")

")

Q1 2025 Earnings Call Transcript")

(NASDAQ:MU)")

(NYSE:DT)")

Introduction and investment thesis

Dynatrace, Inc. (NYSE:DT) is a leading company in the modern IT observability market, providing customers actionable insights what’s happening exactly within their IT infrastructure and applications. Thanks to the company’s services, customers can prevent costly downtimes or quickly debug arising issues. The observability platform of Dynatrace is characterized by a high degree of automation, where AI-based solutions are leveraged for many years. These features grant the company an important competitive advantage in the market. Thanks to strategic acquisitions over the past years, the company has broadened its market scope and is currently offering application security and log management services as well.

In my previous article on the company, I have argued that the continued growth of emerging product categories, increased investments in sales, and strengthening partnerships with hyperscalers (especially with Microsoft (MSFT)) and GSIs will soon lead to a reacceleration in top line growth. Well, the company’s latest Q3 FY24 earnings print refuted this theory of mine, but I think it would be too early to give up on the shares now.

I understand that many investors could be frustrated that DT shares delivered “only” 22% return over the past year, whereas many other Software as a Service, or SaaS, companies even doubled in market value. However, let’s not forget that DT shares also corrected significantly less during the 2022 downturn due to their relatively defensive nature within the high-growth software space. This mainly results from DT focusing on large enterprise customers with more stable revenue streams, which is combined with a subscription-based pricing model.

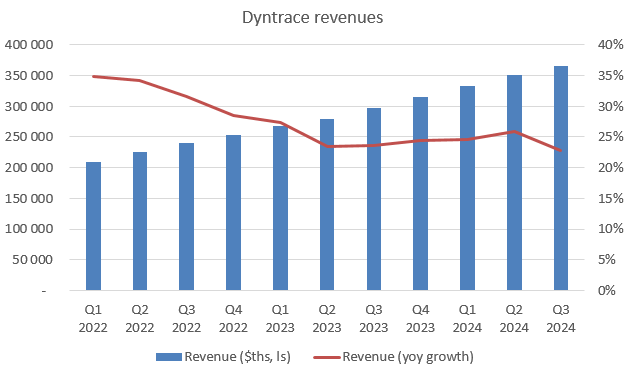

As opposed to a usage-based pricing model (e.g., key competitor Datadog (DDOG)) customers couldn’t dial back spending on DT’s platform all of a sudden when things got shaky, leading to significantly slower top line growth deceleration than for many other software peers. Now, as cloud spending seems to pick up in general and usage-based pricers begin to experience revenue growth reacceleration (e.g., Amazon’s (AMZN) AWS), Dynatrace must wait a few quarters until existing subscriptions expire and new ones with higher commitments will be signed. Taking at a look at revenue trends over the previous quarters, this phenomenon is reflected there indeed:

Created by author based on company fundamentals

Although FX effects distort the dollar-based revenue figures presented above to a slight extent, one thing is obvious. as many SaaS companies suffered from revenue growth slowdown during 2022 and 2023, Dynatrace’s top line growth held up relatively well. However, just as many software companies begin to turn the tide DT negatively surprised investors with its most recent earnings print where the YOY revenue growth rate ticked down 3 ppts to 23%.

Based on this, I believe it’s no wonder that shares reacted negatively to the earnings release, even if revenues of $365 million beat the average sell-side analyst estimate by $7 million, and the total revenue guidance for FY24 has been increased by $10.5 million. I believe the buy-side hoped for an even stronger print, not for further visible top line growth deceleration.

Words vs numbers

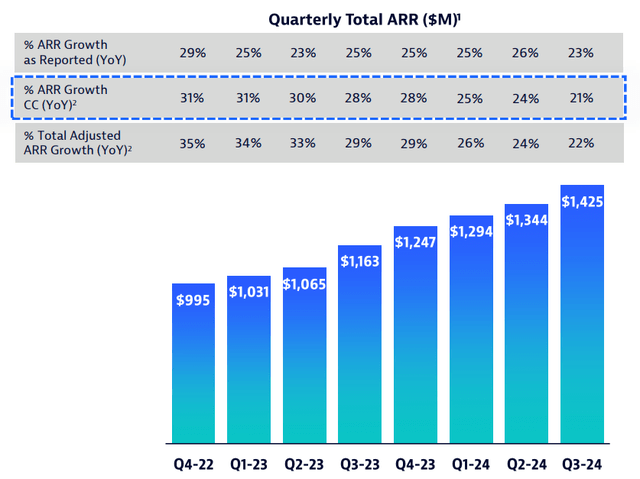

If we look at the more forward-looking metric of annual recurring revenues (ARR), which measures the daily revenue of all subscription agreements at the last day of a quarter multiplied by 365, we can see the same trend:

