interest coverage at 4.08x, there seems to be a high level of liquidity to service the debt. On top of that, its available liquidity represents 34.5% of the total debt and the upcoming maturities don’t represent a high refinancing risk, nor an immediate threat to the bottom line from higher interest rates because most of the 2025 amount is related to the credit facility and term loan, both of which are already burdening the REIT with a high interest rate.

Investor Presentation

Dividend & Valuation

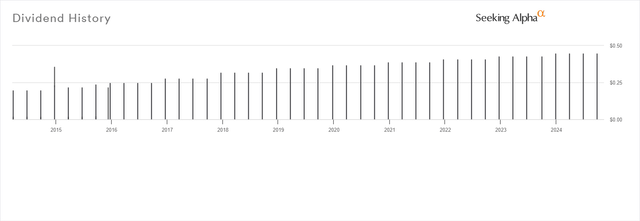

GTY currently pays a quarterly dividend of $0.45 per share, resulting in a forward yield of 5.68%. Its payout ratio based on forward AFFO is admittedly a bit high at 77.92% to make the dividend attractive to income investors, but it nevertheless leaves a high enough margin for both safety and growth. The track record is also impressive, as the dividend was increased by an annualized rate of 8.33% in the last decade.

Seeking Alpha

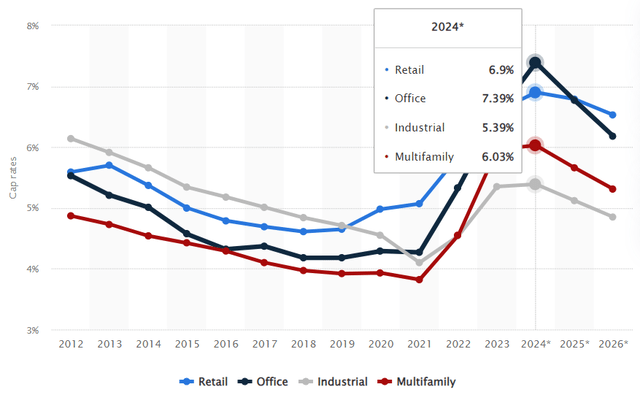

Its forward AFFO yield is also at 7.3% and that indicates good value despite the fact that its FFO multiple is only slightly below the average of its peers (14.39 vs 14.84). Moreover, its implied cap rate of 7.15% is a bit high compared to the forecast average cap rate for retail asset transactions in 2024 (6.9%); I also believe that Getty’s assets would fetch prices at a lower cap rate than the average as they don’t introduce the same risk observed in most retail assets because of the tenants they appeal to and the nature of the leases the landlords of such properties can underwrite.

Statista

Risks

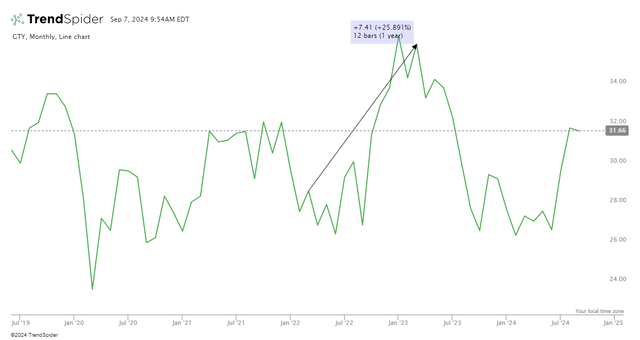

One of the risks that shouldn’t be overlooked is Federal Funds rate cuts, as this may put downward pressure on GTY’s price. Shortly after interest rates started climbing rapidly in 2022, GTY started rising too, perhaps due to the attractive tenant base and lease structure; Getty’s tenants enjoy relatively stable cash flows regardless of economic conditions as they cover essential needs and the leases may make investors extra confident in the growth of rents and dividends.

TrendSpider

A capital outflow driven by a less conservative market once interest rates go lower could be offset by a general transfer of capital from the debt market to equities, but that’s mere speculation and shareholders of GTY should expect short-term volatility, regardless.

As far as more long-term risks are concerned, the reliance on New York is not insignificant, and changes in the market dynamics there could visibly affect Getty’s bottom line in the long run.

Verdict

All in all, I think that Getty Realty enjoys the presence of all the return factors that I am looking for when searching for stocks that could outperform the market; small size, high quality, and a low price. For this reason, I am rating GTY a strong buy.

What do you think? Do you own this stock or do you favor some other REIT? I’d love to know! Also, please leave a comment if you found this post useful; it means a lot. Thank you for reading.

Read the full article here

")

")

")

")

")