")

")

Introduction

Self-storage REITs have been in a bit pause due to the concerns of oversupply and rate-drop from “a substantial slowdown after the higher rates experienced at the height of the pandemic and its aftermath, when demand pushed rates higher than usual.” On the other hand, these REITs have demonstrated the most impressive dividend growth for last 3 years, indicating the industry has survived the “slowdown”, as the last 3 years should be the most effected times. In particular, Extra Space Storage Inc(NYSE:EXR) has grown a dividend growth with the fastest rate over the last 3 years within the storage group. The most recent Q2 earning report has shown EXR’s ability to maintain the high occupancy at its 1800+ stores. The size advantage and growth potential make EXR well positioned for the REIT recovery going forward. I recommend a BUY for EXR.

REIT Overview

EXR is a national wide storage operator in US, that

owns and/or operates over 3,500 self storage properties in 43 states, and Washington, D.C. The Company’s stores comprise approximately 2.5 million storage units and over 280 million square feet of rentable space

The key business focus is on the location convenience and the affordability. It is one of the largest storage operators in the United States with 1,895 stores under its management, according to its Q2 report.

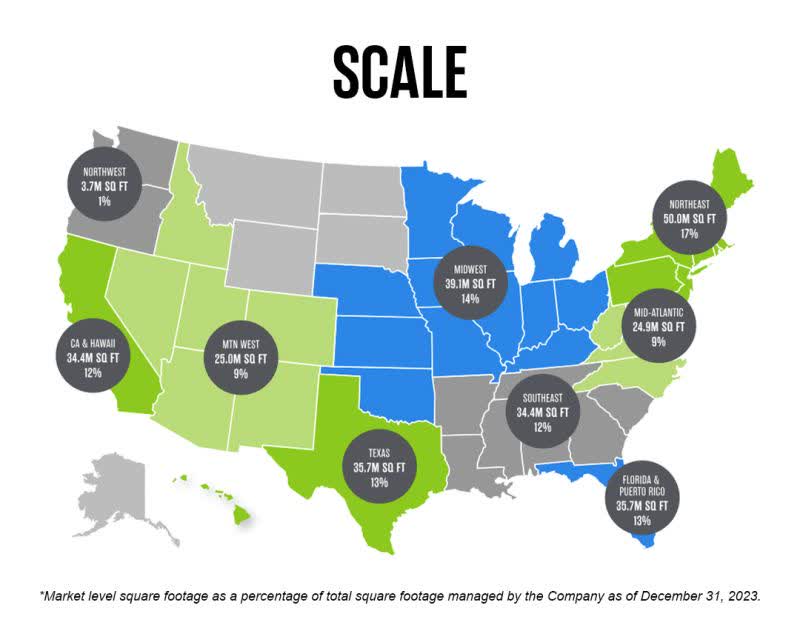

The following shows the storage geolocation distribution and scales (Note the exact numbers need to be updated):

