")

")

")

")

Brief Overview

Fox Factory (NASDAQ:FOXF) is a multi-product company that designs and manufactures vehicle accessories. They are mostly known for their suspension products, particularly in the mountain bike business, where Fox Factory products are considered among the best available and command premium prices. Over the years and through several acquisitions, the company has expanded to include many other businesses, almost always focusing on peripherals. Nowadays, Fox Factory has ventures in trucks, motorcycles, snowmobiles, custom vans, wheels, and even baseball bats.

Most of these other businesses were acquired in the past ten years. The many acquisitions boosted growth, and Fox Factory was popular with investors for that reason. However, starting in 2023, the company has faced headwinds, growth has slowed down, and investors started questioning the acquisition strategy. For a more detailed look into Fox Factory, please refer to my first article on them.

2Q24

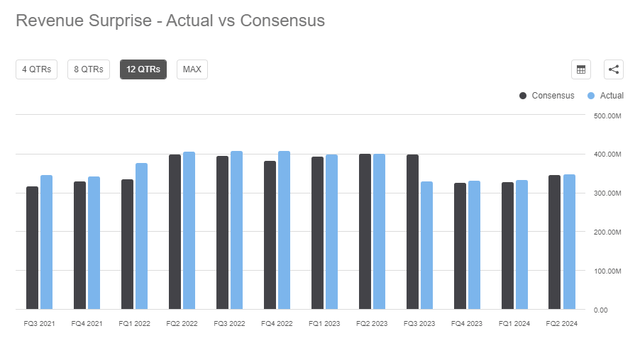

Fox Factory’s revenue came largely in line with consensus, with a slight beat of 0.51%.

Revenue x Consensus (Seeking Alpha)

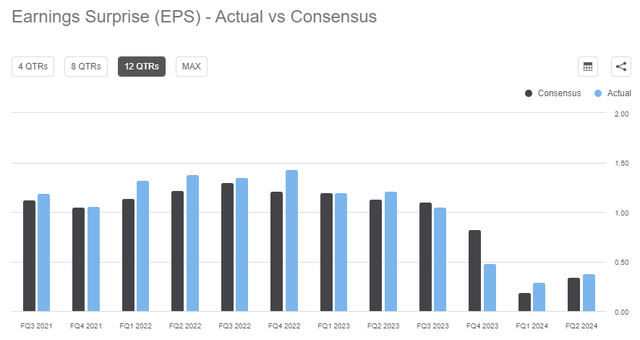

Earnings were slightly more positive, with a 9.75% beat.

Earnings x Consensus (Seeking Alpha)

However, the stock tanked in after-hours trading and the following day. The most likely reason is the guidance delivered by the company. Over the past three earnings, management had been warning the market that the first two quarters of 2024 would be rough, but that they expected the situation to normalize in the second half of 2024. Here’s an excerpt from their 1Q24 call:

In closing, we continue to be positive about the back half of the year. In terms of innovation, we have a robust product roadmap in place. We eagerly anticipate our upcoming product launches, which are happening across all three segments of our business, and we are confident that these new products, coupled with our spec share gains in the OEM market, will drive growth in the second half of the year.

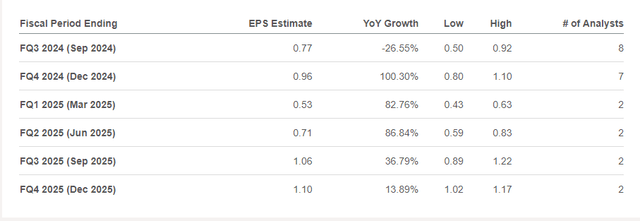

As a result, market consensus had adjusted to expect a stronger second half. Right before 2Q24, consensus EPS for 3Q23 and 4Q24 were $0.77 and $0.96, respectively.

EPS Consensus (Seeking Alpha)

However, the company just released its guidance along with earnings, and it was way below those numbers.

For the third quarter of fiscal 2024, the Company expects net sales in the range of $355 million to $385 million, vs. $417.38M consensus, and adjusted earnings per diluted share in the range of $0.35 to $0.50, vs. $0.81 consensus.

