")

Q4 2024 Earnings Call Transcript")

")

Synopsis

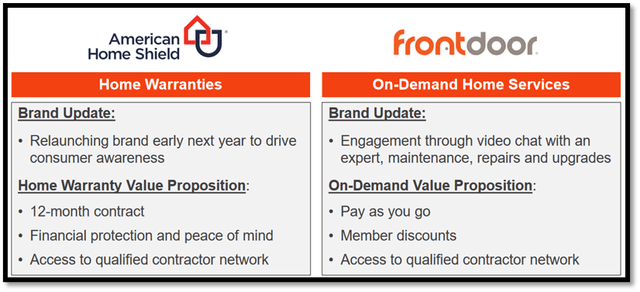

For every American homeowner, much effort and expertise in home servicing is needed in maintaining their living space, especially to avoid costly breakdowns of their essential appliances and home systems. With over 50 years of experience in home repair and maintenance and over 75 million service requests, Frontdoor (NASDAQ:FTDR) is the leading provider of home service plans in the US as measured by revenue. It primarily operates under the American Home Shield brand. In general, customers subscribe to its annual service plan, which covers the repair or replacement of essential parts of appliances and home systems. FTDR also offers on-demand home services and a recently launched digital app for home repair and maintenance. Customers have on-demand access to FTDR’s network of professionals that helps them get repairs, services, and upgrades. This is accompanied by its app-based interaction, where customers get a live chat with an expert. As of September 2023, there are 2.0 million service plans active in the US. Summarizing its two main brands, American Home Shield sells annual home warranties, and Frontdoor focuses on on-demand home services.

In 2022, FTDR’s revenue growth has shown signs of deceleration caused by a tough home market. In addition, margins have been contracting annually since 2019. Despite a challenging 2023 real estate market, 3Q23 revenue still grew 8%, driven by price increases. Looking ahead, the housing market is anticipated to grow in 2024, which will provide support for FTDR’s outlook. However, my target share price lacks a sufficient margin of safety. Therefore, I am recommending a hold rating for FTDR as of now.

Investor Relation

Historical Financial Analysis

Author’s Chart

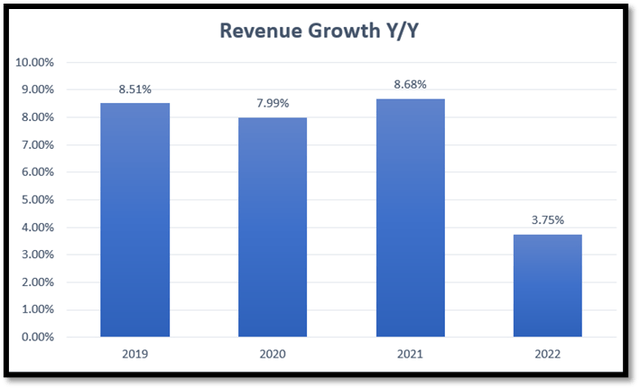

In the last four years, FTDR’s year-over-year revenue growth has been consistent in the range of 8–9%. However, in 2022, it fell significantly to 3.75%. During 2022, operations have been impacted by a tough home seller’s market due to declining home inventory levels and a rising interest rate, pulling back demand.

Author’s Chart

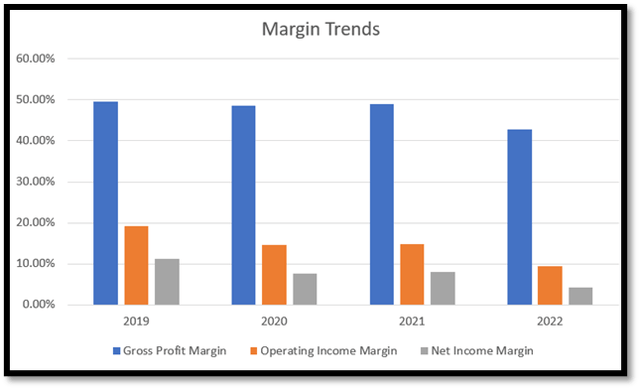

Margin has been contracting year-over-year, showing its worst performance in 2022. The cost of services was exceptionally high due to inflationary pressure. This includes increasing contractor-related expenses and parts and equipment costs. As a result of inflationary cost pressure on its gross profit margin, FTDR experienced some of the worst margins ever.

