")

")

")

Energy Vault (NYSE:NRGV) held promise when it went public on the NYSE via a blank check company in the winter of 2022. However, the reality since then, like many climate economy tickers, has been marred by aggressive interest rate hikes that have collapsed investor risk sentiment and turned portfolios sour on unprofitable renewable energy tickers. Current shareholders should be cognizant of NRGV’s falling liquidity base which when aggregated with continued near-term cash burn could push the ticker below the NYSE’s $1 minimum listing requirement. Hence, my outlook on the ticker has changed for the worse since I last covered it.

NRGV offers a range of short, long, and ultra-long duration energy storage systems. The firm is known for EVx, a gravity-based long-duration energy storage system that uses renewable energy to lift large composite blocks that can then be dropped when energy is required. The kinetic energy generated from dropping the blocks spins generators that create electricity. EVx is offered through the company’s G-VAULT platform. NRGV has since expanded its energy storage offerings to include lithium-ion battery storage platform B-VAULT and a hydrogen energy storage platform named H-VAULT.

Energy Vault Website

Operations, Ramp, And Cash

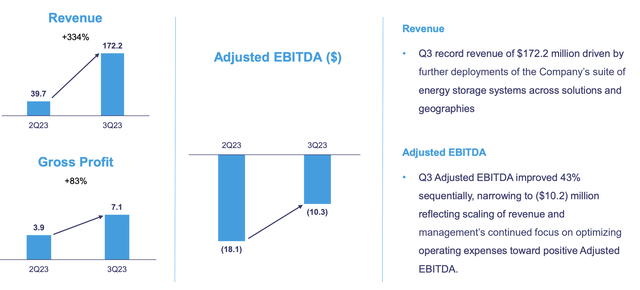

NRGV generated $172.2 million in revenue during its last reported fiscal 2023 third quarter, a remarkable achievement for a company currently trading at a $240 million market cap. Revenue was also up from $1.7 million in the year-ago comp and was driven by the uptake of its batteries within the US market. Gross profit for the quarter was positive at $7.1 million for a roughly 4.1% gross profit margin. The quarter was decent with core profitability metrics like adjusted EBITDA seeing a 43% sequential improvement to a $10.2 million loss.

Energy Vault Fiscal 2023 Third Quarter Presentation

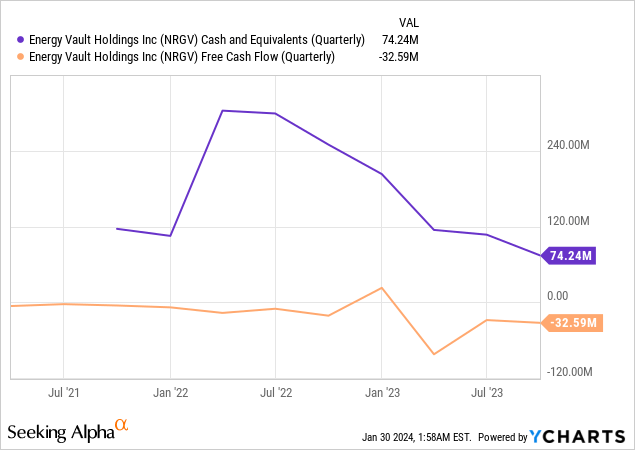

NRGV’s net loss during the quarter was $18.9 million, an improvement from a loss of $28.8 million in the year-ago comp. The company earned $2 million of interest income on the back of its cash, cash equivalents, and restricted cash balance of $132.2 million. However, this balance has been dropping heavily. It was $286.2 million at the start of NRGV’s fiscal 2023 and has dipped at a rate of $95.4 million per quarter to its current balance. Assuming NRGV’s quarterly cash burn continues to reflect this rate of decline would mean a cash runway of roughly two quarters.

Cash burn from operations for the nine months as of the end of the third quarter was $116 million, up 142% from $48 million in the year-ago comp. These metrics around cash are the core figures to watch and why the stock has dipped so much. Revenue is ramping but operations are highly unprofitable and gross margins in the low single digits mean material profitability gains will be required to shift the dial on cash burn.

Energy Vault Fiscal 2023 Third Quarter Presentation

NRGV does stand to ride significant secular tailwinds as developed nations move more aggressively to decarbonize their electricity grids with wind energy and utility-scale solar. Growth has continued even with higher interest expenses and inflation that has swelled costs and disrupted buildout times of new renewable energy projects. The collapse of renewable energy yieldcos like NextEra Energy Partners (NEP) reflects this negative change in the investment zeitgeist towards climate economy tickers. NRGV’s cash burn would likely have been a footnote in the ZIRP era but now poses an existential risk with the Fed funds rate currently at a 22-year high of 5.25% to 5.50%. It’s been a brutal environment, with Californian short-duration energy storage leader Stem, Inc. (STEM) experiencing a fall of 70% over the last 1-year.

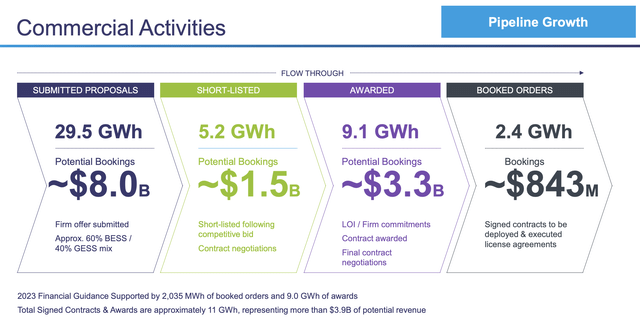

This pull forward of profitability expectations means NRGV’s forecast for full-year 2023 revenue to come in between $325 million and $425 million is less relevant to its valuation in the near term. Is the stock still a buy? Not in the current environment. NRGV pipeline is impressive though with booked orders of 2.4 GWh, around $843 million, at the end of the third quarter. This was up 49% year-to-date with awarded projects up by 153% to 9.1 GWh of $3.3 billion. Hence, there could be a strong argument made for the company now trading for 0.3x its booked orders. NRGV also stated during its third-quarter earnings call that they expect their cash burn to slow markedly during the fourth quarter as new projects come online to drive lower cash burn. The company also secured a $1 billion non-cash project performance bonding capacity and expects gross profit margins to come in between 10% to 15% as of the end of its fourth quarter. I’m less enthusiastic on the ticker due to the short cash runway but there could be a significant rerating if the guidance for lower cash burn is realized. I have no position here.

Read the full article here

")

")