")

")

")

Q3 2024 Earnings Call Transcript")

")

")

The first thing I ask myself when I think about buying shares in a new company these days is, “Will they improve the quality of my portfolio?”

Frankly, the answer is usually no.

You see, I already own shares in 65 different blue-chip companies. I’ve already got my bases covered when it comes to just about every sector, industry, and secular growth story that I want long-term exposure to. Those 65 stocks set a pretty high bar to clear as far as quality goes. And therefore, so long as I stay disciplined, it should be quite difficult to add a new company to my portfolio moving forward.

For the last year or so I’ve been actively trying to reduce my holding count by taking profits when redundant investments run up to overvalued territory. As life gets more and more complicated (my kids are getting older and require more and more of my time), I’d like to reduce that holding count to 50 stocks or so. I’m still a full-time equity analyst, staying on top of these holdings is a part of my normal work week. But, these days I’m spending more and more time writing newsletters and special reports for subscribers and the actual equity analysis part of the job is often pushed out into the wee hours of the night.

My doctor tells me I should sleep more. And I know I’m a better dad and husband when I’m well rested. So, I’m trying to listen.

Yet, when a compelling opportunity arises in the stock market I’m not going to ignore it. Part of my job as a husband/father is to serve as a provider for my family. And being that my plans for financial freedom – or, as my young daughter calls it, the “forever weekend” – revolve around the reliably increasing passive income created by wonderful dividend growth stocks, when one goes on sale, I’m still willing to buy it.

Recently, when Emerson Electric Co. (NYSE:EMR) sold off, and I posed the question to myself, “Would owning shares of this company improve the quality of my portfolio,” the answer was, “Yes.”

So, I bought the dip. A couple of times.

On 8/2/2024 I established my EMR position at $108.19. About a week later, on 8/7/2024, I added to the position into further weakness at $99.92. In this article, I’ll explain why Emerson Electric is now a part of my dividend growth portfolio and why it’s a stock I’ll likely continue to add to so long as the sentiment surrounding shares remains poor.

Emerson Electric Company Overview

Emerson has been on my watch list for a while now because I’ve been wanting to add exposure to a secular trend that I believe in the re-industrialization of America.

I’ve written about this before, but in short, this is a broad idea, that encompasses the onshoring (and near-shoring) of manufacturing capabilities to the US due to ongoing geopolitical strife and the supply chain headaches that arose during the pandemic (which companies – and governments – have been taking steps to fix ever since).

But, the factories that I envision coming back aren’t your grandfather’s factories. Neither is the underlying infrastructure that will make it all possible.

I believe that demand trends in the manufacturing and logistics space are going to usher in the 5th Industrial Revolution now that technological advancements are making truly automated factories and even supply chains possible.

As the 5th Industrial Revolution plays out in America, I expect to see hardware and software continue to mesh in the manufacturing and logistics processes, resulting in increasingly advanced manufacturing/shipping systems that will require total reconstruction, or at the very least, refabrication, of the existing environment.

Automation will play a central role in this trend, as will ongoing electrification of the US economy.

Emerson is primed to benefit from these trends.

EMR Investor Relations

Morningstar says, “In our view, Emerson Electric is the undisputed powerhouse in process manufacturing on the west side of the Atlantic.”

To me, this company is a top-notch player in the industrial space alongside companies like Honeywell International Inc. (HON), which I already own, Eaton Corporation plc (ETN), which trades with a hefty, 30x P/E multiple, GE Vernova Inc. (GEV), which trades for 27x earnings, and Vertiv Holdings, which is the most expensive of the bunch, with a blended P/E ratio of 36.5x.

These are all industrial powerhouses that I’d be happy to own at the right price; however, right now, EMR and HON are the only two trading at a discount to fair value, which is why I’ve been adding to these names (and not their peers).

