")

")

Federal Reserve Rates – Quick Overview

A couple of months ago I wrote an article analyzing how lower Fed rates should impact different market rates on bonds, loans, and assorted fixed-income securities. With rate cuts imminent, I thought to have another look at these issues.

Some context first.

When the Federal Reserve sets rates, it is setting a specific interest rate, the Federal Funds Rate. Said rate is an overnight bank funding rate but, for the purposes of this article, it might be better to think of it as the risk-free short-term interest rate in the economy.

There are other important interest rates out there, including SOFR, the yield on the 10y treasury, and 30y mortgage rates.

Some of these are functionally equivalent to Fed rates, including t-bill and money market rates.

Some move alongside Fed rates, including those of variable rate treasuries, senior loans, and CLO debt tranches.

Some are impacted by Fed rates, including those of corporate bonds, mortgages, and municipal bonds.

Let’s take a closer look at some rates and investments above.

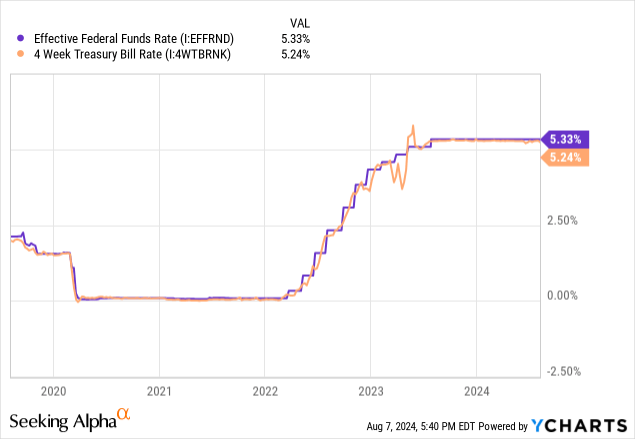

T-bills and Other Ultra Short-Term Investment-Grade Securities

The Federal Funds rate is the risk-free short-term interest rate. T-bills are effectively risk-free short-term securities, so t-bill rates are functionally equivalent to Fed rates. This has been the case these past few years, as expected. Exceptions below were data collection issues, as I recall.

Data by YCharts

Considering the above, t-bill rates should decline as the Fed cuts rates. Declines should be swift and of effectively the same magnitude. As an example, if the Fed cuts rates by 0.50% next month, t-bill rates should decrease by 0.50% next month.

The same should be true of other investment-grade, ultra-short-term securities, including money market funds and the like. The same should be true of the Alpha Architect 1-3 Month Box ETF (BOXX), which achieves similar returns to t-bills through options. Call them synthetic t-bills if you wish.

There should be no significant impact on prices, as there is simply no mechanism for significant price movements to occur. At least not due to Fed rate movements.

Securities with a bit more maturity behave somewhat differently.

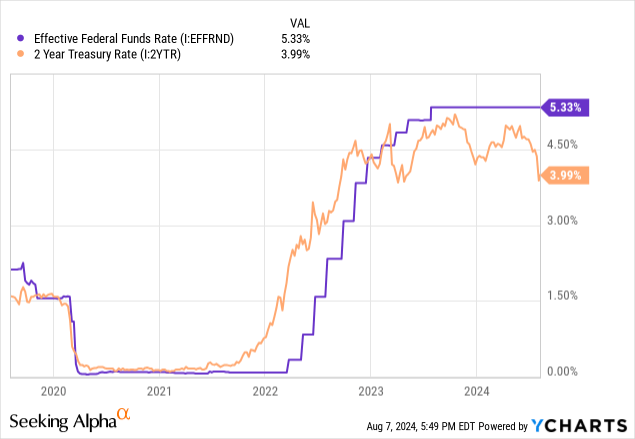

New 2y Treasuries and Other Short-Term Investment-Grade Securities

The Federal Funds rate is an overnight rate. 2y treasuries last for much longer than one night but are still short-term securities, so yields should broadly track Fed rates. This has been the case these past few years, as expected.

Data by YCharts

The relationship above is somewhat indirect, partly caused by the market. Federal Reserve hikes increase t-bill rates, which cause investors to demand higher 2y treasury rates in turn. The Federal Reserve does influence treasury rates through QE and other programs, but rates are not directly set by the Fed, nor does it target a specific range. The same is true for longer-term treasuries and for most other fixed-income asset classes. These are market rates of interest, influenced by the Fed, but not set by it.

