")

")

Shares of F&G Annuities & Life (NYSE:FG) have been a strong performer over the past year, rising 34%; however, the stock is down nearly 20% since its recent high amid the broader market pullback. Given its higher-risk investment portfolio, shares can exhibit significant market sensitivity, but the magnitude of this drop has been jarring. Because of this pullback, shares are down 9% since my May article, recommending them as a “buy.” That makes Monday night’s earnings release well-timed, and I remain bullish on FG.

Seeking Alpha

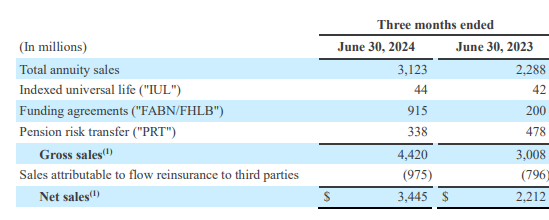

In the company’s second quarter, F&G earned $1.10, beating consensus by $0.02, as gross sales rose by 47% to $4.4 billion. This represented a record level of gross sales, given the strong demand for annuity products. Net sales of $3.4 billion were also up 30% from last year. As investors look to lock in current rates, we have seen significant demand for annuities, with total annuity sales up 36% from last year.

F&G

In addition, F&G has meaningfully increased funding agreements sales. Here, it sells bonds that are backed by an insurance policy. It then uses the proceeds to invest in its general account, and it earns the net spread between its invested interest rate and what it pays on the notes. These are purely a net investment income vehicle with no material underwriting risk. Pension risk transfer (PRT) sales tend to be volatile as they are usually large chunks of plans.

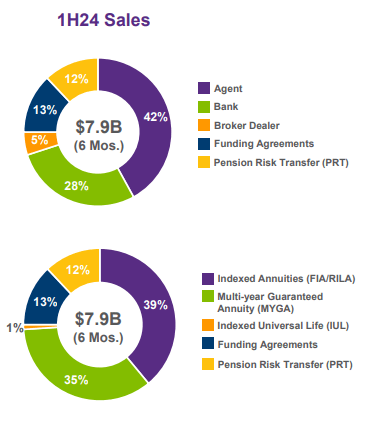

So far in 2024, indexed annuities account for the plurality of sales, followed by guaranteed annuities. Annuities account for about 75% of sales. Q2 saw a bit less pension risk transfer activity and a bit more funding agreement. F&G also continues to maintain a fairly diverse sales stream, relying on both agents and partner banks and broker dealers.

F&G

While gross sales have been very strong, there has also been increased surrender activity. For instance, F&G had $578 million of net fixed index annuity (FIA) flows. This is down from $628 million last year even with gross sales rising substantially, due to increased terminations. During a period of time after buying an annuity, the consumer can surrender the policy and receive cash. A policyholder may choose to do this when rates have risen substantially as their policy came at lower rates. With cash, the policyholder can buy a new policy at today’s rates.

Now, it is important to note that when a policyholder chooses to terminate the policy that they pay a penalty. This leads to a surrender fee and allows the insurer to book a profit. It also frees up the capital associated with that policy to be used for new policies, which is why we are seeing such strong sales activity. Importantly, even with surrender activity elevated, F&G continues to grow. Its AUM of $52.2 billion was up 13% from last year.

Thanks to higher interest rates and a growing portfolio, F&G earned $684 million of investment income from $252 million last year. $145 million of investment income came from alternatives. This underperformed expectations by $20 million or $0.15. Over the long-term, F&G targets a10% return in alternatives; however, they have generated 8.1% this year.

Now, F&G has earned a 13% historical average return on this allocation, so it has been a prudent investor. Alternative returns can be volatile. While the strong stock market should be supporting returns, elevated interest rates have weighed on private equity and private real estate valuations. Returns here can lag public markets by about a quarter, so if we do see the recent market weakness persist that is likely to be a headwind for results, but it may impact Q4 earnings more than Q3 earnings.

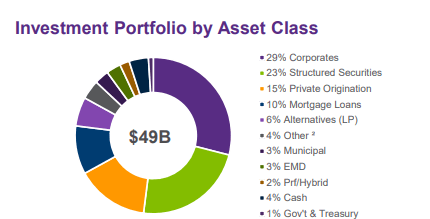

Within its investment portfolio, 96% of fixed income is investment grade. However, its fixed income allocation includes exposures to less liquid markets that have higher perceived risk. Due to this, I have mentioned that we can see F&G come under pressure during periods of market turmoil, as we have seen recently. Notably, it has 23% in structured securities and 15% in private debt, as well as a meaningful exposure to real estate.

