")

")

")

")

According to Grand View Research, the global market of video games around the world is projected to have a growth rate of CAGR of 13% from 2023 to 2030, making it a market that should not only experience more demand and a larger player base but also be driven by the development of new technologies. This, together with the fact that it is very present in the lives of many, is attracting the attention of some investors who want to invest in this sub-segment.

It’s a very appealing industry, but it’s not trivial to analyze it. In a superficial analysis of the best-known (and listed) players, such as Electronic Arts (EA), Nintendo (OTCPK:NTDOY), Take-Two Interactive (TTWO), and Ubisoft (OTCPK:UBSFY), Ubisoft is definitely the cheapest (which is why it attracts attention), yet it still has well-known IPs such as Assassin’s Creed and others.

A catalyst for Ubisoft’s valuation to become even more detached from its peers was the ~48.5% drop in Year to Date, with the highlight being the more than 20% drop that has been taking place over the last 5 days, following pressure on management and weak game sales.

The thing is, there are important reasons why Ubisoft is trading at such an undervaluation, such as the uncertainty about its future, brought about by some failures, as well as titles that are often considered ‘average’ by players, which end up reflecting in its moats (or lack thereof) and in the forecast of its fundamentals.

Challenges May Arise For Ubisoft’s Franchises

Ubisoft has IPs that are important to the history of the games’ industry, such as the Assassin’s Creed franchise, the Far Cry franchise, and the Tom Clancy’s franchise. In some franchises like Far Cry, as new titles kept being released, the company has exploited a very similar (not to say repeated) formula, leading to a feeling of deteriorating quality, since there have been few innovations in the opinion of many. This is reflected in the user reviews, for example, while Far Cry 3 (a 2012 game) has a user score of 8.4 on Metacritic, the most recent game, Far Cry 6 has a 5.3 score.