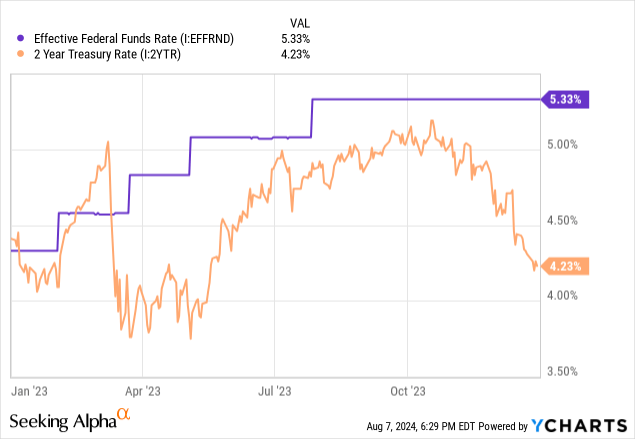

Due to the above, 2y treasury rates are impacted by market forces, including investor demand, sentiment, and expectations, including future Fed policy. As an example, 2y treasury rates started to go up by late 2021, months before the Fed hiked, as the market expected the Fed to hike in the near future, and priced 2y treasury accordingly.

Market forces might cause 2y treasury rates to move opposite Fed rates, but this should be a somewhat rare occurrence. As an example, 2y treasury rates slightly declined during 2023, even as the Fed hiked rates a couple of times.

Data by YCharts

2y treasury yields are impacted by market forces, and the market is sometimes irrational and sometimes gets things wrong. In hindsight, focusing on t-bills in early 2023 was the better call, with the market pricing 2y treasuries at lower, unattractive rates.

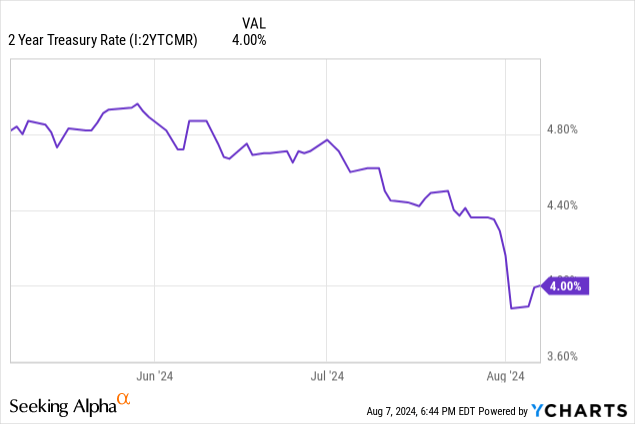

Notwithstanding the above, 2y treasury rates should decline as the Fed cuts rates. This is the most common, expected scenario, with exceptions few and far between. Due to expectations, the decline should start a couple of months before the Fed starts to cut, as has been the case.

Data by YCharts

Other short-term, investment-grade securities should behave as 2y treasuries.

Old 2y Treasuries and Other Short-Term Investment-Grade Securities

Significant rate cuts would cause the rate on newly issued 2y treasuries to plummet. Older, existing treasuries would retain their original rates, currently at 4.0%. Significant rate cuts would, therefore, lead to increased demand for older, existing 2y treasuries, boosting their price.

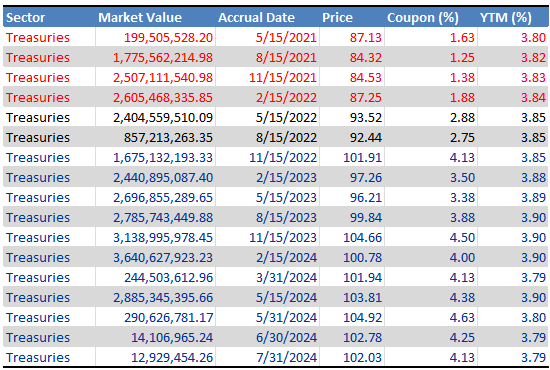

It is impossible for me to show an example of the above using 2y treasuries, as these are all invariably ‘old’ by now, being issued after the Fed started to hike. One can see this in the portfolio of the iShares 7-10 Year Treasury Bond ETF (IEF), which focuses on medium-term treasuries. Older treasuries, before Fed hikes, have low prices. Newer treasuries, issued after several rounds of hikes, have high coupons. Treasuries in the middle are somewhere in between. Table color-coded for your convenience.

IEF – Table by Author

Another interpretation of the above is that changes in Federal Reserve rates should change the expected returns of holding treasuries. For newer treasuries, expected returns change through coupon rates moving. For older treasuries, their coupons are fixed, so any change in expected returns must come from changes in prices.

