")

")

Introduction

A research report from Nuveen revealed some key insights about the municipal bond market, and Nuveen also issued a very bullish outlook, in Municipal bonds: poised for growth in a favorable market.

The report was done based on the market information available at the end of Q2 2024. While the Muni market insights remain very similar, the macro conditions such as rate cut and economic data have changed. On the other hand, most Muni funds have been pretty flat in the past 2 months or so, the highly anticipated Muni bond recovery is still yet to happen. I look at it as a key consolidation phase before the next move to break out from the current narrow trading range. Many institutions (funds) have actually been increasing their positions in Muni funds. Eaton Vance Municipal Bond Fund (NYSE:EIM) is a good example of such Muni fund. I recommend interested investors to follow the money flow and buy EIM shares right now and lock in the high yield. EIM has a (federal tax exempted) dividend at 5.84% and a NAV discount at 8.74%. I expect a decent total return for EIM in 2024, assuming the rate cuts get started in September. The high-yield and top credit quality make it a good holding for long-term income investment.

EIM Fund Overview

EIM is a Muni bond CEF managed by Eaton Vance. It was incepted on August 30 of 2002, 3 years after Eaton Vance launched its sister fund EVN.

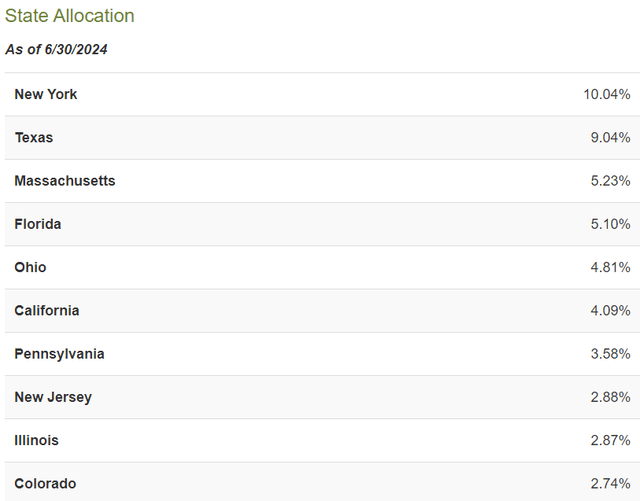

The fund focuses on a portfolio of municipal bonds from various states. In the current portfolio, the top two states are New York with 10.04% weight and Texas with 9.04% weight. The next tier includes Florida, Ohio, California, Pennsylvania with less weights, as shown below:

EIM Portfolio State Allocation – from CEFConnect.com

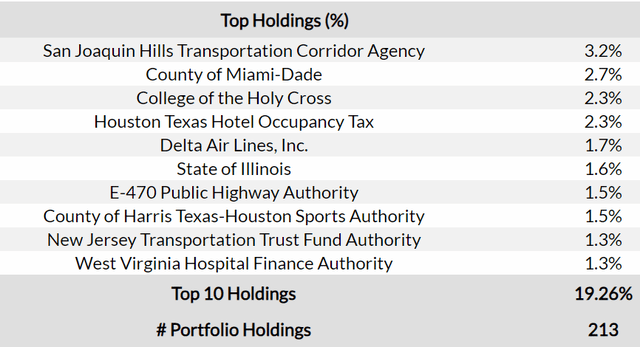

The total holdings are 213, which is smaller than some of the bigger Muni funds and Muni ETFs, where over 500 or even 1000 municipal bonds can be found in the portfolios. It is still a well diversified bond portfolio with the top 10 holdings taking 19.26% weight as shown below.

EIM Top 10 Holdings – from CEFData.com

The following summarizes some of EIM’s key characteristics:

- AUM: $651.19M.

- Volume (last day): 57,032. The volume is a bit tight for trades.

- Inception: August 30, 2002.

- Yield: 5.84%. Tax-exempted high yield.

- NAV (Discount): 8.74%.

- Expense Ratio: 1.09%. The expense is a bit higher than its sister fund (0.98%).

- Risk Score (Morningstar): 21. It is considered “conservative“.

- Credit (A or higher): 85%. Credit is of top quality.

- Duration (modified): 7.89 years.

- Leverage: 29.20%. It is a high leverage, although less than the CEF average and some high-yield Muni funds with leverage at high 30s in percentage.

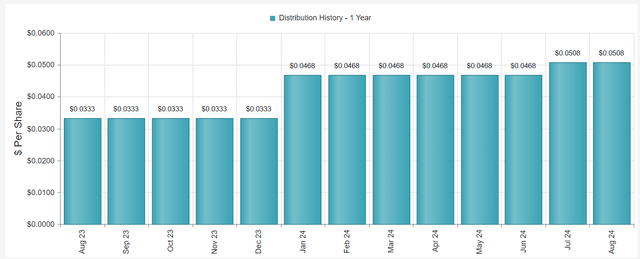

The dividend distribution was increased recently in July, which is the second increase in 2024, as shown below:

EIM Distribution History – from CEFConnect.com

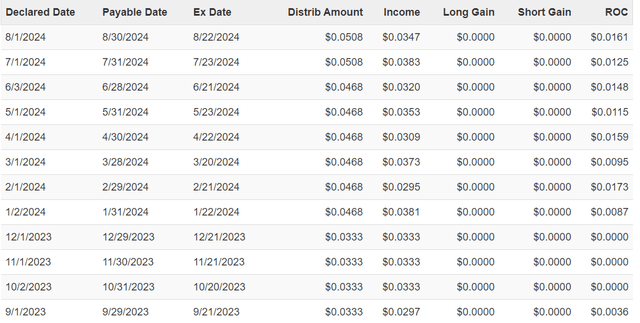

Notice that the increased portion in 2024 has been primarily funded by the ROC, as indicated below:

EIM Recent Dividend increase and category – from CEFConnect.com

Favorable Macro Scenarios Make Muni Funds Attractive Potential Gainers in the Near Term

Municipal bond markets are highly fragmented and often very illiquid in trading. Individual investors like myself can be overwhelmed by so many choices. It will be a much easier job to select the Muni funds (covering hundreds or even thousands Muni bonds in the portfolios) based on the fund properties and characteristics such as, AUM, yield, NAV discount, leverage, etc. These have been proven to be pretty stable identifiers for funds with a long trackable history. The investors should spend more time focusing on the macro conditions and portfolio positioning.