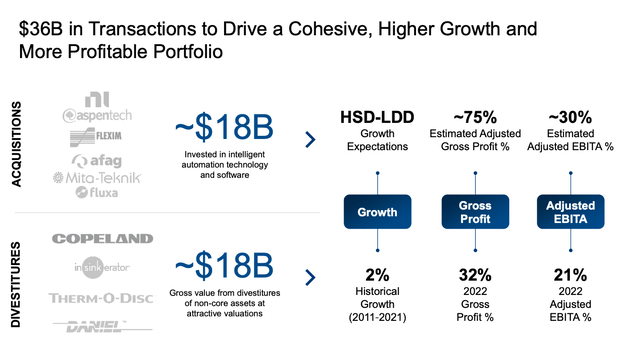

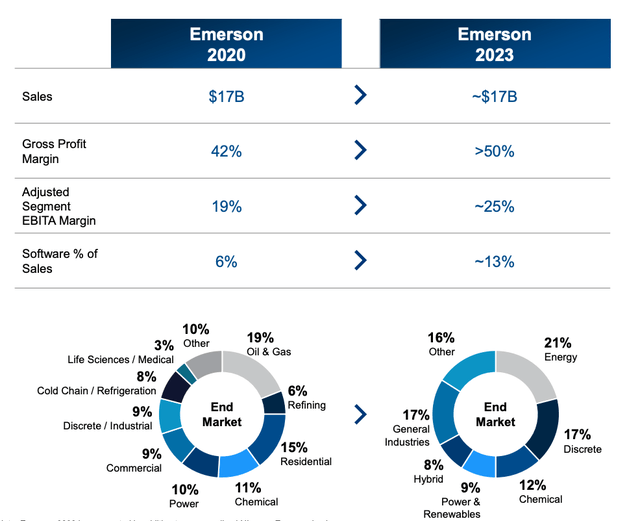

I’m surprised to see EMR’s relative discount to peers because this is a company that has totally evolved in recent years. Emerson has taken steps to sell off non-core segments of its business and used the proceeds to acquire industrial software assets.

EMR Investor Relations

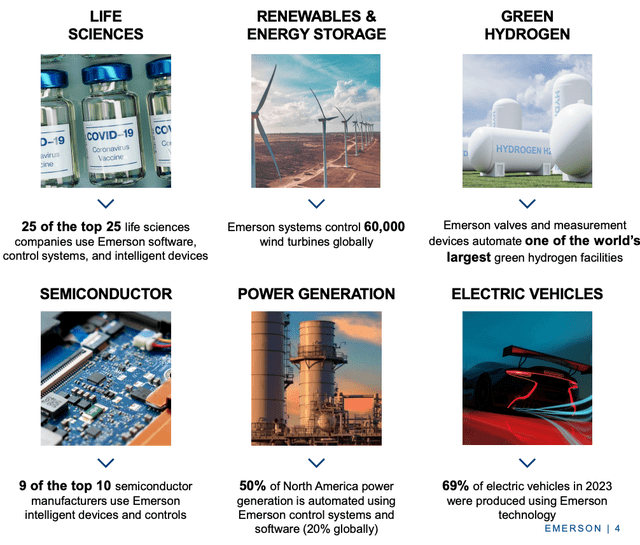

The trends that EMR is investing in are enormous.

The company believes:

-

The global energy transition towards renewable energy and decarbonization “have a $12b TAM [total addressable market] growing double digits”.

-

The industrial software market has a $35b TAM.

-

The Factory automation market has an $80b TAM.

-

The Life Sciences industry offers a $7b TAM (regarding the implementation of AI/software into the manufacturing process).

-

The Metals and Mining industries offer a $10b TAM as demand for batteries and decarbonization technology increases.

As you can see, in a very short period of time this company has revolutionized its operations and while there are ongoing questions about M&A synergies and concerns about the valuations that EMR paid for recent software acquisitions, I love the company as it stands today.

EMR Investor Relations

The company has repositioned itself as a pure play on the advanced manufacturing/electrification trends.

Bank of America Global Research says, “The transition to a pure-play industrial automation firm should also lead to higher valuation multiples over time, in our view”

I don’t know if we’ll see significant multiple expansion here; however, as I’ll highlight in a moment, fundamental growth alone has the potential to propel shares much higher.