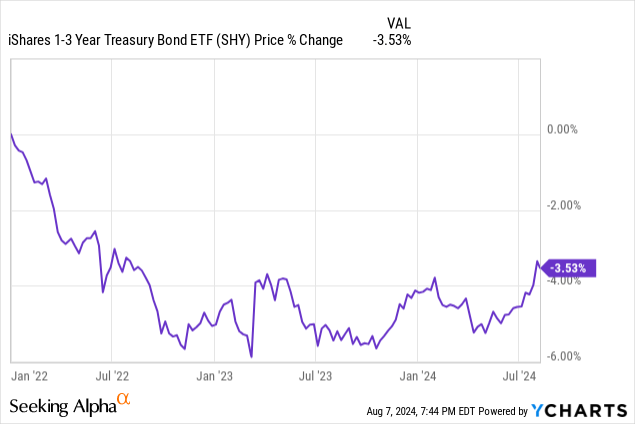

At first, bond funds see declining share prices from Federal Reserve hikes. Short-term treasury ETF share prices are down 3.5% since early 2022, for instance.

Data by YCharts

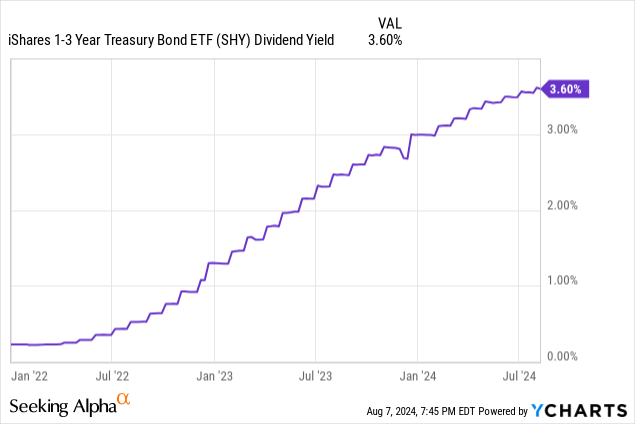

In time, older, lower-yielding treasuries mature and are replaced by newly issued, higher-yielding alternatives, resulting in higher dividend yields.

Data by YCharts

Rate cuts should have the opposite impact, leading to short-term price gains, and long-term dividend cuts.

Due to the vagaries of ETF distribution requirements and portfolio turnover, the above might impact share prices a bit less than expected, but the net effect should be the same.

Other short-term, investment-grade ETFs should behave as 2y treasuries.

One can quantify the impact interest rate movements should have on bond prices through duration. As interest rates on 2y treasuries, and most other bonds for that matter, are impacted by market forces, duration does not tell us how Federal Reserve policy impacts prices, however, at least not exactly.

New 10y Treasuries and Other Medium-Term Investment-Grade securities

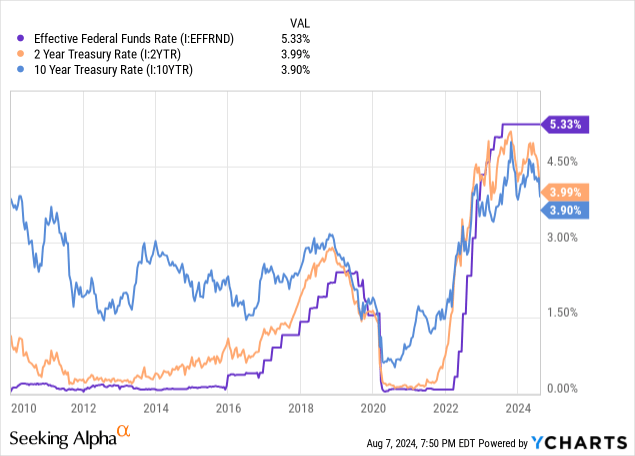

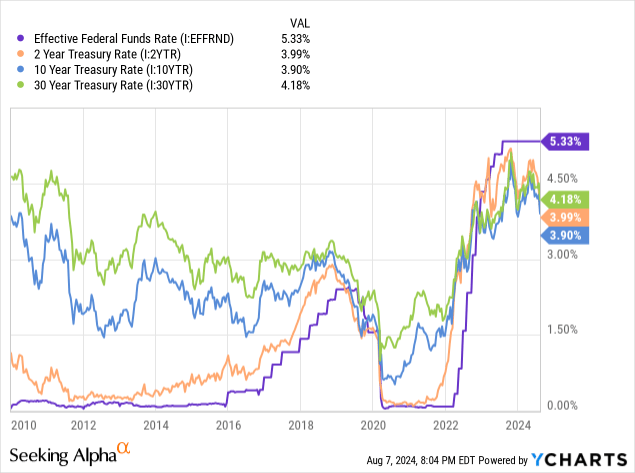

Once maturities go up, the link between Fed rates and market rates becomes more tenuous and more volatile. As an example, compare 2y and 10y treasury yields with Fed funds rates since early 2010.