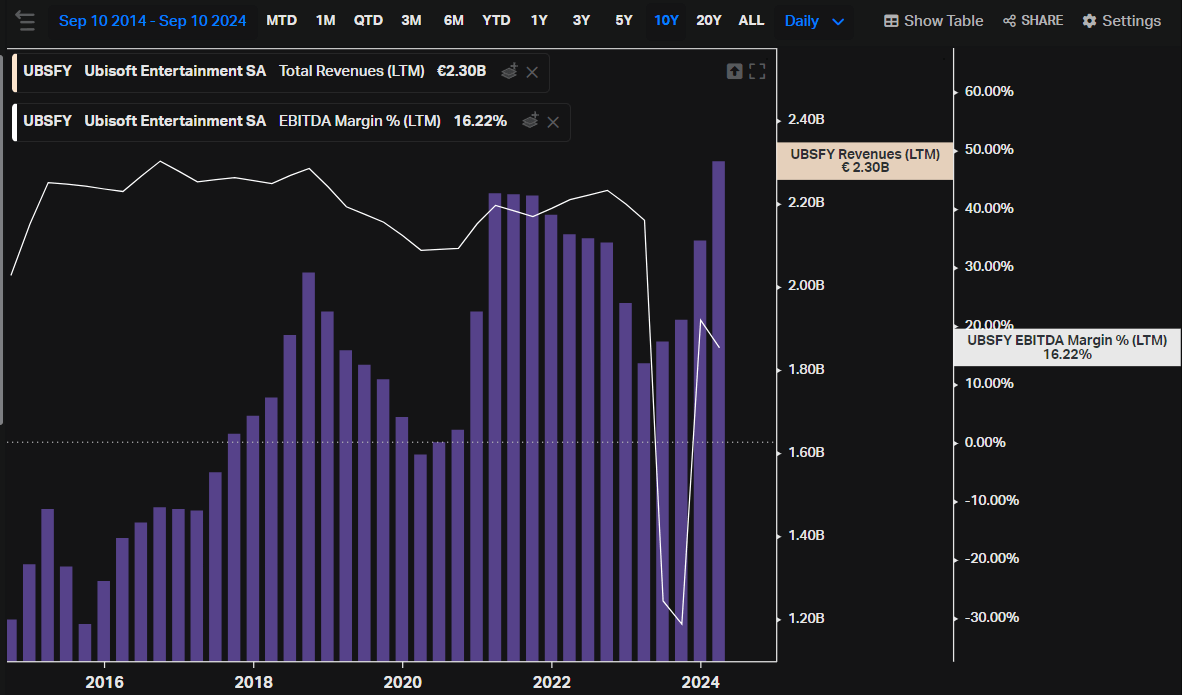

With the Assassin’s Creed franchise, the company has managed to reinvent and win over part of the public, keeping it more relevant. Despite this, there was still a certain amount of slippage, with the bestseller being Assassin’s Creed IV, released in 2013, selling 15 million against something close to 10 million for Odyssey and Origins, which are more recent titles. It’s worth mentioning that the information on the most recent titles isn’t that reliable, and there’s no way of knowing exactly according to the source itself. Even with the emphasis on an old game, Assassin’s Creed Valhalla exceeded $1bn in revenue and must have exceeded 40% of Ubisoft’s earnings across the 13 months after the game’s release. It’s worth noting that in LTM Ubisoft’s revenue was €2.3bn, so to have a game that exceeds $1bn is quite something.

Counterbalancing these periodic releases, the company also has other sources of income with a more recurring or “Games-as-a-Service”, nature, which was what drove the growth in Q1, with Rainbow Six Siege and The Crew standing out, along with higher sales of the Assassin’s Creed franchise. In the company’s own words, for Full-year 2024-25, “It expects solid net bookings’ growth, a slight increase in non-IFRS operating income and growing non-IFRS Cash Flow from Operations leading to positive Free Cash Flow.”. These assumptions are also based on the launch of the new Assassin’s Creed (Shadows) due out on November 15 and Star Wars Outlaws which launched on August 30. The latter disappointed investors with lower-than-expected sales, some bug problems at launch, and the like. XDefiant is also in this boat, showing drops in views on Twitch.

This is Ubisoft’s main problem: although the company has managed to maintain growing revenues and reasonable margins over a long period of time, you have to have a lot of confidence that management will be able to maintain successful launches, and that’s not always the base scenario.

Koyfin

Even though Assassin’s Creed Shadows could still be a positive surprise, Star Wars Outlaws has already flopped, and making good games that take time to win back the confidence of players and investors is no trivial matter either. This business model is very different from that of Nintendo, which manages to maintain a more constant rhythm of profitable first-party game releases, as well as earning from console sales and other things. It’s also different from Take-Two Interactive, since the whole market gives it the benefit of the doubt and believes that GTA VI will be a big thing.

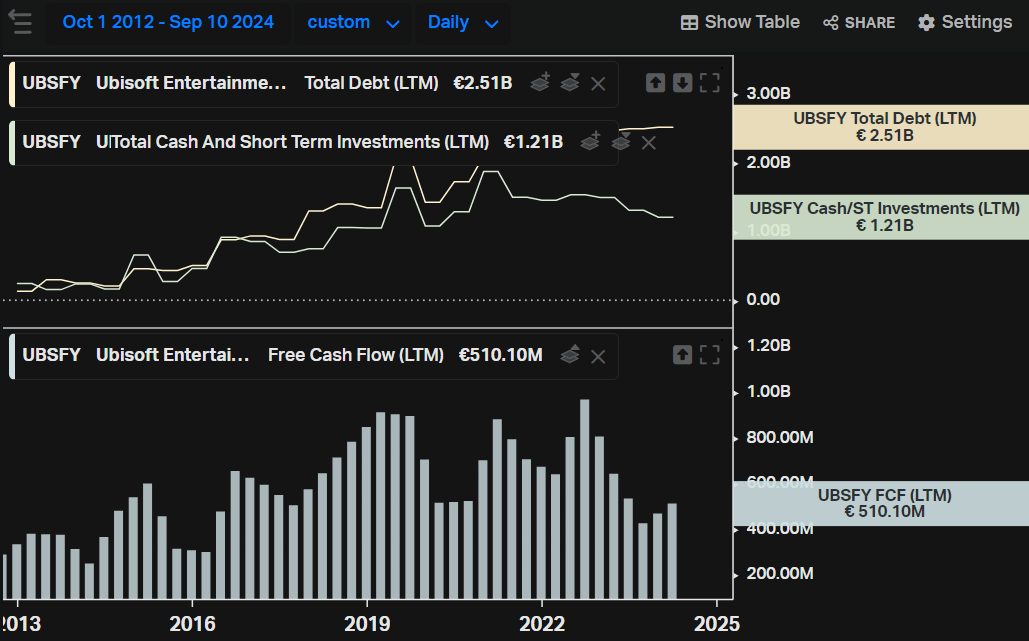

Unlike what is almost suggested by its valuation, the company is not close to bankruptcy. The company has maintained a reasonable level of Free Cash Flow over the last few quarters and still has very controlled debt. Therefore, the problem really lies in the reliability and sustainability of these financials, for example, it’s difficult to know whether the Assassin’s Creed franchise – which is relevant to the results – will be able to maintain this player base in the medium and long term, since Ubisoft’s ability to adapt is debatable, having executed once on Assassin’s Creed but proving to have faced some challenges as it did with Star Wars Outlaws and Far Cry.

