Q2 2025 Earnings Call Transcript")

")

Dear readers/followers,

It’s been a number of months – almost since November of last year – since I updated on E.ON (OTCPK:ENAKF) (OTCPK:EONGY). The company has released a number of updates and results since my last article, and while we haven’t seen outperformance from the company by any means, we’ve seen solid results in a way that means I might be at the very least interested in looking closer.

However, keep in mind that because in my last article, I considered the company fully valued, I am unlikely to present the company with an attractive valuation target here in relation to where it trades right now. Enel (OTCPK:ENLAY) is currently my, by far, the largest utility investment out there – and this has not changed since my last article.

While I have picked up a number of other businesses since then, among them Black Hills (BKH), Evergy (EVRG), and others, my main focus for utilities remains on the European market. While all markets are potentially attractive, it’s the EU and NA markets, I consider to be the most stable in terms of income and delivering results.

I’m a big fan of diversifying portfolios with utility companies because they can provide stability during market volatility, as they offer safer cash flows due to their regulated nature. That’s why I continue to put large amounts of capital in my portfolios towards utilities at this time.

At this time, E.ON has underperformed the broader market, and we’ll look at what sort of upside this company has. You can find my last article on the company here.

E.ON – The company’s performance and upside

Utilities are In an interesting place right now. From a position where most utilities seemed to have approached renewables much like “give me any renewable project at any price now!”, we’re now in a not-unsurprising situation where every company with half a mind seems to, including E.ON, be very careful about what sort of projects they work with and apply for.

It’s a value-over-volume approach that’s ruling the space, and to me, It feels like “sanity” has returned here. This is not to say that renewable projects are not generally value-accretive – they are. It’s just that for some time, construction and ancillary costs (such as service) were hard to take into account, and resulted in unprofitable potential. Now we’re seeing this normalize. So as long as companies manage solid purchase price agreements, things should work out.

Remember also that there’s an AI-driven level of increase in data center power consumption – and this should keep these prices elevated as well and not allow them to drop too far.

Businesses are required, including E.ON, to work on their infrastructure/network investment – because the biggest hurdle to transition isn’t actually production, it’s the grid. It means that any company worth its salt and with assets in infra has been stepping up investments here. This is also what has driven the unfortunate decline in another company I write about, National Grid (NGG), but which I continue to view as attractive.

I’ve made no secret of the fact that I view the entire Utility sector as undervalued. That’s why between 2021 and 2023, until now, moved from less than 2% to 11% utility investments in my personal and commercial portfolio. The sector now poses, depending on where you look and what geographies you take into consideration, a yield of around 4-4.5% which is in line with the historical ones. Part of the problem we see at this time is that risk-free rates are up, which presses down these companies as well.

E.ON, meanwhile, is still flying on the asset swap with RWE back in 2020. All of this and the things that happened after have meant that the company is now fully exposed to the network side of things, with around 70% of networks coming from Germany – the rest are Sweden, Central Europe, and Turkey. These high renewables investment opportunities that are currently abound in Europe have led E.ON, as of the latest communicated earnings and trends, to increase network investments by 18%.

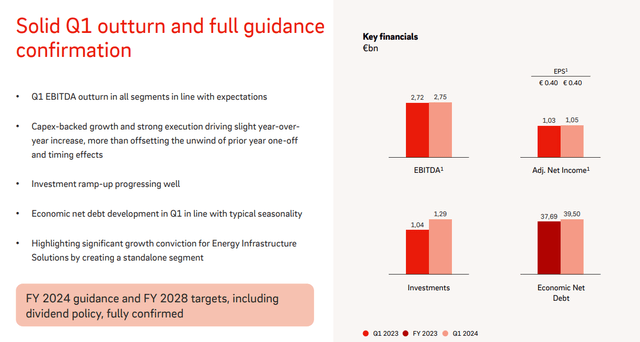

Otherwise, if we look at the 1Q24 period, we saw a solid performance in line with expectations across every single segment. The company was also able to confirm the 2024E guidance as a result of this.

E.ON IR (E.ON IR)

As you can see, this also includes the dividend guidance. E.ON saw organic growth in RAB, with a new regulatory period in Sweden and an unwinding of network loss recoveries. The most positive trend as I see it was the company’s net income, which on an adjusted basis was up even in the absence of any positive one-offs which we had last year. It resulted in a quarterly EPS of €0.4.

The company still is far from the “best” utility out there – in that, I prefer to invest in other utilities above E.ON, but it’s becoming more of a competitor here.

The company’s fundamentals are at a comfortable level, with very solid credit updates from both S&P Global and Moody’s, which are now holding E.ON at BBB+ or equivalent.

Key performance drivers for 2024 and what can happen that can disturb this ongoing positive trend is organic RAB growth, unwinding of 2023A dispatch cost benefits, COVID-19 recoveries and the like (which are absent this year), and other comps from 2023 which drove results upward. On a comparative basis, this year seems to become a rather “clean” fiscal if this makes sense, absent of a lot of the one-offs we saw last year, which should give us a good picture of what this can deliver.