Data by YCharts

As can be seen above, 2y treasuries consistently trade alongside Fed rates, with a bit of volatility. 10y treasuries tend to do so too, but the relationship is much more tenuous and volatile. Sometimes other factors dominate, as occurred from 2010 to 2016.

Considering the above, rates on newly issued 10y treasuries should decline as the Fed cuts rates, but much will depend on the specifics of future Fed policy, investor expectations, and sentiment. Rates might not necessarily decline, and the timing might be very different. These caveats do not apply to t-bills and similar investments and are of much less importance for short-term treasuries.

Everything here should apply to similar securities or funds to 10y treasuries, including the Vanguard Total Bond Market Index Fund ETF Shares (BND), and the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD).

Old 10y Treasuries and Other Medium-Term Investment-Grade securities

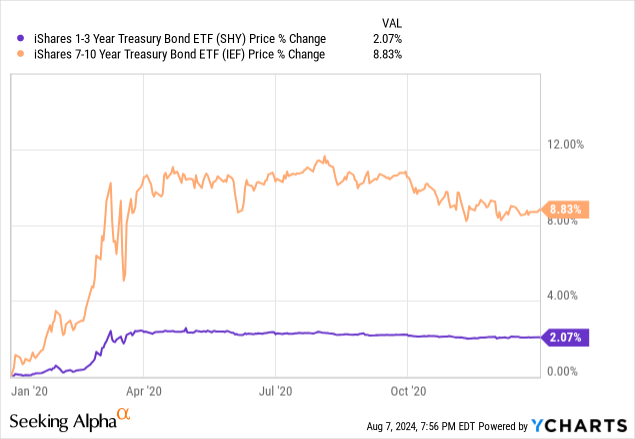

As with 2y treasuries, significant rate cuts would cause the rate on newly issued 10y treasuries to plummet, while older 10y treasuries would retain their existing higher rates. Investor demand for these older treasuries should increase, boosting their price. The impact would be greater than for shorter-term treasuries, as investors would be lock-in higher rates for longer / due to their greater duration.

As an example, medium-term treasury ETF share prices increased by 8.8% during 2020, compared to 2.1% for shorter-term treasury ETFs.

Data by YCharts

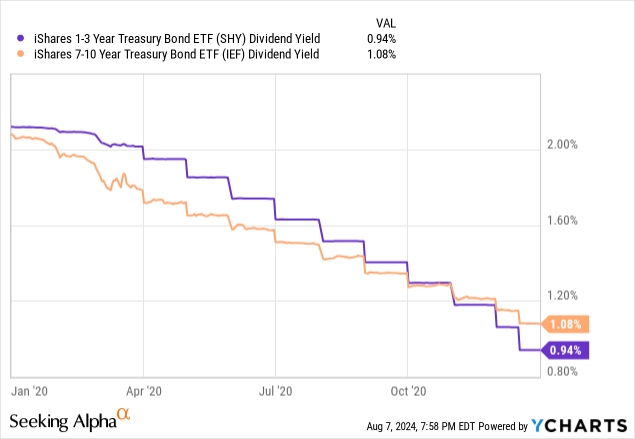

Dividends should decrease too, albeit more slowly, as it would take longer for these higher-maturity treasuries to mature. IEF’s dividend yield declined by 1.0% during 2020, compared to 1.2% for SHY. The gap is wider than implied in these figures, as IEF’s higher share price was also partly responsible for its lower yield.

Data by YCharts

Medium-term treasuries could, potentially, see higher capital gains from Federal Reserve cuts, and would take longer for their dividends to decline. For dovish investors, these seem stronger investments than shorter-term treasuries.

In my opinion, current Fed guidance should not necessarily result in significantly lower 10y treasury rates/higher prices. More dovish investors might disagree.

Everything here applies to similar securities to 10y treasuries too.

30y Treasuries and Long-Term Investment-Grade Securities

For very long-term securities, the link between Fed rates and market rates becomes even more tenuous. 30y treasuries seem less connected than 10y treasuries to Fed rates, for instance, although not significantly so.

Data by YCharts

Considering the above, long-term investment-grade yields should move alongside those of medium-term securities, but with greater volatility. Capital gains would, potentially, be higher. For dovish investors, longer-term treasuries have the highest potential returns, although risks are higher too.

Very long-term investment-grade corporate bonds should perform similarly to 30y treasuries. Can’t say I cover many of these, but you do have the Vanguard Long-Term Corporate Bond Index Fund ETF Shares (VCLT).

