")

")

The pressure continues on Fed Chairman Jerome Powell and the Federal Reserve to cut the Fed’s policy rate of interest.

Thursday, the European Central Bank decided to “not” reduce its policy rate of interest. If the Federal Reserve doesn’t lower its policy rate and the ECB lowers its policy rate, this just sets the stage for a rise in the Euro price of one dollar.

The ECB does not want a stronger U.S. dollar.

The U.S, dollar is strong enough as it is.

And, how likely is it for the Federal Reserve to lower its policy rate of interest just before the election date for the U.S. presidency?

In addition, former president Donald Trump has requested that the Federal Reserve not lower its policy rate of interest just before the election.

The Federal Reserve would get a lot of “political” complaints if it moved its policy rate in the very near future.

Yes, some of the Fed’s Governors have been hinting that a change is coming.

But, is this just talk?

Is it all just talk?

Playing off the press…and the investment community…just seems to be a part of the strategy of the Federal Reserve at the present time.

When have you ever heard the Federal Reserve chair and so many members of the Fed’s Board of Governors talk so openly about the possibility of Federal Reserve changes in its policy rate of interest?

And, how does this talk “jive” with what the Federal Reserve is doing with its program of quantitative tightening?

In the latest banking week, ending July 17, 2024, the Fed saw its securities portfolio decline by $14.1 billion. (See the Fed’s H.4.1 statistical release, “Factors Affecting Reserve Balances of Depository Institutions.)

Since the end of June (the final banking week in June ending on June 26), the Fed’s securities portfolio has declined by $30.1 billion.

The pace of this reduction in July has declined from before June as the Federal Reserve has announced that it is reducing the speed at which it is now reducing the size of the securities portfolio.

Still, the Fed’s major policy effort, its quantitative tightening continues.

Note, that since the Fed’s efforts at quantitative tightening began in the middle of March 2022, the Fed’s securities portfolio has declined by $1,728.7 billion or by more than $1.7 trillion. On March 22, 2020, the securities portfolio totaled just under $8.5 trillion.

The commercial banking system has seen its reserve balances…primarily listed as “cash assets” on the Federal Reserve’s H.8 statistical release “Assets and Liabilities of Commercial Banks in the United States…shrink by $571.0 billion since the March 2022 date.

Still, the amount of reserve balances held by commercial banks totaled $3,322.4 billion.

Thus, the Federal Reserve has been tightening up on bank reserves and is continuing to tighten up on bank reserves.

But, what must be realized and accepted, is that the banking system is very flush with funds.

Consequently, the U.S. financial system is very flush with funds.

Note that on January 1, 2020, before the beginning of the economic recession in the United States, the commercial banking system held only $1,548.8 billion in reserve balances.

Note, that this amount was considered by many to be an excessive amount of “excess reserves.”

The point is, the U.S. commercial banking system has lots and lots of “cash on hand.”

And, all this money in the financial system is one of the continuing forces keeping the U.S. economy going.

However, it causes a question to be asked about how many “excess reserves should be present in the current economic and financial environment.

The Federal Reserve has reduced “excess reserves” by $1.7 trillion.

But, the U.S. commercial banking system still has $3.3 trillion in “excess reserves” on its balance sheet.

So, what work does the Federal Reserve still have to do?

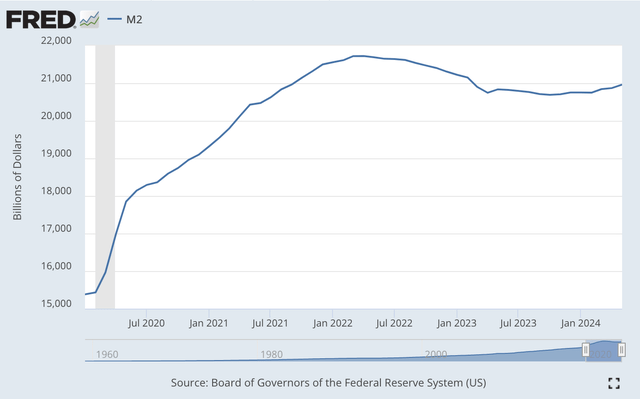

The M2 money stock is still bloated.

Take a look….

M2 Money Stock (Federal Reserve)

In February 2020, the M2 money stock was $15,432.3 billion.

In May 2024, the M2 money stock was $20,963.4 billion.

The increase: 35.8 percent!!!

This is one of the largest increases in the M2 money stock in history!!!

And, there is still money lying di around in the banking system.

Why didn’t inflation take off even faster than it did?

Well, the velocity of the M2 money stock dropped precipitously.

Rather than going into “spending” the money stock pumped into the financial system during this period of time went into assets like stocks, real estate, gold, and other “investment-like” outlets.

Wealth went up, not expenditures on goods and services.

And, this is where we are today.

So, what should the Federal Reserve do?

The Federal Reserve seems to feel a need to continue to reduce the size of its securities portfolio.

Reducing the size of its securities portfolio should reduce the amount of “liquidity” in the financial system…and in the economy.

But, how far should the Federal Reserve go?

Right now, my feeling is that the Federal Reserve would like to continue to reduce the size of its securities portfolio and in so doing, reduce the amount of reserve balances on the balance sheets of commercial banks.

This will be a “touchy-feely” decision.

This is what Chairman Powell and the other Federal Reserve Governors are dealing with right now.

The one thing Mr. Powell does not want to do is to “tighten up” by too much.

He doesn’t want the Fed to create a financial collapse.

Mr. Powell knows that the reserve balances in the commercial banking system must be reduced further for the financial system and the economy to get back into a more stable situation.

But, Mr. Powell doesn’t want to be pushed!

Mr. Powell wants to “continue the tightening” on his own terms.

That is why all the focus is being directed upon whether or not the Fed will lower its policy rate of interest.

So, Mr. Powell wants to keep the guessing going for as long as he can.

When do you think Mr. Powell and the Fed will lower its policy rate of interest?

Read the full article here

")

")