EXR Coverage Scale – from LinkedIn post

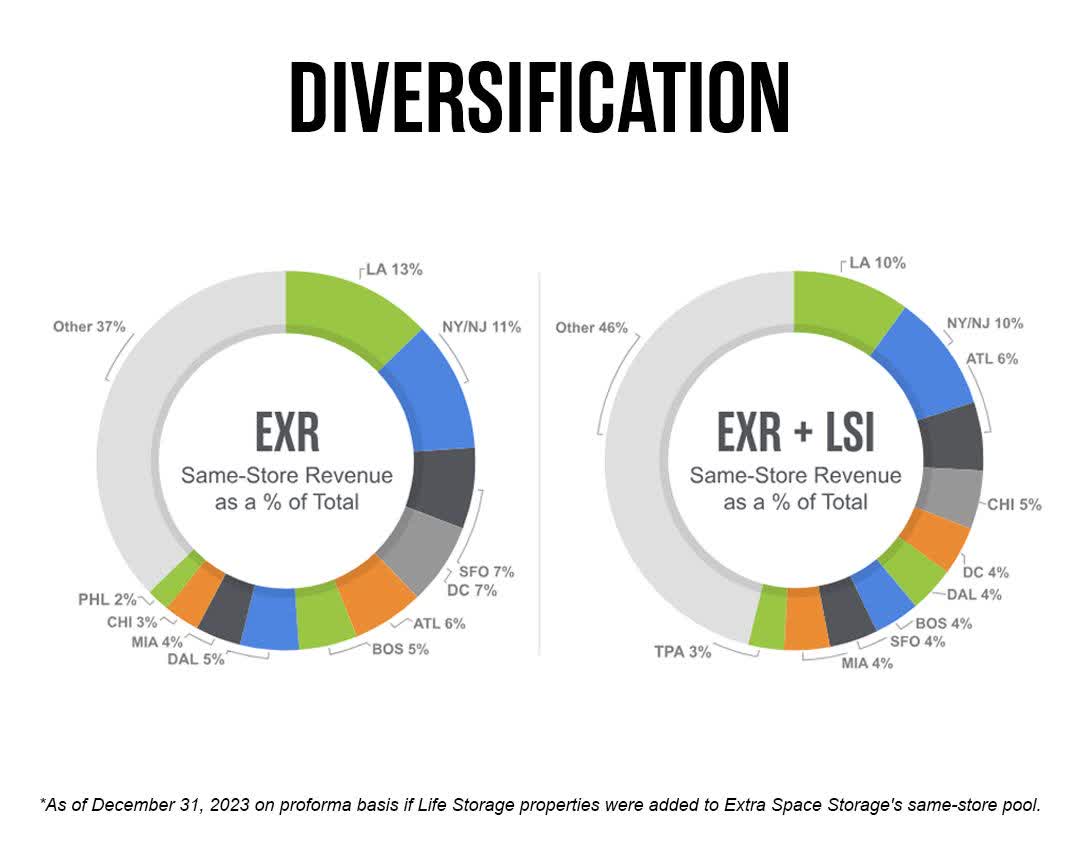

The asset portfolio is also very diversified. The merge of Life storage helps boost its coverage as shown below:

EXR Diversification from LinkedIn post

The following highlights some key market characteristics of EXR:

- Market Cap: $36.14B.

- Volume (last day): 1,142,099

- Yield (FWD): 3.95%

- Payout Ratio: 81.23%

- Dividend Growth (3-year): 19.74%.

- Price/FFO (FWD): 20.39. The value is on the high side, reflecting the premium for its growth prosperity.

- Revenue Growth (yoy): 20.53%. The double g

- Institutional Ownership: 98.71%.

- Wise Edge Analysis: EXR is a growth leader of the self-storage group. It is a dividend grower, that is attractive to investors focusing on the total return.

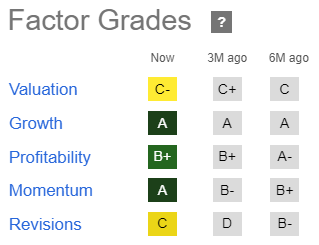

EXR growth is the most promising with a double-digit growth rate 20.53%. It has A grade on its growth as shown below.

EXR Factor Grades – from SA

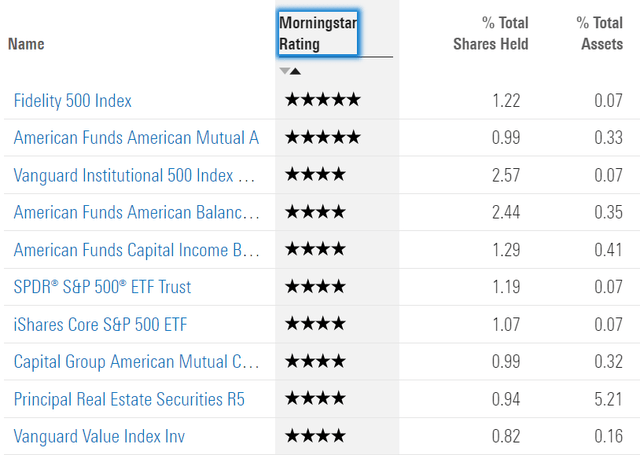

Notice that the institutional ownership is 98.71%, so mostly owned by the funds, index ETFs, etc. Many of them have very impressive quality ratings by morningstr.com as shown below:

EXR Holders Ratings – from morningstar.com

In next section, I will use company’s Q2 report to provide some specific data.

EXR Q2 Report shows solid financial results.

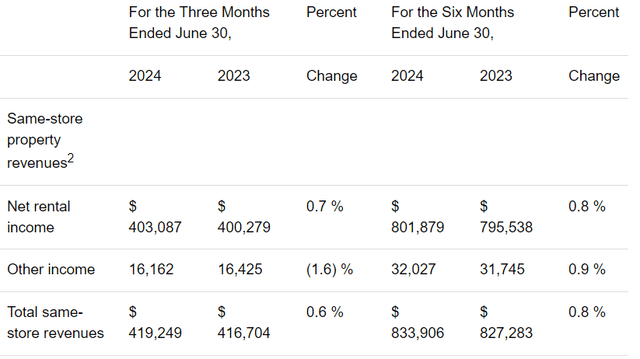

EXR reported Q2 results on July 30, 2024. The following shows the growth in both same-store revenues (0.6%) and rental income (0.7%). The increases are smaller compared to Q1, but it has no sign of “a substantial slowdown” as many concerned since early 2024. I view them very solid growth given the high rate environment.

EXR Q2 Revenue and Income – from SA report

Perhaps the most important metric is same-store occupancy, which stays at high 94.3%, and it is just edged a bit higher than 94.0% achieved one year ago. The Core FFO ($2.06) is the same as last Q but the Achieved FFO is lower at $1.98. I believe this provides a strong evidence that the merge integration seems to work fine and it is expected to contribute more positively to the future operations. In fact the CEO of the company clearly indicated

We’ve maintained strong occupancy levels in the Extra Space and Life Storage same-store pools despite a challenging demand and new customer rate environment. The occupancy gains drove positive revenue growth in both pools. In addition, we continue to realize G&A savings and stronger than expected tenant insurance income, supporting solid FFO per share performance ahead of our projections.

Strong Dividend Growth reveals a promising future.