Non-Investment Grade Fixed-Rate Securities

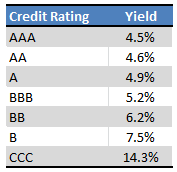

The Federal Funds rate is an (effectively) risk-free rate. Most bonds are not risk-free, with most having at least some credit risk. Higher credit risk means higher yields, for obvious reasons. As an example, compare effective yields for fixed-rate corporate bonds of different credit ratings.

Seeking Alpha – Table by Author

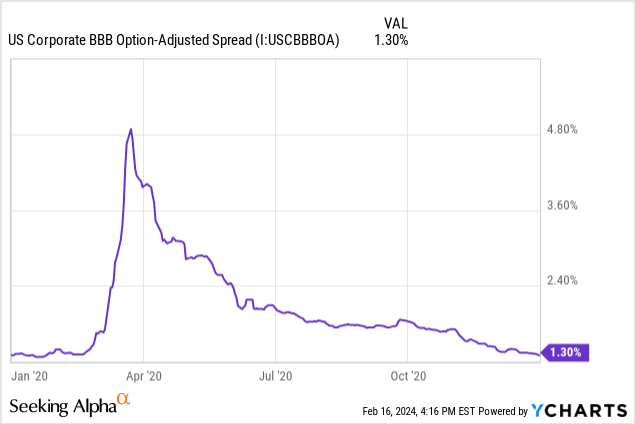

Spreads also vary, with most investors demanding even higher yields during downturns and recessions, due to fears of default. As an example, spreads for BBB-rated bonds spiked from around 1.5% to 4.8% during early 2020, the onset of the coronavirus pandemic. BBB-rated bonds are investment-grade, too, but investors were very worried during the pandemic and sold off everything with even a hint of risk.

Data by YCharts

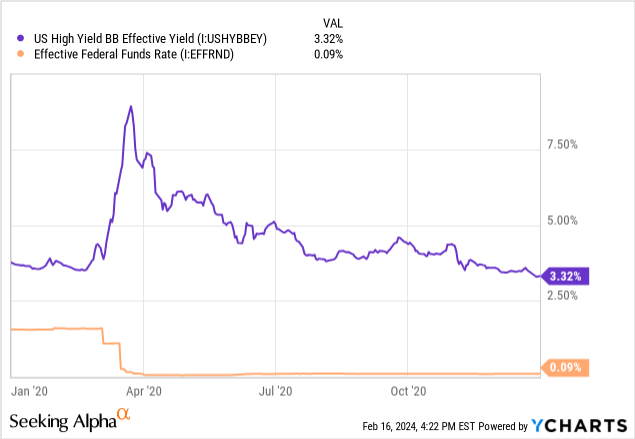

During particularly severe downturns, non-investment grade bond yields could move in the opposite direction from Fed rates, due to wider credit spreads. As an example, during early 2020 BB-rated bonds saw their yields skyrocket despite significant Fed rate cuts. By the end of the year, they were yielding marginally lower, however.

Data by YCharts

Because the Federal Reserve tends to cut rates during recessions, one should not generally expect riskier high-yield bonds to see lower rates / higher prices when the Fed cuts. In most cases, the negative impact of the recession should outweigh Fed policy. Higher-quality investment-grade bonds should increase in price, though.

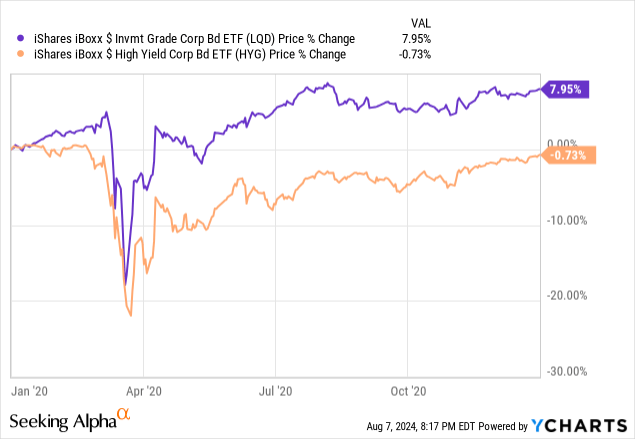

As an example, benchmark high-yield bond ETFs saw their share prices decline 0.7% during 2020. Federal Reserve cuts almost cancelled out higher spreads due to deteriorating economic conditions, but not quite. Benchmark investment-grade bond ETFs saw their share prices increase by 8.0%, in line with expectations.

Data by YCharts

Right now, Fed cuts would occur due to interest rates normalizing after a period of high inflation. Under these conditions, lower rates for riskier, higher-yield bonds seem more likely. As with treasuries, much will depend on the specifics of future Fed policy, investor expectations and sentiment, and broader economic conditions.