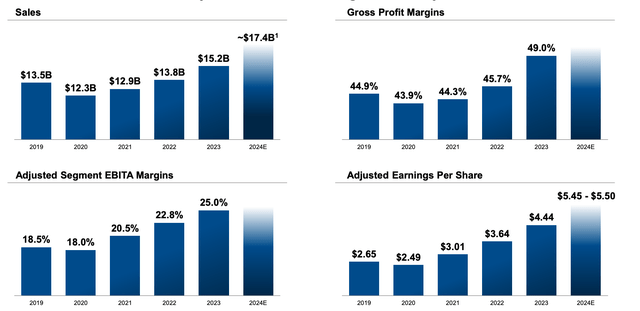

What is clear is that the moves that the company has made in recent years are already paying off from a fundamental growth perspective.

I love seeing companies that are able to increase sales and margins at the same time. Those are typically wonderful stories that signify wide moat companies with secular growth tailwinds.

EMR Investor Relations

I missed the boat when it came to utilities rallying this year because of increased demand from data centers and artificial intelligence. And for the longest time, companies like Emerson were also high flyers because of the huge book-to-bill ratios that we’re seeing play out when it comes to the leaders in the electrification space too. Yet, EMR’s momentum slowed down as of late.

The stock experienced a 13% sell-off from recent highs on a somewhat disappointing earnings release. Yet, I don’t think the company’s long-term growth potential has changed. To me, the secular growth trends that EMR has centered its new business around have years (if not decades) to run and therefore, I was happy to use EMR’s recent dip as an opportunity to rectify my lack of exposure to the automation/electrification trends.

Valuation

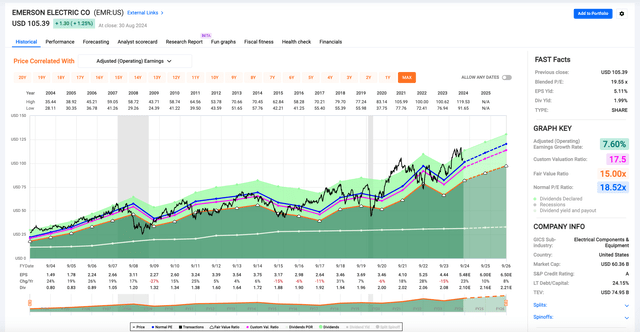

Today, EMR trades with a blended P/E ratio of 19.5x.

The consensus analyst estimate (the combined opinions of 22 Wall Street experts following the stock) for EMR’s EPS growth in 2024 and 2025 is 23.4% and 9.5%, respectively.

With that growth in mind, EMR is cheaper on a forward basis.

Shares are trading for 19.2x its 2024 consensus EPS of $5.48 and just 17.5x 2025’s consensus EPS estimate of $6.00/share.

Those forward multiples are below EMR’s 5, 10, and 20-year average P/E ratios of 20.2x, 19.0x, and 18.5x, leading me to believe that shares are fairly priced at the moment.

Being a historically cyclical company, EMR has had more earnings and share price volatility than I’m used to; however, that’s the nature of companies from this sector.

But, I believe that Emerson’s shift towards software offerings and the secular nature of the demand trends driving its new business will help to reduce earnings volatility moving forward, resulting in less share price swings through up/down cycles.

I think this is already showing up in the estimates, which are positive for the next three years.

FAST Graphs

I believe that 17-18x forward is a fair multiple to place on shares of a blue chip like this (and I wouldn’t be surprised to see EMR maintain a multiple at – or even above – the 20x threshold (remember, several of its peers are trading in the 25-30x forward range).

At the $105 area, I don’t think there’s a very wide margin of safety attached to shares. My fair value estimate for EMR is $111.00. My recent purchases were an example of me channeling my inner Warren Buffett and buying shares of a wonderful company at a fair price.

But as I’ve learned, time and again, over the years… that’s all I need to do to generate satisfactory returns in the market.