For the fiscal year 2024, the Company now expects net sales in the range of $1.407 billion to $1.477 billion, vs. $1.54B consensus, adjusted earnings per diluted share in the range of $1.40 to $1.72, vs. $2.40 consensus, and a full year effective tax rate in the range of 15% to 18%.

It was that much lower guidance that caused the stock to tank, in my opinion. However, it wasn’t that surprising to me, as I expected the company to report weak numbers. The reason for my bearishness with Fox Factory is two-fold:

First, and this is being amply discussed in the financial media, the U.S. consumer is in a weak spot, and is not buying discretionary goods, particularly ones that come at premium prices.

Second, I’m a strong opponent of “diworsefication”, and I believe that in most cases, it creates a worse scenario for the company and the shareholders. Fox Factory has made several acquisitions over the years, and I cannot see any kind of synergy when it comes, for instance, to making baseball bats. The only argument you could possibly make for these purchases is, if Fox Factory management bought all of those businesses at a Warren Buffett-level of value investing, which I don’t believe they did.

Digging into the numbers.

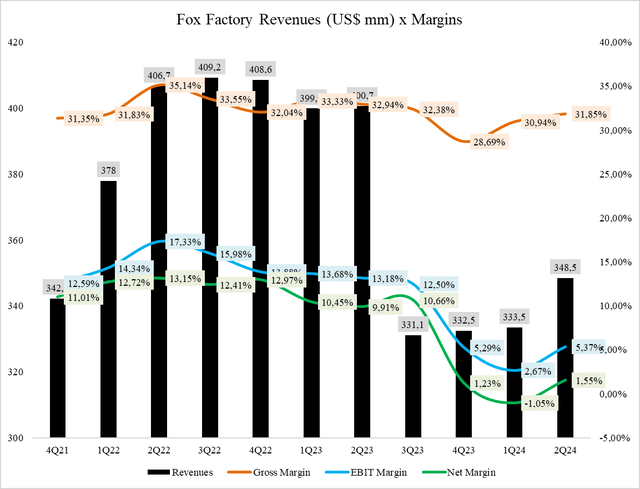

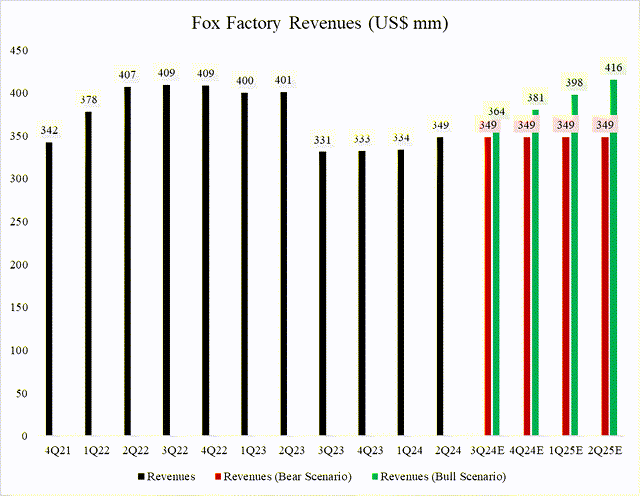

Fox Factory Revenues (US$ mm) x Margins (Company Filings, Author)

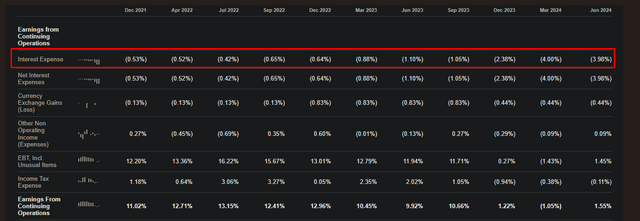

Fox Factory has a margin problem. While the quarterly revenue drop from ~$400 mm to ~340 mm might not seem much; the unit economics of the business resulted in severe margin damage. Another thing is that Fox Factory had to get a lot of debt for the Marucci acquisition and now the interest expenses are bigger too, eating away at profits.