Dynatrace Q3 FY24 earnings presentation

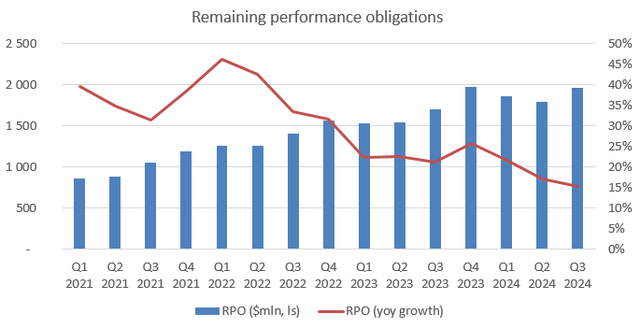

Both reported and FX adjusted figures show the same tendency confirming that investors still must wait for a visible turnaround. Looking strictly at numbers there is another, even more forward-looking indicator for revenues, remaining performance obligations (RPO). These include both billed and unbilled customer commitments and can be found in the quarterly 10-Q filing of the company. Looking at the tendency of RPO in recent quarters seems not encouraging as well:

Created by author based on company fundamentals

Although customer commitments grew $163 million compared to the previous quarter in a seasonally stronger Q3 the YOY growth rate continued to grind lower reaching 15%. As RPO growth is declining for the third straight quarter that’s not a good sign for the upcoming quarter. In the light of this, I can easily imagine that ARR growth continues to slow further in Q4 FY24, which is supported by the fact that management decided to lower its full year ARR growth guidance by 1 percentage point to 18-19%. On the top of that, YOY comparisons will be pretty tough as well, as the company had a relatively strong quarter in Q4 FY23. Based on this, investors will need more patience to let the company prove that they can benefit from an improving IT spending environment where observability is playing an even more important role.

At this point, it’s important to turn to the DT’s Q3 earnings call, where management provided a more optimistic near-term outlook for the company than what was visible from the reported numbers for the first sight. Here is what Jim Benson, CFO had to say on the demand environment within the observability market in general combined with a few helpful company specific metrics:

“The observability market opportunity is growing, the demand environment remains healthy and our pipeline continues to grow at a faster pace than our reported ARR growth rate. More specifically, within the sales funnel, we are seeing a growing number of larger and more strategic deals related to observability architecture and vendor consolidation initiatives, and we expect this directional heading to continue.

To give you a sense of the magnitude of this trend, the number of deals in the pipeline greater than $1 million of ACV, both new logo and installed base, has increased 39% compared to the same quarter last year. We view the growing number of these deals as a sign that the increasing complexity of managing fragmented tools is becoming unmanageable, and customers are looking for a partner to help them drive business value and tool consolidation.” – Dynatrace Q3 FY24 earnings call.

As I have shown in the previous section, some of these larger deals the CFO talked about have not appeared in ARR or RPO numbers yet, otherwise we would see more encouraging numbers there. This means there could be a handful of larger deals in progress, which could be signed in the upcoming 3-6-9 months depending on where they exactly are within the sales cycle. 39% YOY growth in deals with more than $1 million ACV is significantly higher than recent RPO growth rate of 15% or ARR growth rate of 21%, which suggests that revenue growth rates should experience an uptick in the upcoming quarters.

Based on my experience with Dynatrace management over the past two years, they’ve always provided informative insights into the business and followed up on their promises. I have no doubt that the CFO’s words carry significant weight and try to help investors during a time when reported fundamentals point to a more uncertain direction.

Something, which probably makes things even more confusing is that management decided to decrease its FY24 ARR growth guidance by 1 pp to 18-19% YOY growth. At first sight, this could be hard to reconcile with the previous optimistic comments from the CFO. The explanation for this has been the larger variability inherent in these enterprise-size deals with regards the time needed to close them. So, management decided to stay prudent and build in some buffer into the guide reflecting this increased variability.