Koyfin

Cheap Valuation Sustains A Hold Rating, But Risks Remain

One of the things preventing the rating of Ubisoft stock from being a sell is the valuation. The stock is already so depressed that a hold is still the most prudent course of action. A short here (without a stop) could be disastrous if some positive trigger happens and quickly pushes the stock up, whether it’s a launch that goes much better than expected or an extraordinary event such as an M&A.

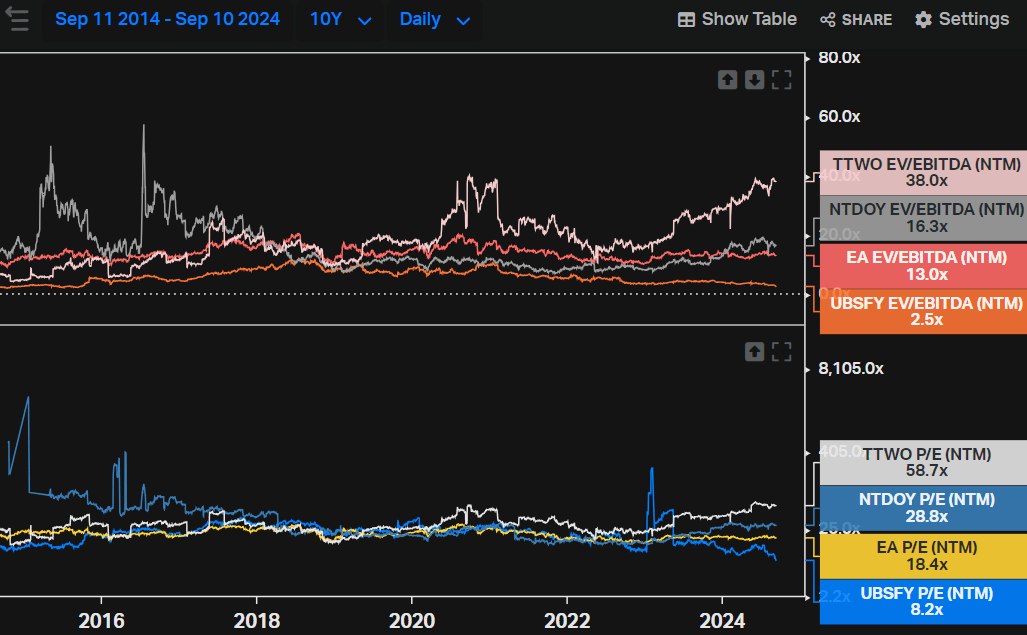

As already mentioned, other game companies deserve a premium over Ubisoft, especially Nintendo and Take-Two. Looking at the EV-to-EBITDA NTM, Ubisoft is trading at 2.5x, while all the others are trading above 10x. For NTM price-to-earnings, Ubisoft is the only one trading below 10x.