3Q23 Earnings Breakdown

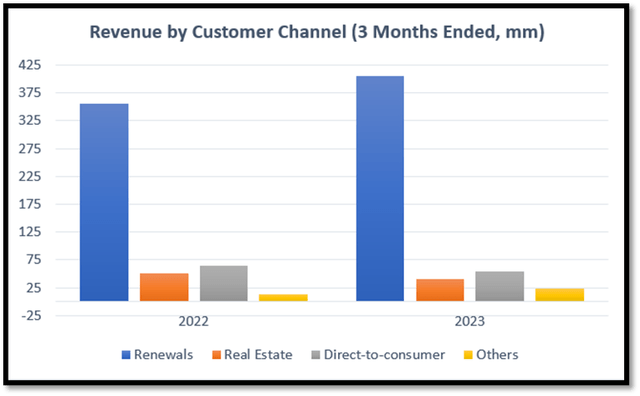

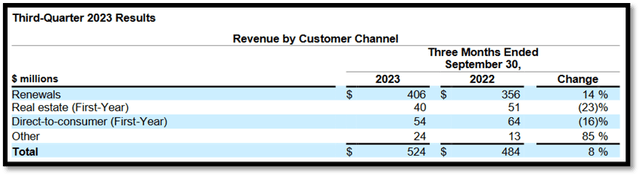

FTDR reported strong 3Q23 earnings results as total revenue grew 8%. This robust growth is driven by price increases while being partially offset by declining volume. Its 3Q23 revenue can be segmented into renewals, real estate, direct-to-consumer, and others. Renewals refers to the contract period of its home service plan, which has increased by 14% from $356 million to $406 million. Real estate revenue, where the service plans are sold via contracts in relation to real estate sales, has fallen by 23% in the challenging real estate market. Direct-to-consumer revenue fell by 16% due to a variety of macro conditions affecting demand for the home warranty category. However, other revenues, which consist of on-demand services and other fees, have increased by 85% due to the higher demand for on-demand services, which increased by $11 million.

FTDR has been experiencing a demand pullback for home warranties as a result of tough macro conditions such as the rising mortgage rate and home prices. Based on FTDR’s consumer research, there are still millions of households that are compelled to buy their product. This is because homeowners seek financial protection and reassurance for the inevitable breakdown of their home systems and appliances. Thus, management has decided to increase marketing expenditures for the American Home Shield brand and utilize strategic discounting to optimize demand conversion.

Author’s Chart

3Q23 Earnings Release

Challenging 2023 Real Estate Market

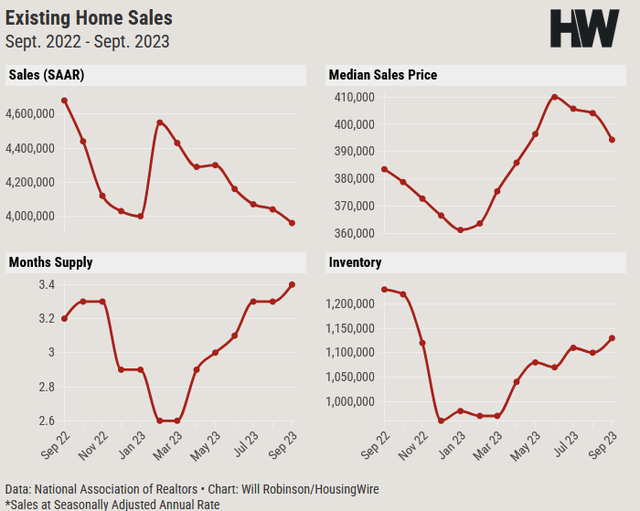

Management has stated that for the past nine months, their operations have been affected by the tough real estate market condition. This includes the fall in home resale transactions as a result of high interest rates and low inventory levels for homes. This has impacted FTDR’s Real Estate First-Year revenue. Data from October 2023 has shown that existing home sales have slid by 15.4% from 4.68 million to 3.96 million. Low home inventory levels and a high median sales price will further exacerbate the sales.

HousingWire

2024 A Potential Year for Inflection

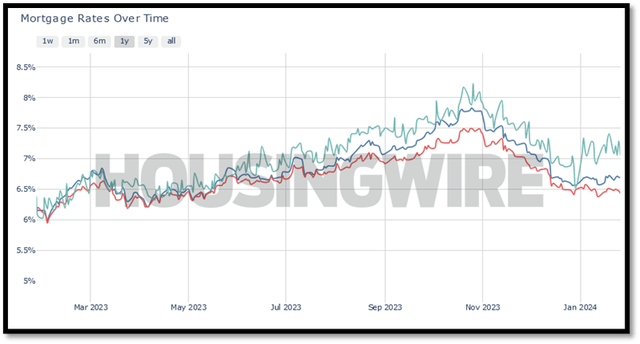

However, this might be a different case for 2024. Over the month of December 2023, there has been an 8.3% increase month-on-month in pending home sales. This was the largest monthly jump since 2020. The mortgage rate has slid to 6.6%, the lowest level since May 2023. The declining trend in mortgage rates is a welcome sign for households seeking to buy a new home but may create pressure on home inventory levels. As a result, mortgage applications grew by more than 10%. National Association of Realtors [NAR] also forecasts that the Federal Reserve will further cut the interest rate four times in the upcoming year. Therefore, the positive growth in the housing market is a promising start to 2024 for FTDR.