As a long-term investor, I’m more concerned with asset allocation and portfolio positioning, in terms of maintaining exposure to the strongest secular growth trends than I am waiting for extraordinary margins of safety.

The fact is that companies like EMR don’t go on big sales very often.

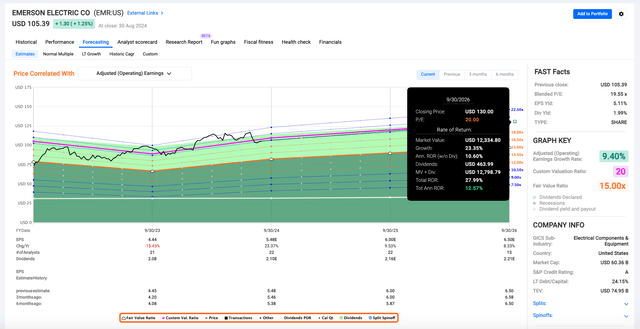

If/when EMR dips down to the 15x level like it has several times during the past decade, I’ll happily buy more shares. But, I think the opportunity cost of sitting on the sidelines and waiting for those rare moments is too great because of future growth. In EMR hits next year’s EPS projections and maintains a 20x multiple, then we’ll be looking at share prices in the $120 range (up 14% from here).

Two years from now, we’ll be talking about a $130 price (a 12.5% annualized rate of return with dividends included) and I know I’d regret not having bought shares at $105.

FAST Graphs

I was hoping to have the opportunity to accumulate more shares below the $100 threshold, but EMR quickly bounced off of recent lows. But, I have cash ready to go in the event that sentiment sours again.

The Dividend

In the meantime, I’ll happily sit back and collect this dividend.

Emerson Electric yields nearly 2.00% at the moment.

This company is a Dividend King with 67 years of consecutive dividend growth.

It doesn’t get much better than a streak like that, and I certainly sleep well at night knowing that EMR has been paying a rising dividend for nearly twice as long as I’ve been alive.

My biggest gripe with the dividend is the slow dividend growth as of late. EMR’s 5-year DGR is just 1.39%. Emerson has been providing paltry 1-2% annual raises for nearly a decade now. This is largely due to the operational restructuring and M&A that I discussed above. While evolving the business, management appears to have wanted to maintain as much capital as possible for potential acquisition opportunities. I respect that. Though, I’d be lying if I said EMR’s low-single digit dividend growth wasn’t a disappointment.

Frankly, the lack of dividend growth is what kept me out of the stock for so long. Usually, a company with a ~2% yield needs to provide 8%+ annual dividend growth for me to consider ownership. But, I view this as more of a growth play than a dividend growth play because of the automation/electrification upside. EMR’s 2% yield is a nice kicker on top of those growth secular trends. I don’t know when the company’s focus will shift away from M&A and back towards shareholder returns.

EMR Investor Relations

Emerson clearly expresses its desire to continue to raise the dividend. And now that much of the restructuring appears to be over with, I’d love to see management start a trend of annual raises that exceed inflation.

Conclusion

Despite the poor dividend growth, I believe that EMR’s dividend is quite safe. The company’s forward payout ratio is just 35%. That’s solid coverage and well below Emerson’s historical average.

Historically, EMR’s dividend payout ratio has hovered in the 40%-50% range, which would imply stronger dividend growth in the coming years than we’ve seen in the recent past.

A 40% payout ratio of next year’s $6.00 EPS estimate would result in an annual dividend of $2.40/share. That’d be a 14.2% raise compared to the current $2.10/share dividend. I’d be ecstatic about that.

Only time will tell if I’m right about increased dividend growth prospects moving forward, but like I said before, my main focus here is the underlying secular growth trends that EMR should benefit from, resulting in reliable earnings growth prospects for years to come.

It’s easy for me to be a long-term shareholder when I know that the forces driving cash flows higher have very long runways ahead of them…and that’s especially the case when we’re talking about a Dividend King trading with a valuation that is below long-term averages.

Read the full article here

")

")

")

Q3 2024 Earnings Call Transcript")

")