Credit spreads are more impactful for riskier, higher-yield bonds compared to higher-quality bonds. Credit spreads have outweighed Fed cuts for riskier bonds in the past, and that could be the same moving forward.

Variable Rate Bonds and Loans

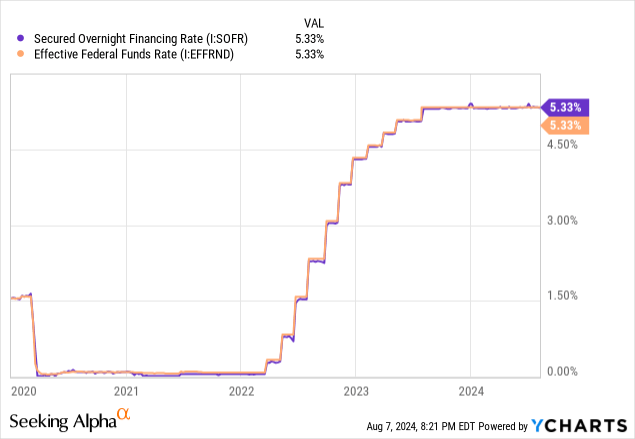

Some bonds and loans have variable rates, in which coupon rates are directly tied to specific benchmark rates. As an example, we have variable rate treasuries, senior loans, and CLO debt tranches. SOFR is the most common benchmark rate, which is effectively identical to the Fed funds rate.

Data by YCharts

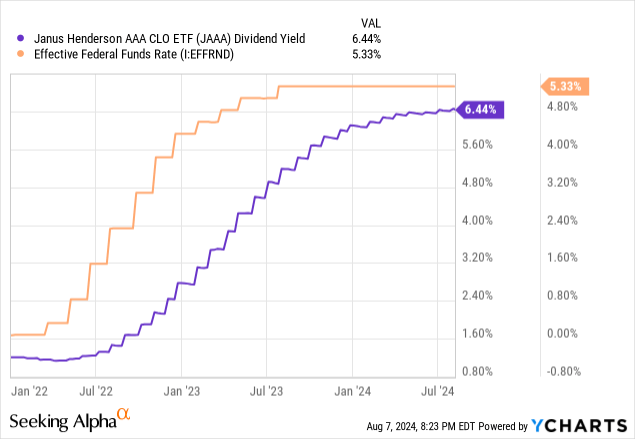

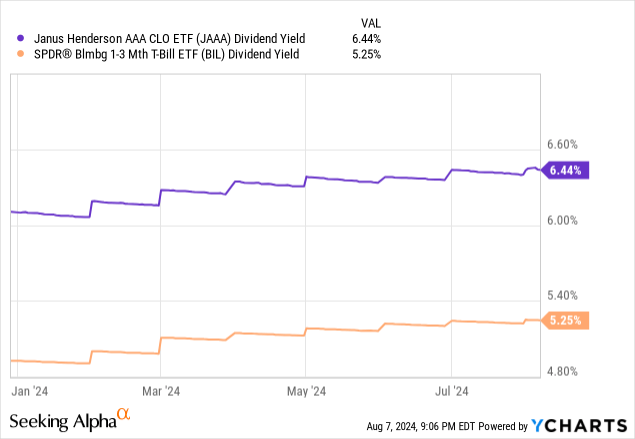

Considering the above, yields on variable rates bonds and loans should decline as the Fed cuts rates. Declines should be swift and of similar magnitude. As an example, compare the dividend yield of the Janus Henderson AAA CLO ETF (JAAA) with Fed rates. Dividend yields clearly move alongside Fed rates, with both following a straightforward stepwise function. Since early 2022, JAAA’s yield has increased by 5.2%, in line with Federal Reserve hikes.

Data by YCharts

Moving forward, the dividend yield on JAAA should decrease by the same magnitude that the Fed cuts. Fed cuts of 3.0% mean dividend yield decreases by 3.0%. The same is true of other variable rate investments and funds.

Some variable rate securities have credit risk, and so are impacted by the issues mentioned in the prior section (credit spreads widening during downturns and recessions). These issues could, potentially, outweigh Fed policy, but I find that extremely unlikely, especially in the short term. For these securities, Fed rates have a direct, swift impact. Credit spreads matter too, but the impact is more indirect, dependent on the market, and sometimes slower. I can’t really see credit spreads outweighing the Fed in the vast majority of cases.