As indicated at the beginning of Introduction, Nuveen views the Muni market as favorable for growth.

Investors feel confident that both Treasury and muni rates should be lower by year end, so they are looking to lock in higher rates now.

For investors looking for price gains, lower rates will mean higher prices. I believe that the price appreciation of the bonds will be sufficiently reflected in the Muni funds. Furthermore, the funds with better bonds selections are expected to be the price winners. EIM is a good choice with the top (A or higher) rated bonds mostly.

The rate cuts could also help to reduce the leverage cost, as many Muni funds use high leverages. It is also possible the potential rate decline cycle could officially get started with the first cut. These are the times when the CEFs, including Muni funds, tend to perform well. Similarly, EIM’s 29% leverage could provide positive effects on the returns of the fund.

Keep in mind that investors are often given alternatives from the same issuer. This will provide some flexibility to select funds that can meet investors’ specific requirements such as diversification, durations etc. The following is a key summary of EIM’s sister fund EVN, provided for reference purposes.

EVN – Eaton Vance Municipal Income Trust

- AUM: $454.59M

- Volume (last day): 94,836.

- Inception: January 29, 1999.

- Yield: 5.68%. Tax-exempted high yield.

- NAV (Discount): 5.50%. It is a smaller discount than EIM.

- Expense Ratio:0.98%. It is smaller than EIM.

- Risk Score (Morningstar): 26. It is considered “Moderate”, higher than EIM.

- Credit (A or higher): 57%. Lower quality than EIM.

- Duration (modified): 7.89 years.

- Leverage: 24.79%. It is less than EIM.

Notice some key differences compared to EIM. EVN has a lower credit quality and a higher risk score than EIM. On the other hand, EVN has received a 5-Star rating from morningstar.com, while EIM is rated 3-Star.

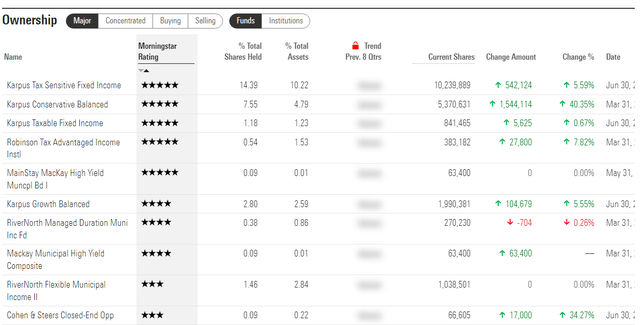

There has been continued accumulation of new positions in Muni funds

Many funds have been putting new money into EIM in 2024, as shown below. Notice the two big percentage changes, one is over 40% and the other is over 34%.

EIM Ownership Rating Sorted -from Morningstar.com

It is worth noting that its sister fund EVN has gotten relatively less attention despite its better (5-star) Morningstar rating. I believe it is due to the smaller NAV discount (5.5% at the moment), which may be viewed as more expensive than EIM.

Notice that the Muni active ETFs have also attracted a lot of interest and money flows. It was recently reported that investors “Suddenly Have a Lot More Active Muni ETFs to Choose From“. One of the ETFs highlighted is active ETF CGMU, as shown below:

CGMU Charting – from SA

CGMU has gained about $1B in AUM to reach over $2B in a short period of time.

I believe the “big money” has been preparing for the capital gain from the Muni funds in 2024, in anticipation of a rate cut from the FED. Notice that CGMU pays a 3.1% dividend (tax-exempted), which is much lower than the high-yield Muni funds. EIM offers a better dividend at 5.8%. Higher yields like over 7% are not difficult to find in Nuveen’s Muni CEFs. Interested readers can find some details in my previous analysis. Notice some of the Nuveen’s Muni funds have also seen significant inflows of money. While EIM stands out with the top quality holdings and the high yield, the new money in CGMU would probably look for the price “alpha” in the shorter run.

Risks and Caveats

Keep in mind that the Muni market could be affected by the seasonal increase in supply from the new issuance of Muni bonds. For example, “Muni bond yields may come under pressure due to heavy issuance”, noted by the report from Nuveen (see the link at the beginning).

This may explain the short-term price behavior for these funds, but certainly represents price volatility risk, which is very sensitive to some income investors.

The high leverage of the CEF is still a risk factor, and still subject to volatility, even after a potential rate cut in September. The total performance return could still be affected and become uncertain.

Closing Thoughts

EIM is a solid long-term holding for income investors thanks to the top quality credit rating, with A or above ratings exceeding 85% of the portfolio. The high yield (5.8%, federal tax-exempted) fund offers a good choice for income investors who want to get into the Muni space without having to select the individual bonds for themselves. The current rate-cut plan and the possible rate decline cycle could be strong tailwinds for EIM to narrow down its NAV discount (8.74%) and produce an attractive total return in the short term. The EIM has seen quite some incoming money flows from the top-rated institutions/funds. Income investors may want to get in right now to lock in the high yield and wait for a possible price appreciation in 2024.

Read the full article here

")

")

")