Interest Expenses as % of Revenue (Company Filings, Author)

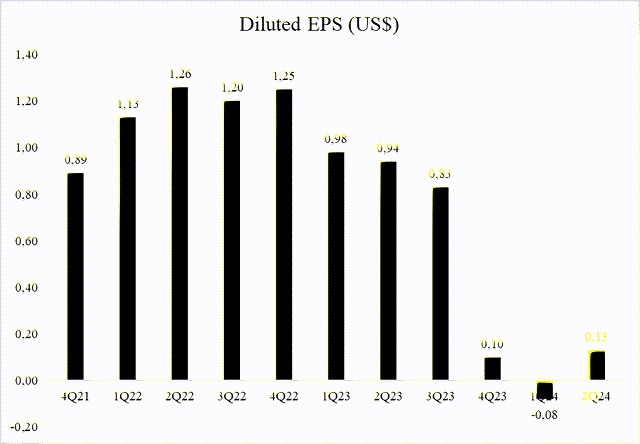

As a result, EPS has tanked.

Diluted EPS (US$) (Company Filings, Author)

It seems to me that the Marucci acquisition was a shot in the foot, as the high debt resulted in higher interest expenses. That, combined with a slowdown in the business, makes me question whether Fox Factory is capable of being profitable in the current markets.

Adj. EPS vs EPS

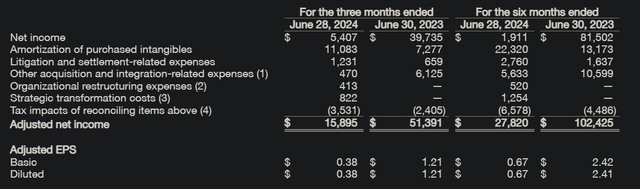

There’s a bit of confusion when it comes to Fox Factory’s earnings and EPS, because the company often refers to Adjusted Earnings. In my opinion, the changes it makes to earnings aren’t a fair representation, as they result in much larger earnings, and most of the expenses they add back are related to the many acquisitions they have made over the years.

Net income vs Adj. Net income (Company Filings)

Management keeps pushing forward their return to growth, even though it claims it doesn’t have much visibility beyond the next quarter.

Michael Dennison

We’re seeing limited visibility in Q4 this early. But Q3 is trending like we saw in Q2, where Q3 is above Q2 and looking strong. So it’s pretty positive. Like I said in my comments to Larry, our back half predictions and projections for both the bike business and our Marucci business is on plan. They’re doing very, very well.

Scenarios & Valuation

I usually like to build two scenarios: a bearish one and a bullish one. Here, for the bullish, I assume the company will return to its previous revenues, while for the bearish, I hold revenues steady.

Fox Factory Revenues & Scenarios (Company Filings, Author)

The company’s gross margin is very stable at ~32%, so I leave that unchanged. I leave operational expenses fixed at US$ 92.2 mm, which is the number they last reported.

Fox Factory Operating Expenses (Seeking Alpha)

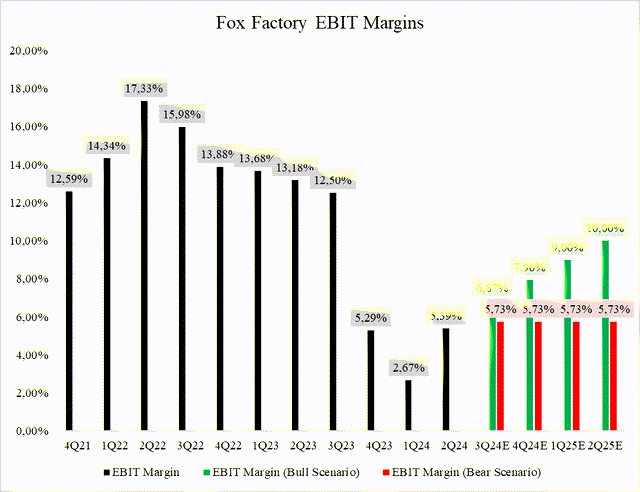

Here’s the impact on EBIT margins from the two different scenarios. Note also that EBIT margin doesn’t return to ~13% because the company has increased its operating expenses this year considerably (~US$ 90 mm from ~US$ 77 mm).