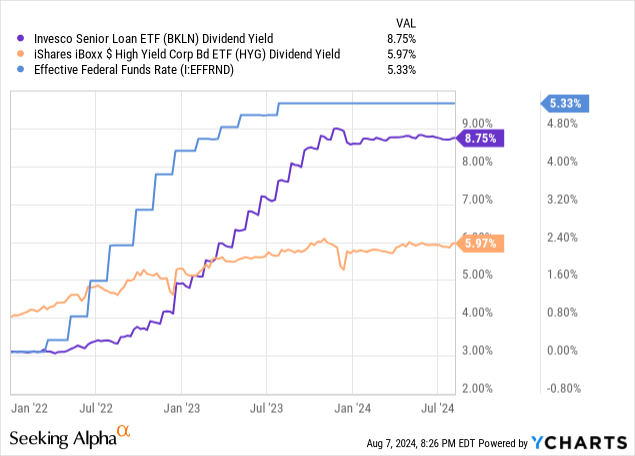

As an example, compare the dividend yield on senior loan funds versus high-yield funds since early 2022. Senior loans quite clearly move in line with Fed rates, much more tightly than high-yield bonds. There is some volatility, but not enough to really break the relationship.

Data by YCharts

To give some more figures on the above, senior loan yields have declined by around 0.25% since late 2023, even though the Fed has not cut rates since then. Small movements like these are quite common and can grow in size long-term. In theory, these movements could outweigh the Fed. In practice, I don’t see how they could. Perhaps if the Fed cuts rates by only 0.10%, but 0.25% movements are standard.

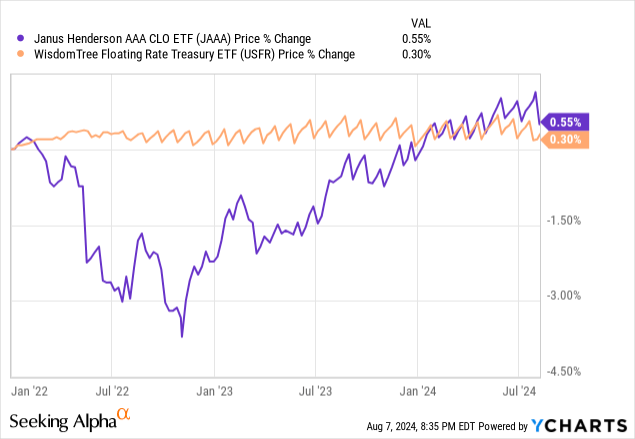

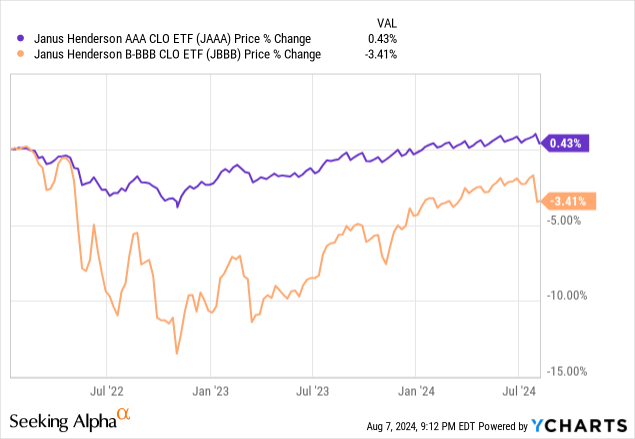

Rates on both newly issued and older variable rate investments move alongside Fed rates, which means no shift in investor demand or prices. As an example, share prices for AAA-rated CLOs and variable rate treasuries have been flat since early 2022. Fed hikes had no impact on these securities in the past, cuts should have no impact in the future either.

Data by YCharts

Let’s take another short look at IEF’s treasury holdings:

IEF – Table by Author

As mentioned previously, the Federal Reserve hike led to higher coupon rates on newer treasuries and lower prices on older ones. For variable rate investments, both newer and older securities would see higher coupon rates from Fed hikes, with no impact on prices.

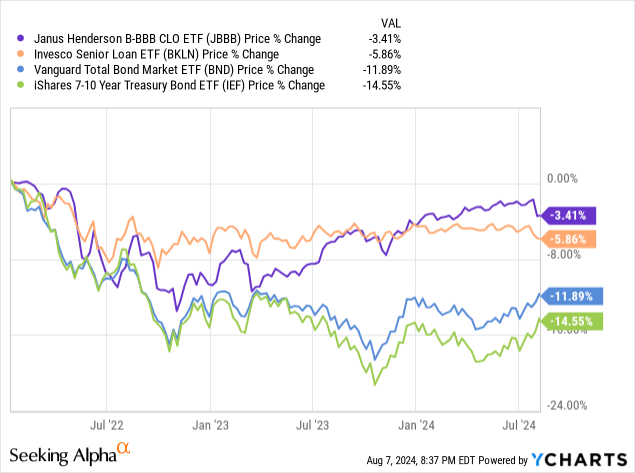

Prices on riskier variable rate investments might move because of changes in credit spreads, which might coincide with Federal Reserve hikes or cuts. As an example, both BBB-rated CLOs and senior loans have seen their prices drop since early 2022. Prices dropped because economic conditions deteriorated, not directly because of Fed hikes. Prices dropped by much less than average, too, consistent with this.

