")

")

")

")

Investment Thesis

I recommend buying Eletrobrás (NYSE:EBR) shares after the release of the 2nd quarter results. Although the company has shown an increase in costs and a reduction in profits, I believe these are isolated events.

In addition, Eletrobrás continues to show excellent signs, such as a reduction in operating expenses, and the company is continuing its strategy of divesting non-core assets, which should improve its capital structure. With an attractive valuation, my view is quite positive.

Review Of Eletrobrás in 2Q24

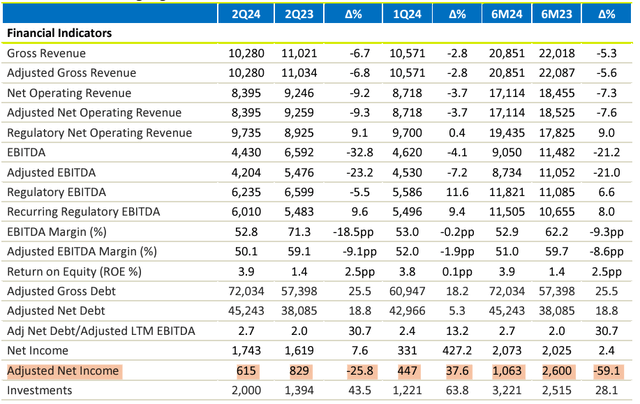

Eletrobrás released its 2nd quarter results on August 26th, and as we can see below, revenues did not match market estimates, but profits beat estimates.

Earnings (Investing)

From now on, I will comment in detail on each segment of the result. But first, it is interesting to note that the company publishes its results in BRL, so I will convert them to US dollars using the exchange rate 1 dollar = 5.59 reais, as this was the exchange rate on the last day of the second quarter. Enjoy your reading!

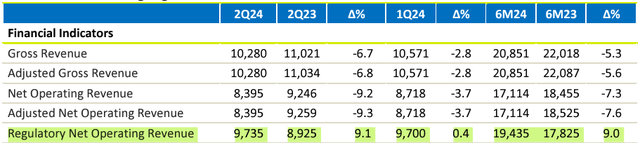

Revenues – Various Events

As we can see below, the company had a 9.1% annual increase in its Regulatory Net Operating Revenue, reaching BRL 9.7 billion ($1.74 billion.). This was due to the recognition of revenues related to Amazonas Energy totaling BRL 482 million ($86 million). Another factor was the 10% increase in energy volume, offsetting the 11.8% drop in prices compared to 2Q23.

Net Revenue (IR Company)

In my view, the company should continue to grow revenues, as seen in the gradual rehiring of the generation segment and the incorporation of other subsidiaries.

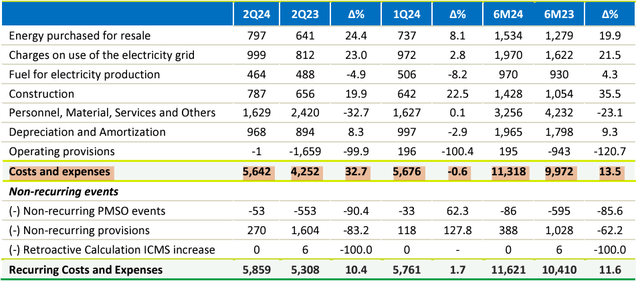

Costs, Expenses and Margins – Various Events

Total operating costs increased by 32.7% YoY to BRL 5.6 billion ($1bn). The highlights were the charges for using the electricity grid and the increase in costs for purchased energy.

Costs and Expenses (IR Company)

It is worth noting that the increase in costs was due to unmanageable factors, such as fuel expenses. The 19% reduction in PMSO (Personnel, Materials, Services and Others) expenses was influenced by 15% lower personnel costs, in addition to reclassifications, maintenance, and lower material purchases.

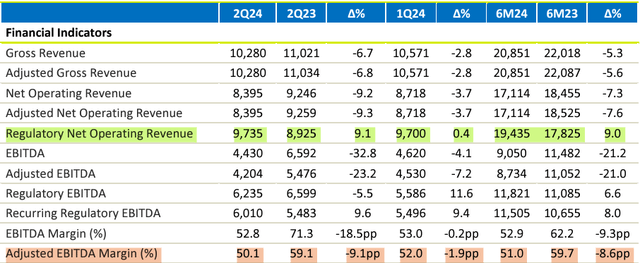

Finally, the company obtained an adjusted EBITDA margin of 50.1%. This represents a reduction of 9.1% compared to 2Q23.