HomeWire

Strong Renewal Channel Expected to Remain Robust

Based on its most recent 3Q23 earnings, the renewals channel accounts for ~77% of its total revenue. Therefore, it forms the largest share of its total revenue. Although demand in its direct-to-consumer and real estate channels was weak, renewals remained strong, as it reported growth of 14%. In addition, the retention rate grew to 76.2% despite the 11% price increase. Renewal customer count remained flat at 1.55 million, even though prices have increased. For the full year 2023, management is expecting its renewal channel to grow by ~15%. From this, it shows management confidence in the robustness and strength of its renewal channel.

However, do keep in mind that its direct-to-consumer and real estate channels, both are expected to decline. Direct-to-consumer is expected to fall in the low double-digit range, while the real estate channel is expected to fall in the mid-20% range due to the challenging real estate market as well as macroeconomic conditions. Despite this, for the full year 2023, management has raised its revenue guidance to be in the range of $1.765 billion to $1.775 billion, which represents a year-over-year growth of 6%.

Discounted Cash Flow Model

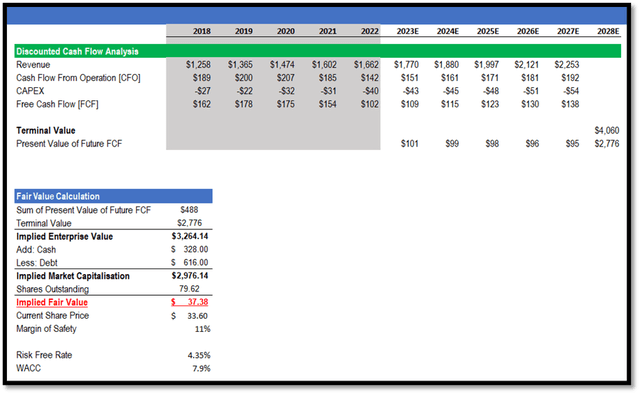

As there are no suitable competitors that are listed to be used to compare against FTDR, I will be using a simplified 5-year DCF model with a terminal value exit to determine FTDR’s intrinsic value.

For 2023 and 2024, FTDR’s revenue growth that I have used is in line with the market consensus of ~6%. I believe the market estimates to be reliable, as they are in line with management’s guidance as well as the growth catalyst discussed above. For 2025 to 2027, I expect the growth rates to be in line with 2024’s growth estimates. Therefore, my model also uses ~6% for these remaining years. This growth assumption ensures that my DCF model stays conservative.

FTDR’s 5-year median CFO as a percentage of revenue is ~14%. In my model, I utilized its most recent financial year’s percentage of ~9%, and I extrapolated for the next 5 years. As it is below its median, I believe my CFO assumption is conservative.

For CAPEX, its 5-year median was 2% of revenue, and I used this rate for the next 5 years to ensure consistency. When I deduct CAPEX from CFO, it will give us FCF, and I will discount FCF back to its present value using FTDR’s WACC of 7.9%.

To calculate the terminal value, I require a risk-free rate. The US 30-year Treasury yield provides a good proxy for this, and it is 4.35%. Using 2027’s FCF, WACC, and risk-free rate and applying them to the Gordon Growth formula, my terminal came up to $4.036 billion, or a present value of $2.759 billion.

Using FTDR’s WACC to discount its future FCF, the sum of the present value of its future FCF is $487 million. Hence, by adding the present value of its FCF and terminal value, its implied present enterprise value is $3.246 billion. Based on my conservative assumptions discussed above, my implied intrinsic value for FTDR is ~$37.38. Compared to its current traded price, there is an implied upside of around 11%.

Author’s Valuation Model

Risk

As discussed above, the real estate market is expected to recover in 2024, driven by interest rate cuts that impact mortgage rates. However, if inflation were to take a turn for the worse, an interest rate cut might not happen or could occur at a slower pace. In this scenario, mortgage rates would be affected. This would negatively impact the housing market, which ultimately could affect FTDR.

Conclusion

FTDR has been experiencing a tough macroeconomic environment with rising mortgage rates and inflationary pressure. Despite all of that, the company has demonstrated a solid performance in the renewals sector, which forms a significant portion of its revenue. This underlines its strength in customer retention and service quality, even in the face of increased prices. Looking forward to 2024, it’s a year that has the potential for a turnaround for FTDR, as the housing market has been showing signs of recovery and is expected to grow. Even though the upside potential is positive, I believe my target share price lacks a sufficient margin of safety. Therefore, I am recommending a hold rating.

Read the full article here

")

Q4 2024 Earnings Call Transcript")