")

")

")

")

")

Note:

I have discussed Enphase Energy, Inc. (NASDAQ:ENPH) previously, so investors should view this as an update to my earlier coverage of the company.

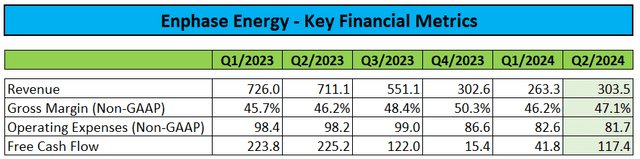

After the close of Tuesday’s session, leading microinverter and battery storage solutions supplier Enphase Energy Inc. or “Enphase” reported another set of mediocre quarterly results with revenues and profitability coming in below consensus expectations:

Company Press Releases

While below analyst projections, reported results were still within the guidance ranges provided in the Q1/2024 earnings release.

Domestic sales increased by approximately 32% sequentially, but revenue in Europe remained flat despite Enphase entering a number of additional European markets during the quarter. Particularly, the important Netherlands market was weak due to ongoing regulatory uncertainty.

That said, weakness in Europe had been widely expected following competitor SolarEdge Technologies’ (SEDG) warning last month.

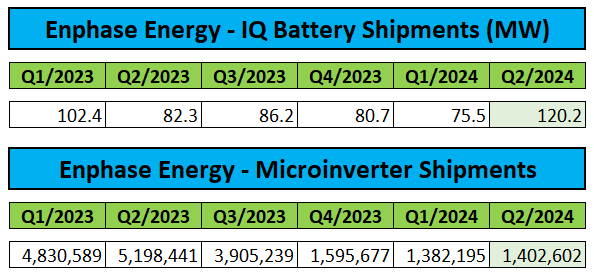

While total microinverter shipments were up just slightly on a quarter-over-quarter basis, sales benefited from an almost 60% sequential increase in IQ Battery shipments:

Company Press Releases

Please note that the company’s global microinverter capacity is around 7.25 million units per quarter.

Battery sales benefited from increased Net Metering 3.0 (“NEM 3.0”) installations in California as over 90% of these systems have batteries attached as compared to just 15% for NEM 2.0 systems.

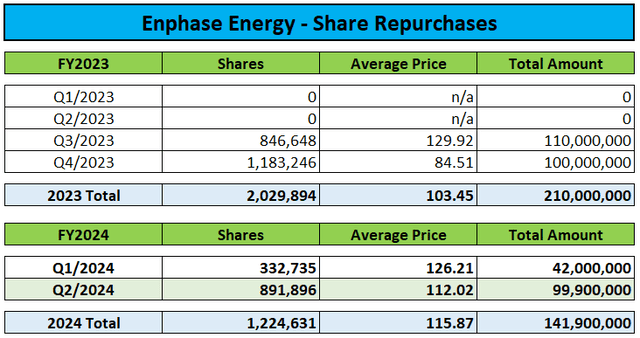

Enphase generated a healthy $117.4 million in free cash flow, which was mostly allocated to share buybacks:

Company Press Releases

Since inception of the company’s up to $1 billion share repurchase program twelve months ago, the company has bought back approximately 3.25 million shares at an average price of $108.13. There is up to $648.1 million remaining under the program.

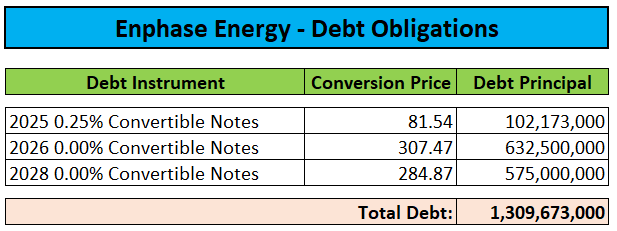

Enphase ended the second quarter with $1.65 billion in cash, cash equivalents, and marketable securities, up slightly from the $1.63 billion reported at the end of Q1.

The company’s debt remained unchanged at $1.31 billion:

Regulatory Filings

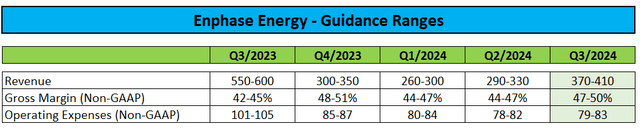

In the press release, Enphase also provided its outlook for the third quarter. While management guided for up to 35% sequential revenue growth, consensus expectations are already sitting near the high end of the range:

Company Press Releases

Similar to Q2, sales will be boosted by a projected up to 50% sequential increase in IQ Battery shipments.

While domestic sales are projected to grow further, Enphase expects a seasonal slowdown in Europe. However, according to management statements on the conference call, backlog is healthy with more than 85% of Q3 revenues (at the mid-point of the range) already booked.

During the questions-and-answers session, a number of analysts appeared to be concerned about microinverter demand not recovering to levels previously anticipated by management, despite sales no longer being dragged down by excess channel inventory.

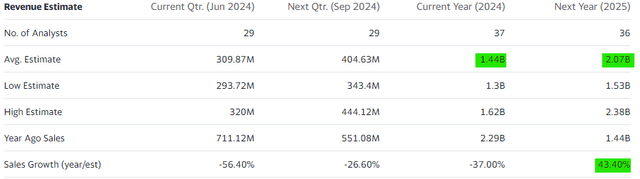

Please note that consensus expectations are currently calling for revenues to increase by well above 40% next year, which translates into an average quarterly revenue run rate of above $500 million, substantially higher than the level expected for the third quarter.

Yahoo Finance

While management remained optimistic on the company’s prospects going forward, I would expect consensus expectations for both 2024 and 2025 to come down further.

For example, achieving the current revenue consensus of $1.44 billion for 2024 would require sales of more than $480 million in Q4, which appears overly ambitious in the current environment.

Despite the company’s mediocre results and less-than-stellar outlook, shares moved up by 5% in after-hours trading, with market participants likely cheering the normalization of channel inventory as well as strong progress in the core U.S. market.

Bottom Line

Enphase Energy reported another set of mediocre quarterly results, with Q3 guidance nothing to write home about either.

While sales will no longer be impacted by excess channel inventory, European demand is likely to remain weak for at least the next couple of quarters.

Consequently, I would expect analysts to adjust their models and reduce revenue and profitability expectations for both 2024 and 2025.

With the industry recovery apparently not as strong as previously anticipated by management and market participants, I am reiterating my “Hold” rating on Enphase Energy’s shares.

Read the full article here

")

")

")

")

(NYSE:BABA)")