Koyfin

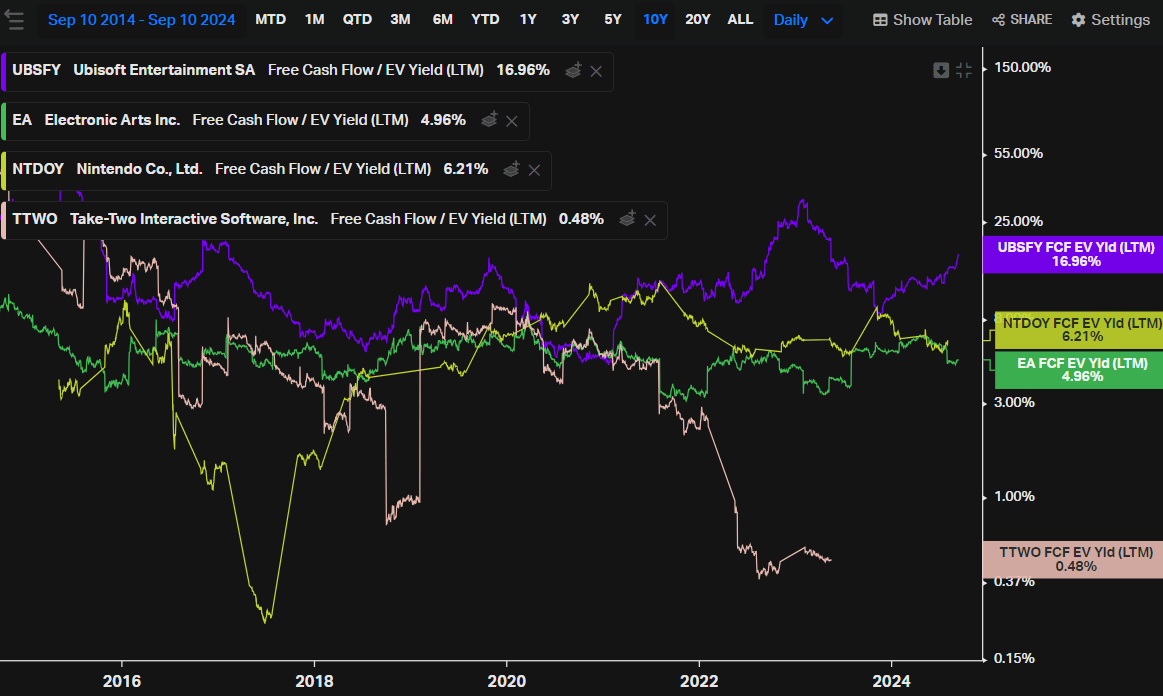

Not only that, but as the company has managed to generate Free Cash Flow in an adequate volume over the last few quarters, its FCF Yield (in relation to its EV) is almost 17% at current prices. Meanwhile, the other companies analyzed trade at less than 6.5%. This level means that as long as the company can just sustain this level of revenue and profitability, it would already be able to return value to the shareholder at an attractive level, since 16% per year even for an uncertain stock is ok.

Koyfin

If we consider how cloudy the financials and prospects are for the next few years and how turbulent the operation (and management) appear to be, it’s not worth adding Ubisoft to the portfolio even at these prices. This is mainly because we can’t count on these ~16% per year being maintained in the medium and long term. The dependence on a few titles is so huge that if a few failures accumulate over a shorter period of time, the company could see a reduction in revenue and pressure on margins. If it were a company with a more reliable track record (like Take-Two Interactive, which relies on GTA), this dependence wouldn’t be as severe as it is.

Counting On M&A Is A Risky Speculation

Recently, a hedge fund called AJ Investments, which owns less than 1% of Ubisoft, requested that the company be privatized or acquired by another investor. Among the arguments, they believe that the company is being “mismanaged” by Guillemot family members and Tencent. Although it’s impossible to know the outcome of this story, it does raise a few points that are worth keeping in mind.

With the stock trading at less than 3x its EBITDA for the next 12 months (in relation to EV) and still a lot of noise about its games, there really is a feeling that the market is undervaluing Ubisoft and not giving it any benefit of the doubt, so if its main shareholders have the necessary capital and believe that the company is too undervalued, a delisting could occur.

Not only that, but there are companies that could capture some synergy with Ubisoft and are capitalized, such as Microsoft (MSFT), which not long ago acquired Activision Blizzard for much more than Ubisoft is quoted on the market today, and also bought Bethesda. But it’s almost impossible to know if Microsoft or any other player would be interested in this, or if it would even be worth it. In Microsoft’s case, they already have a lot of IPs and the bulk of the investment in new game studios seems to have already been made. Disregarding all the current management and possible legal obstacles, would it be worth Microsoft paying ~€3bn (along with debts) to own a few (but important) IPs like Assassin’s Creed and Far Cry? It could happen, but it seems too uncertain to count on it or to justify the exposure of Ubisoft stock.

In other words, even if these possible extra events could trigger an increase in the value of the stocks, I think it’s too speculative to change the thesis or consider it an important reason to invest.

Final Thoughts

What drives my hold rating is mainly the valuation. As a stock traded at infinite multiples and with a controlled capital structure, positive surprises could prevent a rally. On the other hand, this factor alone is also far from sustaining a buy rating.

As a company that is currently going through a troubled scenario – with some failures, pressure on management, and uncertainty about the future of its franchises – adding Ubisoft to the portfolio looks more like a speculative play than a solid investment. These characteristics, together with a less attractive business model than its peers, make me avoid Ubisoft stock for the time being.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

")

")

")