Data by YCharts

Riskier variable rate investments should see their share prices drop in the coming years if economic conditions worsen and spreads widen. These losses might coincide with Federal Reserve cuts but would not be caused by these. The distinction matters, although obviously economic conditions are intertwined with Fed rates.

Simplifying things a bit, I think soft landing means stable share prices and hard landing means lower share prices. The Fed might cut more during a hard landing, but that doesn’t mean these are equivalent scenarios. Another bout of inflation should lead to lower CLO prices and Fed hikes, the same as 2022. Broader economic conditions are what matter, the Fed less so.

What About CLOs?

I’ve gotten dozens of questions about CLO share prices and Federal Reserve cuts. Although rarely explicitly stated, I think lots of investors believe that Fed cuts should lead to CLO dividend cuts, decreasing investor demand for these investments, and ultimately resulting in lower share prices. I do not believe that significant capital losses are likely, for several reasons.

First, is the simple fact that CLOs and variable rate investments are simply not structured for that to happen. CLOs see stable share prices as interest rates move, in theory, and (mostly) in practice.

Second, capital losses imply wider credit spreads, which might coincide with Federal Reserve cuts, but would not be caused by these. As an example, JAAA trades with a 1.20% spread to t-bills right now.

Data by YCharts

Federal Reserve cuts would lead to reduced yields on both JAAA and t-bills, with spreads remaining the same. JAAA’s share price decreasing implies dividend yields increasing and spreads widening, which are not a direct, necessary result of Fed cuts. Spreads could widen as the Fed cuts rates, especially if the economy worsens, but these are genuinely different phenomena.

The same is true of riskier CLOs and variable rate investments, although the comparisons are much harder to do. Lots of differences between securities, more factors to consider, and higher volatility.

Third, prior interest rate hikes did not lead to higher CLO prices, with these seeing small price declines as economic conditions worsened. If the past is any indication, future Fed cuts should lead to higher CLO prices. I don’t think this is terribly likely, but that is the precedent we have.

Data by YCharts

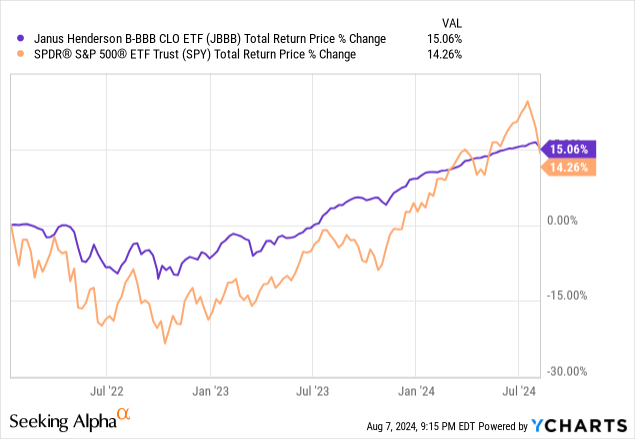

As an aside, I’ve become a bit more partial to the idea of CLOs (slightly) declining in price as the Fed cuts. I think if you told investors that BBB-rated CLOs would outperform the S&P 500 since early 2022 CLO prices would have increased.

Data by YCharts

Steven Bavaria and I were bullish on CLO ETFs back in 2023, and interest rates played a role in that (for me at least). If we were, 1000x more influential, we could have perhaps moved the market. Other investors could have come to the same conclusion as us too, perhaps enough investors to move the market.

Still, I don’t expect CLO share prices to decline as the Fed cuts rates, for the reasons stated previously. Perhaps a small movement is possible. Wider credit spreads would definitely cause a larger movement, but that is, again, a different phenomenon. Dividends will decrease, though, and longer-term treasuries might see higher gains. Dovish investors might wish to avoid CLOs for these reasons, even though share prices should not decline.

Conclusion

Federal Reserve cuts will likely lead to lower interest rates across bonds and fixed-income assets. Different bonds will react differently, with shorter-term, investment-grade bonds being more impacted than longer-term and non-investment-grade bonds.

Read the full article here

")

")