EBITDA Margin (IR Company)

In my view, the company did what it could. Although there was a reduction in the EBITDA margin due to an increase in costs (often beyond the company’s control), Eletrobrás partially compensated for this with yet another excellent expense control, which corroborates my thesis of starting coverage and reiterates my recommendation to buy the shares.

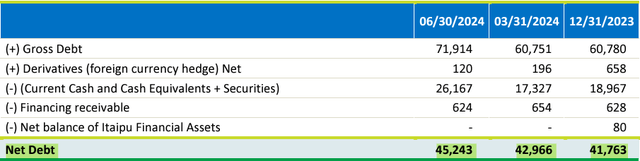

Debt – Doing Well

The company ended 2Q24 with a net debt of BRL 45.2 billion ($8 billion). This results in leverage close to 1.95x, which I consider healthy given the company’s business model.

Net Debt (IR Company)

As for perspectives, the recognition of the proceeds from the sale ($403 million) of the shares in ISA CTEEP should further improve Eletrobrás’ capital structure in the future, which again corroborates my positive view of the shares.

CapEx – Investing In Electricity Transmission

Eletrobrás announced a CapEx of BRL 2 billion ($357 million), and of this amount the company invested around BRL 610 million ($109 million) in the transmission segment.

CAPEX (IR Company)

In my view, the divestment of non-essential assets, the simplification of the corporate structure, and greater assertiveness in Capex will make Eletrobrás an extremely competitive company in the LatAm scenario.

Net Income – You Have To Look Beyond The Number

Due to higher operating costs, obligations and financial expenses, Eletrobrás reported a 25.8% annual reduction in net income to BRL 615 million ($110 million).

Net Income (IR Company)

What was the overall balance of the result in my view? My investment thesis in Eletrobrás makes it clear that this is a turnaround, so the results will have ups and downs. However, the company has once again demonstrated a reduction in operating expenses, strategic divestment and an improved capital structure.

Even if this is punctuated by a reduction in margins, an increase in unmanageable costs and a one-off reduction in profit, it does not change my view of a gigantic company that is improving its results every quarter. My buy recommendation remains reiterated.

Valuation – Cheap For Me

The thesis is definitely not a market consensus, we can see this through the metrics that Seeking Alpha offers us:

Summary (Seeking Alpha)

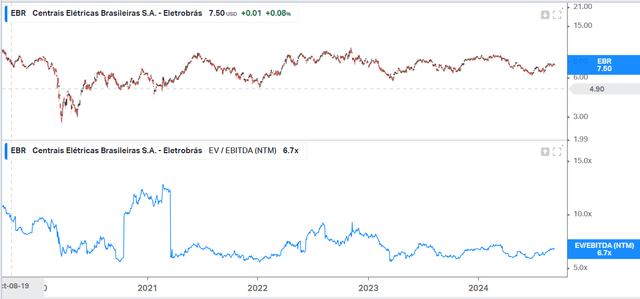

One of the ways I like to evaluate Eletrobrás, as it is a very peculiar company, is through the EV/EBITDA multiple against its own history.

EV/EBITDA (Seeking Alpha)

As we can see, in the last 5 years, Eletrobrás has traded at lows of 5.6x EBITDA and highs of 12x EBITDA. Considering an average of 8.8x EBITDA and that it is currently trading at 6.7x EBITDA, this implies a potential appreciation of 31%, which corroborates my buy recommendation.

Potential Risks To The Bullish Thesis

In my view, the main risk to the thesis today is regulatory and political. It is worth noting that Eletrobrás was privatized by the previous government, and the current government is completely against privatizations. Since it is a regulated sector, I would not be surprised if the government treats Eletrobrás differently because it is now privatized.

In addition, there is a discussion about increasing the government’s power to vote at the company’s shareholders’ meetings. In short, the risks to the company are diverse, and investors should be cautious in their analysis.

The Bottom Line

Eletrobrás reported results as expected in 2Q24, although I saw positive trends, such as the reduction in operating expenses and the continuation of strategic divestment.

It is important to highlight that turnaround theses are marked by ups and downs in results, therefore, a one-off reduction in net income and an increase in costs for unmanageable reasons do not take away the shine of the thesis for me.

Based on this analysis, I recommend buying Eletrobrás shares. In my view, the company is a giant that is undergoing a profound process of operational improvement, and in the future it should present very robust results.

Read the full article here

")

")

")

")

")

")