F&G

Structured securities tend to be less liquid, as their tranche sizes can be relatively small. During periods of market stress when liquidity is reduced, illiquid securities can have even wider price swings, causing exaggerated market movements. This can lead to painful losses if a forced seller. Importantly, given the long-term nature of annuity contracts, F&G is highly unlikely to be a forced seller and can instead ride out periods of stress. What is critical is that its securities mature at par and do not default.

F&G

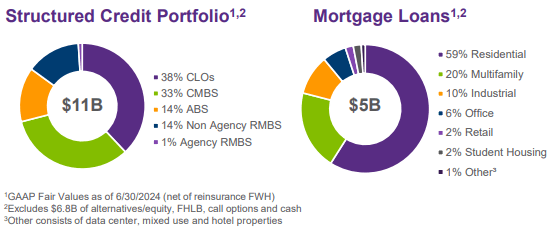

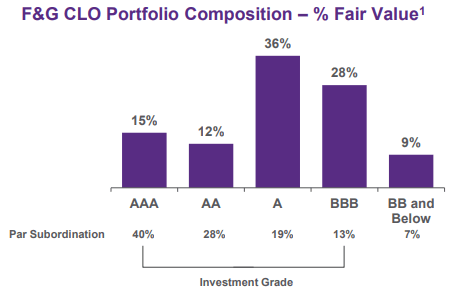

F&G is a “buy and hold” investor, which allows it to stomach illiquidity. Of course, even buy and hold investors face losses if the underlying security defaults. That is why I am comforted by the fact that only 1.8% of the portfolio is in office, the commercial real estate sector with the most pressure. Its CLO exposure is also a source of focus, given these securities are backed by loans to more levered companies, which face greater risk of default in an economic downturn.

This is why it is important to emphasize F&G largely invests high in the CLO capital structure, providing it significant credit protection, a reason why CLOs have historically performed well, even during economic downturns like 2008. For instance, an “A” rated CLO has 19% par subordination. This means the underlying pool of loans could lose 19% on defaults before an A-rated security faces any losses. Beyond par subordination, the underlying portfolio has a higher interest rate than the debt, providing further protection.

F&G

While it has some high-yield CLO exposure, as you can see above, the overwhelming majority of its portfolio is investment grade. On average, there is over 20% subordination. Given losses on loan defaults tend to be less than 50%, there could be a surge of corporate defaults before we see losses on CLO debt. Because it has a large, securitized portfolio, investors will continue to treat F&G with caution during bouts of volatility, but I view its investing program as sound.

During the quarter, it generated a 0.98% return on assets. Excluding the underperformance of alternatives, it generated a 1.3% return on assets, 20bps above target. Indeed, credit losses continue to run below model at about 5bps, supporting extra returns. As you can see, it is earning a 241bp net investment spread.

F&G

Over the coming quarters, I expect to see its cost of funds increase, as it sells more annuities in the current rate world. Even as the Federal Reserve prepares to cut rates, it will be some time before we are back below 3%. However, investment yields are also substantially higher, and so the portfolio yield should continue to rise.

In the coming quarters, I see three items to focus on. First, we will want to see credit losses remain low to validate my view that the structural protections in its securities are sufficient. I believe we would need to see a material economic downturn to inflict significant losses, not just a further slowing. This is not my base case.

Next, it is my expectation that alternative investment returns will remain below long-term averages so long as market volatility persists. While I do not see returns rising back to 10% in the next few quarters, I do expect them to remain positive, likely at 5-8%. Underperformance below this threshold would be an area of concern.

Finally, one negative in the quarter was that it had $16 million of actuarial model update costs. Insurers are always reviewing past policies to see how they are performing vs expectations and occasionally adjust reserves. It is always preferable to see a favorable reserve revision. This adjustment was minor, and its fixed index annuities are relatively simple vs the more complex variable annuities that were frequently sold 10-20 years ago. I have viewed F&G as facing more investment than underwriting risk.

This is a small revision that does not make me yet question that underlying view. However, further negative updates would likely weigh on shares. This environment is likely going to make it difficult for F&G to trade past its $42.52 book value, as there is some uncertainty over market levels on its assets as well as a build in reserves. Importantly, F&G maintains a solid balance sheet. It has a 26.4% debt to capital due to issuing debt to pre-fund a 2025 maturity. Adjusting for this funded maturity, debt to capital is 23.5%, below its 25% target.

In my prior article, I argued F&G could trade to 1.1x book value or $45, which it did reach briefly. Unless we see the market rebound, I do not see F&G recovering all that way. Still, with over $4.10 in earnings power, I do believe shares should trade at book value or about $42.50. That provides about 15% upside, alongside a 2% dividend. While F&G will exhibit a high beta to the market, the underlying risk in its portfolio is more mark-to-market than credit risk. As such, I would use this drop to buy and see shares recovering much of their losses.

Read the full article here

")

")

")

")