Beside the consolidation narrative, which will be an important driving force in the SaaS space over the upcoming years, management also shared some other company-specific growth drivers, which are still intact and could contribute to revenue growth reacceleration.

First, the company’s log management and application security solutions are still sought after by customers providing efficient cross-sell opportunities beside DT’s core observability platform. Both are still on track to achieve at least $100 million ARR by the end of FY25, which could collectively mean more than 10% contribution to total ARR. As an example, the number of paying log management customers has grown ~50% QOQ in the Q3 quarter, which an outstanding achievement in my opinion. Meanwhile, DT managed to close its largest application security deal in the quarter with a leading payment technology company. On the top of that the company announced plans to acquire Runecast, a provider of AI-powered security and compliance solutions, which should strengthen its security offering further.

Second, the company’s recently introduced DPS (Dynatrace Platform Subscription) platform continues resonate well with customers. For an annual spending commitment, which can be drawn down throughout the year the platform enables access to all of DT’s capabilities, increasing the chance of successfully cross-selling other products. In Q3 the company closed more than 150 DPS deals with more than 10% of customers currently using the solution. According to management those customers who are on a DPS contract tend to consume faster than those who aren’t, so the increasing penetration of this solution should be revenue accretive over the upcoming years as well.

Based on the information presented until now, I remain optimistic that Dynatrace manages to reverse the decelerating trend in top line growth, which should take 1-2 quarters tops in my opinion. However, with the recent earnings print DT became a show me story, and if competitors report better numbers, the share price could continue to lag until there is visible improvement in fundamentals.

One positive in the recent earnings print, which could lend some stability to the share price, has been that margins continued to remain best-in-class. TTM non-GAAP operating margin reached 28%, while TTM FCF margin reached 25% in Q3, with the company reporting GAAP profit for many quarters now unlike several peers. However, as global interest rates begin to decrease and risk sentiment improves further investor focus will gradually shift back to top line performance in my opinion, which leaves DT no other choice than to deliver on its promises.

This is the reason I modified my Strong Buy recommendation for the company to Buy even though I strongly believe that fundamentals will materially improve over the upcoming quarters. As a long-term investor I stick to my position, and I would still recommend shares at current levels for those who haven’t initiated a position yet.

Valuation and risk factors

With DT trading at a market value of ~$15.8 billion combined with a $1.43 billion sales estimate for FY24 shares trade at a Price/Sales ratio of 11. If we assume that topline growth reaches a CAGR of 25% over the upcoming three years – as the factors discussed above contribute to growth reacceleration – shares would trade at a P/E ratio of 22.6 when calculating with a net margin of 25%.

When I compare this to the current P/E ratio of ~20 for the S&P 500 (SP500), it suggests to me that shares are relatively undervalued compared to the market in general as a closing valuation gap within 3 years seems overly conservative to me regarding DT. This would mean that a leading SaaS company would trade at the same ratio than the S&P 500 in three years’ time, which is not a realistic assumption in my opinion. To avoid this, DT shares should outperform the S&P 500 over this horizon making them a good long-term investment.

Finally, considering risk factors the most important one is currently that DT fails to live up to those expectations, which have been set by management on the Q3 earnings call. I believe investors are getting impatient after relatively softer share price performance over the previous year, so another quarter of disappointing fundamentals could pressure shares to an even greater extent.

Other, general risk factors, which are worth to look out for are the possibility of a recession, which has been predicted now for two years, or the possibility of higher rates for longer if inflation would begin to pick up again. Both scenarios would be bad for growth stocks, especially the second one in my opinion as it could been evidenced over 2022.

Conclusion

Dynatrace delivered a somewhat weaker than expected earnings print, especially from a buy-side perspective. Management tried to sooth investors’ nerves during the Q3 earnings call by highlighting significant progress in large, consolidation deals, which could turn the tide for the company soon. Beside the consolidation narrative there also some encouraging signs from emerging products, which could support a growth turnaround. These developments should be visible in the company’s reported fundamentals over the upcoming quarters, which could provide the long-awaited boost to the share price.

Read the full article here

")

")

Q1 2025 Earnings Call Transcript")

(NASDAQ:MU)")

")