When I am looking at REITs, I pay a special attention to how they have done during the very tough 5 years, when the sector has been hit very hard by Covid19, FED rate hikes, office debt maturity walls, and “Higher for longer”. More specifically, I have reasons to believe if the REIT can raise dividends and demonstrate a healthy dividend growth in the last 3 years, they have proven themself to be strong survivors and more importantly winners in the REIT recovery. They deserve a place in my watch list of long holdings (potential buys).

The following is a list of self-storage REITs sorted on the dividend growth in the last three 3 years.

Dividend Information for Self Storage REITs – from SA

I use the dividend growth as a “NorthStar” indicator for the quality of the underlying operations. The REIT stocks listed above are among the ones with the best dividend growth. I have a buy rating on EXR, which has the biggest dividend growth metric.

The next is a summary of the other three. It is provided here to share more insights about self-storage REITs.

NSA National Storage Affiliates Trust

- Market Cap: $4.91B.

- Volume(last day): 758,012

- Yield (FWD) 5.14%

- Payout Ratio: 90.36%

- Dividend Growth (3-year) : 16.41%.

- Price/FFO (FWD): 18.22

- Revenue Growth (yoy): 2.43%. It is below sector average 4.56%.

- Institutional Ownership: 90.99%.

- Wise Edge Analysis: NSA is of the smallest size in the group. The dividend payout is over 90% which is a risk for dividend growth. The year-over-year growth is small at only about a half of the sector average.

PSA Public Storage

- Market Cap: $53.36B. PSA is blue-chip storage REIT. One of the largest.

- Volume (last day): 536,289. Trading volume is the lowest in the group.

- Yield (FWD): 3.96%

- Payout Ratio: 72.52%

- Dividend Growth (3-year): 14.47%. It has the least consistent div growth in the group.

- Price/FFO (FWD): 17.90

- Revenue Growth (yoy): 6.02%. Solid above 4.56% (sector)

- Institutional Ownership: 80.34%.

- Wise Edge Analysis: PSA is the largest storage REIT and the main competitor of EXR. PSA has relatively less conviction among the institutions based on the ownership percentage (80%), which is smallest of the four (over 90%). However in June, the company announced repurchasing shares worth $200 million, which has shown the management team’s confidence in PSA’s future.

CUBE CubeSmart

- Market Cap $10.91B

- Volume (last day): 1,447,891. The trading volume shows relatively high market interests.

- Yield (FWD): 4.23%

- Payout Ratio: 77.71%

- Dividend Growth (3-year) 14.38%.

- Price/FFO (FWD): 18.22

- Revenue Growth (yoy): 2.77% . It is below sector average 4.56%.

- Institutional Ownership: 97.67%.

- Wise Edge Analysis: CUBE is a key player. The revenue growth is a concern at the moment.

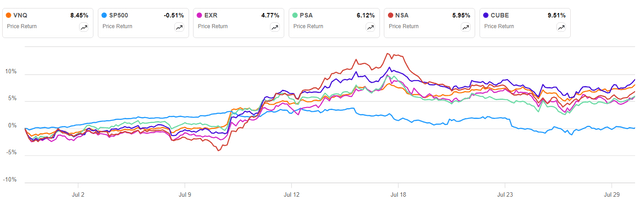

REITs are generally very sensitive to interest rates. The whole sector is on a rally since the time when the FED rate cuts became more certain and the cooling economic data started to flow out. Storage REITs have been part of rally but losing a bit momentum as of late, as shown below.

One Month Price Chart – from SA

Note that the chart uses just past month to emphasize on the recently rally. The self-storage REITs are actually a bit expensive compared to some of the other REIT segments. On the other hand, I think that EXR is expected to have faster growth, which will make its valuation look relatively more reasonable.

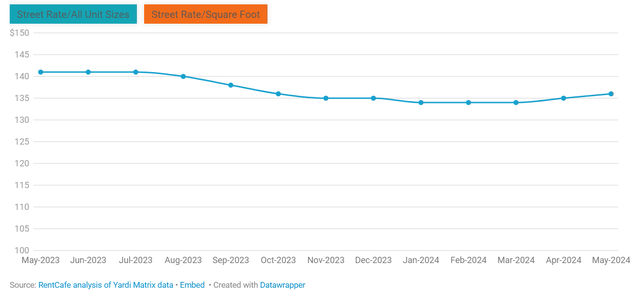

The street rates seem to find a bottom 2 months ago after ending 20-month consecutive rent decreases for self storage, according the following chart.

Average Self Storage Street Rates – from rentcafe.com

If the curve will continue to move up from here, indicating the market is going back to pre-pandemic levels. It would be very bullish to the self-storage business, and therefore very promising to the self-storage REIT stock market.

Closing Thoughts

FED’s rate cut could be a key catalyst in the near term. I expect the current REIT rally to continue and the self-storage segment should also resume its recovery journey. EXR is a solid long term play with its better growth outlook and excellent track record of dividend growth. In the short term, the US economy will play a vital role in affecting the rental and “street rates”. The bearish sentiment (recession) could put the rally to an end very quickly. This is something REIT investors should keep a high alert on.

Read the full article here

")