Fox Factory EBIT Margins (Company Filings, Author)

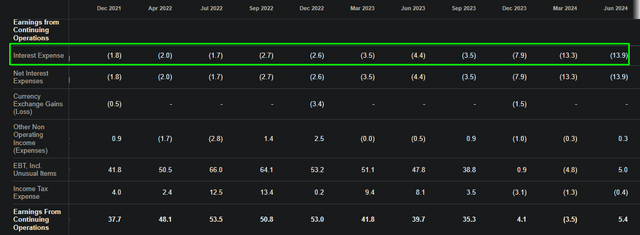

The next biggest expense is net interest expenses. That is much higher now, thanks to the leverage from the Marucci acquisition. I leave that unchanged.

Fox Factory interest expenses (Seeking Alpha)

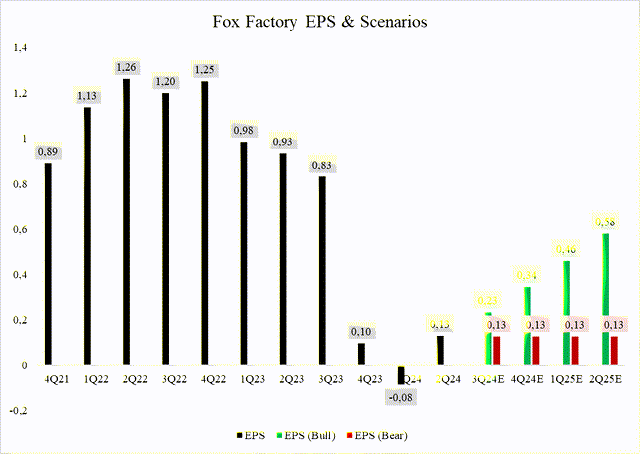

Finally, using the average tax rate from Fox Factory’s profitable quarters, I arrive at two EPS scenarios.

Fox Factory EPS & Scenarios (Company Filings, Author)

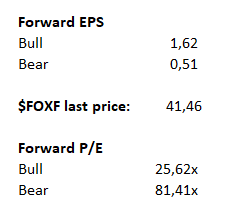

So, according to my calculations, and as of last price of $41.46, Fox Factory is trading at either 25.62x forward earnings in the bull scenario or 81.41x in the bear one.

Fox Factory forward EPS and PE Ratio (Author)

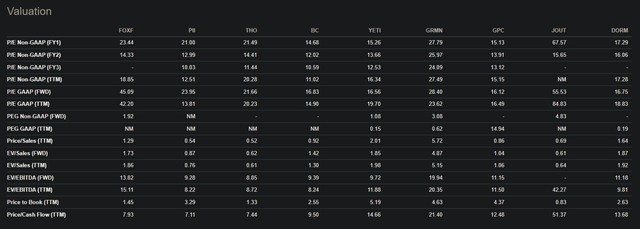

Here’s what I consider Fox Factory’s closest peers to be, and what they trade at:

Fox Factory and Peers Multiples (Seeking Alpha)

It’s my opinion that the stock is still expensive at current levels, as it’s trading at 25.6x forward earnings in the bullish scenario, which isn’t cheap to me. The bear scenario is obviously catastrophic, but I would like to see the stock trading at below 20x earnings at least in the bull scenario, for me to even consider it fairly priced.

Risks & Conclusion

Despite the recent selloff, I don’t believe Fox Factory is cheap. The biggest risk to this thesis, of course, is that the Marucci acquisition starts really surprising to the upside. This is a possibility, and the management has said so in the 2Q24 earnings call:

To that end, I’m particularly thrilled to highlight that we recently announced the exclusive license agreement with Major League Baseball, designated Marucci and Victus as the official bats of MLB starting January 1, 2025. This 4 year agreement not only underscores our brand’s leadership in professional baseball, but also provides exclusive rights for our products. This partnership, combined with Lizard Skins’ position as the official bat grip of MLB, further cement our status as a premier choice for players at all levels.

With this new MLB agreement on the horizon, we’re even more excited about Marucci’s future growth potential and congratulate the team for achieving this distinction. Looking ahead, we’re optimistic about the trajectory of SSG. The anticipated recovery in the bike segment, coupled with Marucci’s consistent strong performance and our exciting product pipeline positions us well for continued growth through the second half of this year.

While Marucci might be going well, I think most segments aren’t, and the risk x reward of the stock doesn’t seem attractive to me at current prices.

Read the full article here

")

")

")

")

")

")