E.ON has no moat, as I see it. It’s one of many utilities in the area, and even the company’s market position doesn’t deserve special consideration, either. Even If Sweden from an internal perspective is large, the segment only accounts for 15% of the company’s annual EBIT, with a low RoR.

Some analysts believe the company deserves consideration in the form of an increased share price for upcoming investments. I don’t belong to that investor group because I believe the earnings for the next few years will be poor. As such, I believe the company will underperform the sector.

Here are the risks and upsides for E.ON.

E.ON Risks and Upsides

The unfavorable valuation for E.ON made me cut my rating in my last article, and the company has not outperformed since then either. This was, therefore, the right choice.

The risk overhang I see is overexposure to certain geographies, with no material exposure outside of Europe except the Turkish market. I’m also not a fan of the deal with RWE. E.ON allowed RWE to “gobble up” many of the attractive renewable assets for a price that was, in retrospect, not on par with what it should have been. E.ON now has full retail and network exposure, something that many players in this field are actively trying to come away from. The reason is that networks are extremely capital-intensive, while retail is extremely exposed to competition and price wars. The combination of the two results in a mix that even beyond a cursory review is fundamentally unattractive – unless it’s expertly managed.

And E.ON, looking at the company’s historical rates of return and shareholder performance, cannot be said to be a top-tier utility performer or expertly managed sort of business.

The upside is focused on more macro-oriented factors, such as higher interest rates allowing for higher network returns from regulators, and the need to bring additional renewables online providing good opportunities for the business. E.ON is also appealingly positioned because a high interest rates is a positive effect to some of the factors of the company – such as pensions and provisions for nuclear.

So, those are some of the positives – and you’ll notice that the negatives provide a bit of an overhang here – this goes on into valuation as well.

E.ON – The upside is limited due to lower earnings

I’m not changing my thesis on E.ON. Some analysts increased their overall targets on the company as of 1Q24, which can be argued to be a successful quarter in most respects. My PT remains at €10.5.

The reason for this is the following.

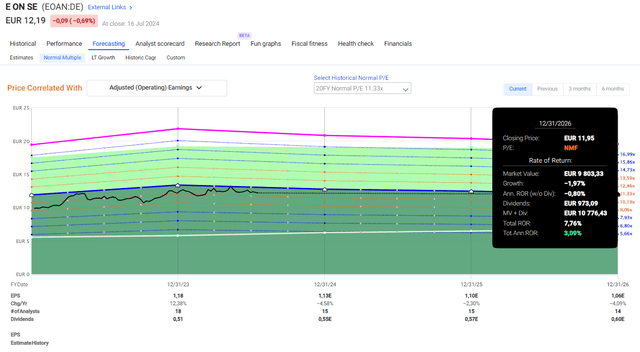

In order for E.ON to outperform, it would require the company to generate significantly better earnings than currently expected. For 2024-2026E, consensus estimates are between negative 3% to negative 5%, with an average of 3.5% (Paywalled F.A.S.T graphs Link)

It would require the company to beat by more than 7-10%, and for me, a utility very rarely does that sort of consensus beating – especially when it misses negatively 25% of the time, to begin with.

Because of the estimated decline in earnings during a rising interest rate environment (above 4-5% risk-free for the time being), with a company that underperforms the sector average yield at 4.35% at a price of €12.20, I am not positive on the company’s future value here.

I would estimate the company to be worth the lower range of its 20-year average, which is around 11.3x P/E, which comes to a €12/share estimate, or thereabouts.

This implies that the annualized upside for E.ON, even inclusive of dividends, is now less than 3.5% per year.

E.ON Upside (E.ON Upside )

Because the upside is so very low, I believe there are multiple more attractive companies available for investing here, and I would rather invest in any of those utilities than E.ON. The company would need to provide at least double-digits to a conservative earnings multiple, also 5% yield or above. That’s what it does when we’re at around €10.5/share – and that’s my rationale for this valuation.

Enel still trades at a P/E of just below 12x, yielding over 6%, and unlike E.ON is expected to grow 6-7% per year, not decline. Enel also has a safe and confirmed dividend, and an accuracy of 60-70% historically. The two companies, even though E. On was just upgraded and is also rated exactly the same at BBB+. This is why I am heavily invested in Enel, and why I am not heavily invested in E.ON at this time – and why my cost basis for E.ON is, in fact, a single digit share price from 2023.

For now, my thesis on E.ON is as follows.

Thesis

- E-ON is a market-leading energy company in Europe with some of the best and largest infrastructure networks in the continent. I have successfully invested in the company several times, meaning that I have significantly outperformed the market by investing in E.ON – at least at times.

- The company is now fully valued for the potential headwinds the company is facing. E.ON is a “HOLD” now based on its valuation and a continued conservative PT of €10.5.

- I’m keeping my “HOLD” and I am starting to look at potential alternatives for investing and reinvesting. I’m not changing my price target here. Enel is a far better investment here and is my current choice in multi-utilities.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is now a “HOLD” for me due to an unfavorable valuation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here

Q2 2025 Earnings Call Transcript")

")